Despite passing on the entire quantum of repo rate hike by the Reserve Bank of India (RBI) to its customers, HDFC Ltd saw a 66 per cent surge in its individual loan disbursements during the April to June quarter. This is the highest-ever growth in disbursements seen by the company during the first quarter of any financial year.

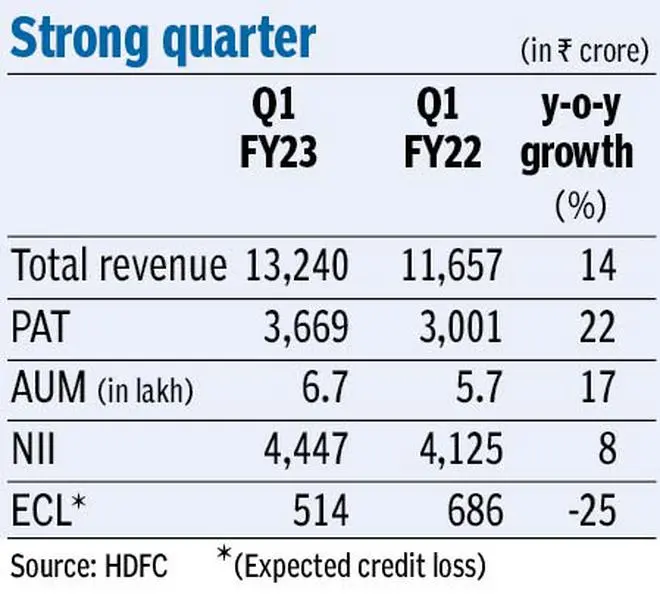

This helped the housing financier post a 22 per cent year-on-year rise in its profit after tax for Q1 FY23 to ₹3,669 crore. In terms of assets under management (AUMs), the growth in individual loans was 19 per cent, the highest percentage growth in HDFC’s individual loan AUM in eight years.

Total AUM stood at ₹6.7-lakh crore as of June 30, higher than ₹5.7-lakh crore a year ago.

“The demand for home loans and the pipeline of loan applications continues to remain strong. Growth in home loans was seen in both, the middle income segment as well as in high end properties,” the non-bank lender said.

The RBI cumulatively raised the repo rate by 90 bps over May-June, in an attempt to curtail the elevated inflationary pressures. Over the same period, HDFC, too, raised its retail prime lending rate by 90 bps via four hikes, the last of which was by 50 bps on June 9. HDFC’s floating rate loans, known as adjustable-rate home loans, are benchmarked to this rate, which now stands at 16.95 per cent. Rates on such loans now start from 7.55 per cent.

Interest income

The interest rate increase, however, did hit HDFC’s interest income, with the NII rising slightly to ₹4,447 crore from ₹4,125 crore in the year-ago period. NIM for the quarter was at 3.4 per cent and the loan spread was 2.25 per cent.

“The monetary policy and interest rate actions have had a short-term impact on the NII and to a slightly lesser extent on the NIM. This has been due to the transmission lag between the interest rate increase in borrowing costs and the increase in lending rates,” Vice-Chairman and CEO Keki Mistry said in the earnings call.

The growth is also lower due to a high base, as overnight interest rate swaps had fallen in the year-ago period due to the ample liquidity in the system, thus expanding NII and NIM. Excluding the impact of these two factors, NII growth for the quarter would have been at 16 per cent, in-line with the AUM growth of the company, Mistry said, adding that HDFC has now shifted from a quarterly reset for individual loans pricing to a monthly reset, to reduce the impact of transmission of rate changes..

Asset quality

As of June 30, the gross NPA for the individual loan book was at 0.98 per cent, whereas that for the non-individual loans portfolio stood at 4.44 per cent. This is an improvement compared to December 31, 2021 — the first quarter of reporting under the new RBI norms — where gross individual NPA was at 1.44 per cent and the gross non-individual NPA was at 5.04 per cent.

The overall NPA ratio also improved to 1.78 per cent from 2.32 per cent at the end of December.

HDFC held total provisions of ₹13,328 crore as of June 30. Expected credit loss for the quarter was at ₹514 crore, lower than ₹686 crore in the previous year. Credit costs for the company, too, fell to 33 bps from 50 bps and the company hopes to further normalise credit costs to pre-Covid levels over the course of the year, Mistry said.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.