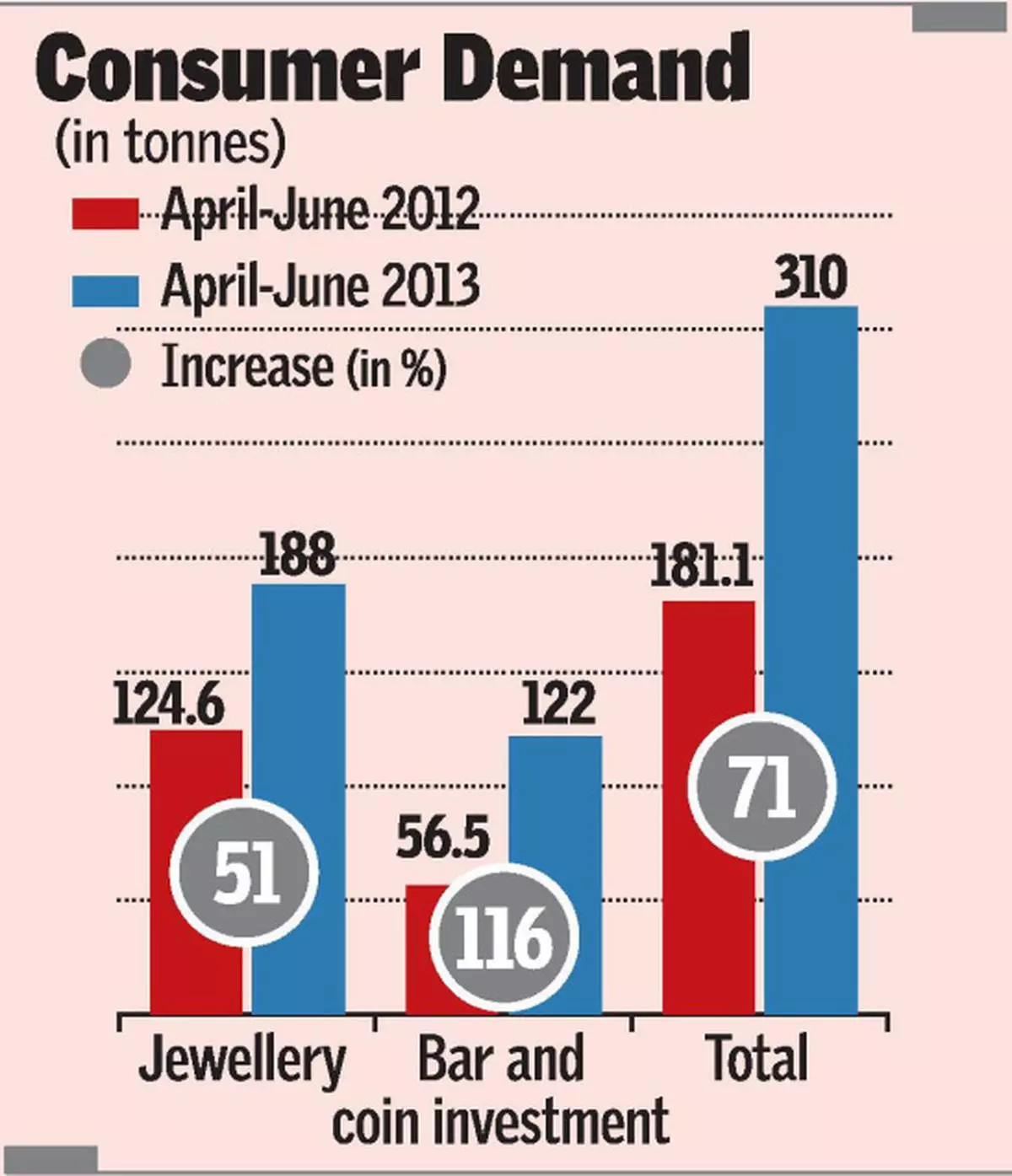

Amid all the efforts being made by the Government to curb gold imports, demand for the precious metal in India zoomed to a 10-year high (310 tonnes) in the three-month period ending June 30, according to the World Gold Council.

“We see a notable dampening of Indian demand in the coming months, more than would normally be expected during the usual Q3 slowdown, as the market digests import regulation changes. Indications for the fourth quarter so far remain positive,” the council, a body of gold producers, said in its report ‘Gold Demand Trend for Second Quarter (April-June), 2013’ released on Thursday.

The report said that total demand rose by 71 per cent compared with the second quarter last year. During the period, jewellery demand surged by 51 per cent, while the demand for bar and coins increased 116 per cent.

The introduction of restrictions on payment terms for gold imports in May and an increase in import duties in early June created an uncertainty in the market. However, it had a limited impact on end-user demand, which was met by stocks that had been built up to healthy levels following the price drop in April. Nevertheless, imports tailed off in June, with demand slowing sharply as the market entered its seasonal quiet period, even as the Government extended the restrictions on imports and further raised import duties to 8 per cent.

In recent weeks, the change in emphasis from restricting payment terms to linking import quotas to exports is likely to create further confusion and exaggerate the normal Q3 (July-September) lull in Indian demand ahead of the Q4 (October-December) festival and wedding season, the report observed.

However, it is interesting to note that price premiums in India have recently spiked higher again, suggesting that demand is healthy. “A good monsoon season so far also bodes well for demand later in the year, with the assumption that the market will, by then, have had time to digest and acclimatise to the recent restrictions imposed by the Reserve Bank of India (RBI),” the report said.

The report comes within two days of further tightening of import norms. First, the Government raised import duty to 10 per cent (third since January) on Tuesday, while it banned import of coins and medallion on Thursday. It has also been decided to tighten the norms related to gold. Out of the total import, 20 per cent will need to be exported, while 80 per cent will be used for domestic consumption. The import can be done only on the basis of full upfront payment. The same norms will be applicable on imports of gold ore and monitoring will done be at the refinery level.

> shishir.sinha@thehindu.co.in

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.