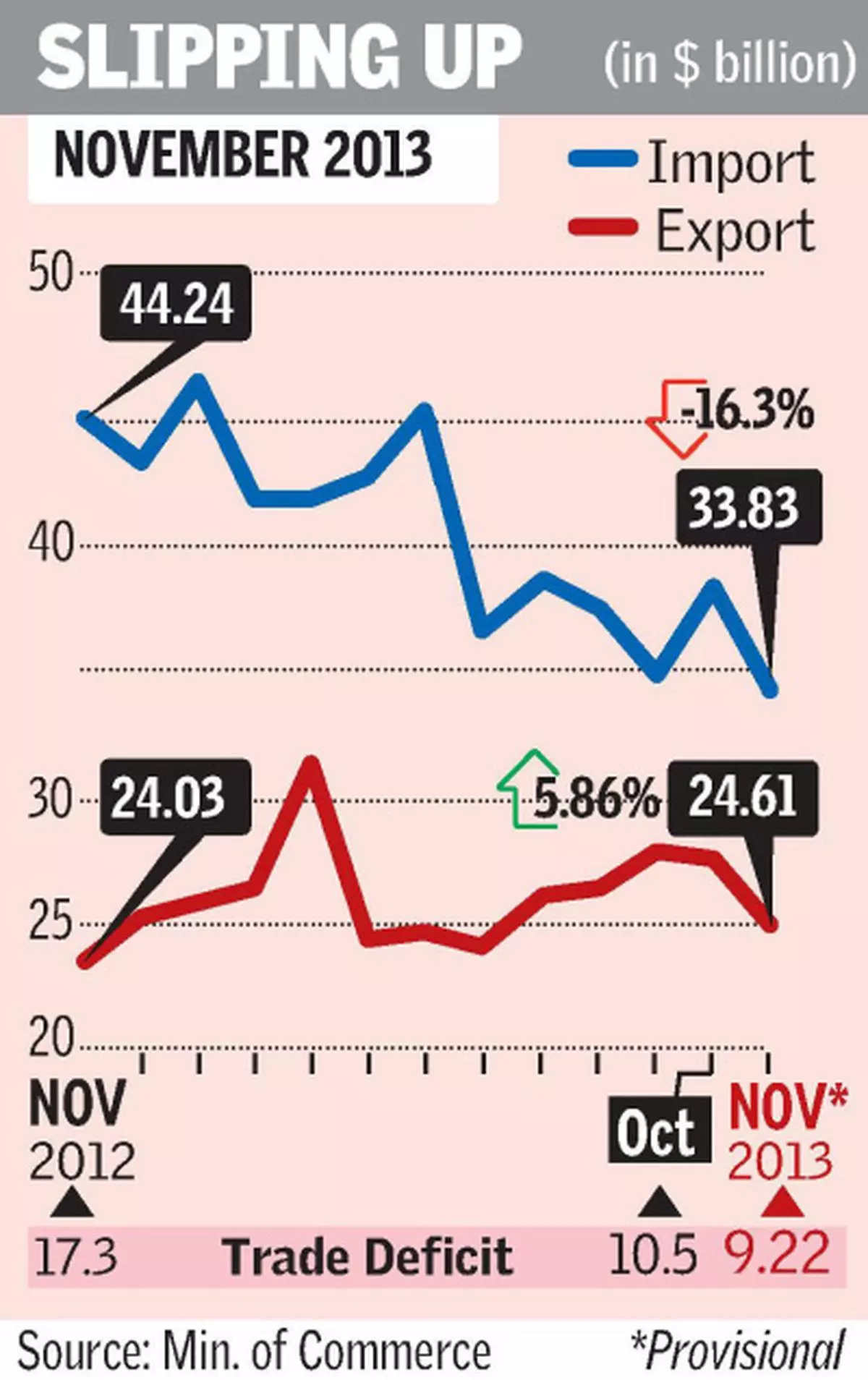

Export growth has slowed down 5.86 per cent to $24.6 billion in November 2013 compared to the same month of the previous year as the shipments of gems & jewellery, petroleum products and pharmaceuticals declined.

Exports in the preceding four months had witnessed a double-digit growth.

November imports

Imports during the month declined 16.37 per cent to $33.83 billion as gold imports continued to fall because of restrictions put in place by the Government and petroleum imports, too, went down.

Gold and silver imports went down 80 per cent to $1.05 billion from $5.4 billion.

Trade deficit

Trade deficit during the month narrowed to $9.21 billion compared with $17.2 billion in November 2012.

Despite the slowdown in export growth, the Government is confident that it would reach the target of $335 billion for the year, Commerce Secretary S.R. Rao said.

Gems & jewellery export

Rao said that the fall in export of gems & jewellery was mainly due to a sharp growth in raw material prices during the month. “However, prices have now started coming down and we expect that the export growth of gems & jewellery will be back on track,” he said.

Both export and import of petroleum products have gone down during the month because of fall in global prices of oil. “Global prices have fallen by $5-$7 per barrel due to some good news on Iran front,’’ the Commerce Secretary said.

April-November data

Exports during April-November 2013 posted a 6.27 per cent growth at $203.98 billion. Imports went down 5.39 per cent to $303.89 billion. Trade deficit was lower by $30 billion at $99.9 billion.

![]() Comments

Comments

from 240 GW in September last year")

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.