Banks seem to be getting back on the growth path after two years of the Covid-19 pandemic.

Fourth quarter results of a number of private sector lenders reveal that most have reported higher profitability on the back of robust growth in net interest income as well as lower provisions. There has also been an improvement in asset quality.

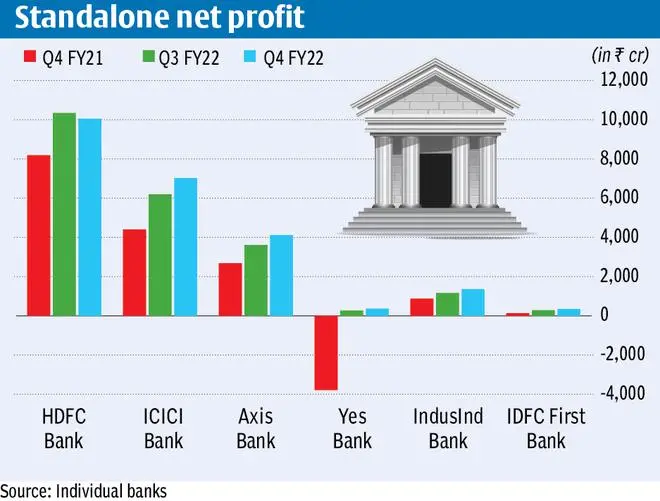

While HDFC Bank reported a 22.8 per cent year-on-year increase in its standalone net profit in the quarter ended March 31, 2022, ICICI Bank’s standalone net grew 59 per cent year-on-year (y-o-y) to ₹7,019 crore in the same period.

Axis Bank registered a buoyant 54 per cent y-o-y growth in standalone net profit to ₹4,118 crore in the January to March 2022 quarter. Yes Bank seems to have recovered from its past troubles and reported a net profit of ₹367.46 crore in the fourth quarter of FY22.

Limited third wave impact

Bankers and analysts note that the third wave of the pandemic had little impact on economic activity, unlike the second wave. Repayments and credit demand have both been on an improving track.

Sumant Kathpalia, Managing Director and CEO, IndusInd Bank, said that the economy had showed strong resilience last fiscal with activity levels bouncing back to pre-Covid levels across various segments, supported by effective policy measures.

“The bank too saw improvement across disbursements, deposits and asset quality with receding Covid impact,” he said.

IndusInd’s standalone net profit increased by 55.4 per cent in Q4 FY22.

Improving demand

Almost all banks are optimistic about prospects in the current fiscal, notwithstanding ongoing geopolitical tensions.

Credit growth is also expected to improve this fiscal, as is demand from the corporate sector, which has been muted till now.

Ashutosh Mishra, Head of Research, Ashika Stock Broking, said, “Banks are reporting very healthy business as well as profitability growth, on both quarter-on-quarter and year-on-year basis. It looks like they have returned to the growth path, leaving behind the trouble from the Covid-19 pandemic. We expect this trend to sustain in FY23 as bank’s credit growth is positively impacted by the inflationary trend in economy and expected lower credit cost.”

Almost all banks are fully provided for in terms of Covid provisioning and capital requirements, he added.

More clarity on banks’ performance will emerge as large lenders such as the State Bank of India announce their results.

Bullish on sector

Aditya Acharekar, Associate Director, Care Edge Ratings, said, “We are positive on the sector. Banks are well-capitalised and profitability is also improving. We expect credit growth above 10 per cent this fiscal, led by retail loans and corporate demand picking up. With no significant impact from Covid after the second wave, there have not been any major asset quality challenges and recovery has happened as businesses get back to normal.”

Banks have seen an increase in advances in the fourth quarter and incremental provisioning cost has been lower, which has improved the profitability, he said.

“Monitorables would include impact of higher interest rates on credit demand. The SME book may also need further monitoring for asset quality pressures,” he added.

Earnings recovery over fiscals

In a recent report, Motilal Oswal noted that after reporting dismal earnings over FY17 to FY20, banking sector earnings have picked pace.

“Strong capitalisation levels will enable dilution free growth as we estimate system loan growth to sustain at 13 per cent CAGR over FY23 and FY24,” it said.

Banking system asset quality has witnessed significant improvement over recent years with GNPA and NNPA ratio declining to 6.9 per cent and 2.3 per cent as on September 2021, it added.

“While we remain watchful of restructured portfolio and asset quality trends in SME segment, we nevertheless estimate GNPA ratio for our coverage universe to moderate to 4.2 per cent by FY24 while NNPA ratio touches decadal lows of 1.3 per cent,” the Motilal Oswal note said.

![]() Comments

Comments

for better management of KYC (know your customer) profiling of the customers")

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.