Call it founder Narayana Murthy’s Midas touch or a comeback for Shibulal, but consistency finally seems to be returning to Infosys’ financials.

The company, for the second successive quarter, beat market expectations with its numbers in the September period.

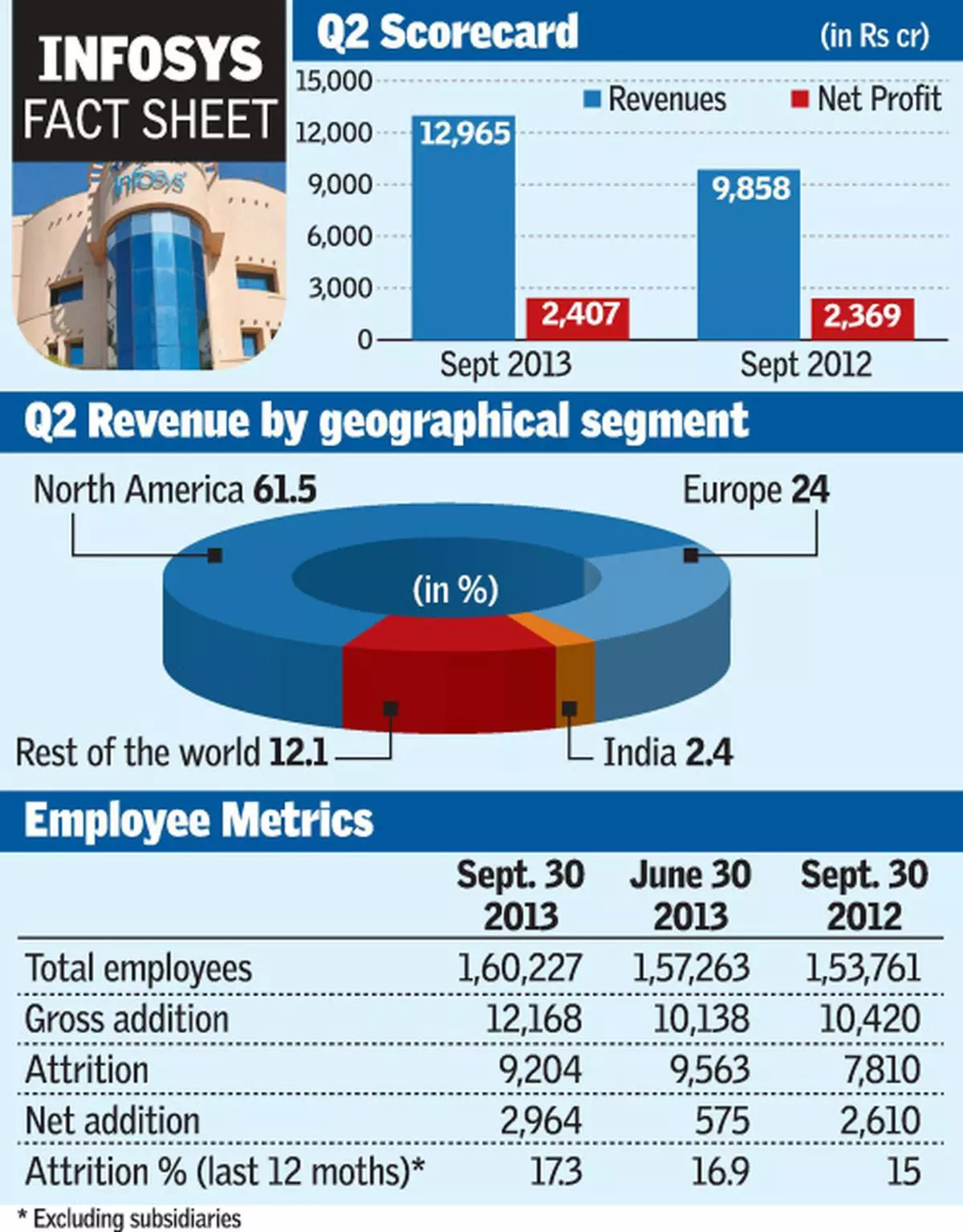

Steady volume growth, improvement in realisations and greater traction from its top clients characterised its results. Both the North American as well as the European geographies grew and key segments such as manufacturing and energy and utilities managed to expand at a healthy pace.

The icing on the cake and the reason markets cheered the results, is the upgrade in guidance on revenue growth to 9-10 per cent in dollar terms. This definitely looks achievable given its show in the first couple of quarters.

In the quarter, Infosys’ revenues grew by 15.1 per cent sequentially (3.8 per cent in dollar terms), while net profits expanded by 1.4 per cent. Net profit growth has been lower due to wage hikes as well as increase in selling and administrative expenses. A visa-related issue has resulted in the company provisioning Rs 219 crore, reducing profits.

All-round performance

Infosys managed to deliver a 3.1 per cent increase in volumes (person-months billed) and a marginal increase in realisations as well. After pricing declines in the past few quarters, realisations now appear to be stabilising. Revenues from its top clients have increased at 5.9 per cent sequentially, much faster than the overall company’s growth rate, indicating significant improvement in client-mining strategies, an aspect that has come into greater focus over the last couple quarters.

Both its key geographies of North America (3.9 per cent growth in revenues) and Europe (5.2 per cent) have witnessed significant traction. All segments led by manufacturing, energy & utilities experienced healthy growth in revenues.

In term of client additions, the action was in the mid-size deals during the September quarter as 15 clients were added in the $10-50 million range.

Clearly, the growth has been well-rounded and across segments which means that it is steadily catching up with TCS and HCL Technologies. The company’s stock, which was trading at a discount to HCL Technologies, has over the past few months gone into premium zone and trades just under the valuation that TCS commands.

Infosys has delivered good numbers in the two seasonally strong quarters. But even factoring in a generally weak December quarter, the company looks well placed to exceed its guidance of 10 per cent growth for the full year.

![]() Comments

Comments

, apparel, durables are the key categories that will create winners in the consumer tech and brand space")

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.