Goods and Services Tax (GST), since its implementation in 2017, has attracted much debate. Recently, some commentators termed the achievement of record April GST collection of ₹1.87-lakh crore on the back of a growth of 12 per cent as hype since the growth was preceded by a decline. It has been suggested that tax buoyancy has been low and collections have shown higher growth only after September 2021; the growth rate of 14 per cent at which the States were promised to be compensated has not been achieved.

Naysayers even argue that while it could not achieve the desired growth rate, it took away the flexibility of the States to raise revenue, thereby leading to double jeopardy for them.

To evaluate the performance of GST in terms of revenues to the Centre and the States, it is pertinent to take a closer look at the tax collection data for the last ten years, which includes pre- and post-GST periods.

The efficiency of a tax system is best measured by tax buoyancy which is the ratio of tax revenue growth to the growth in GDP. A buoyancy of one implies that the taxes are growing at the same rate as GDP while a buoyancy of more than one indicates that the tax revenues are growing at a faster clip than the GDP.

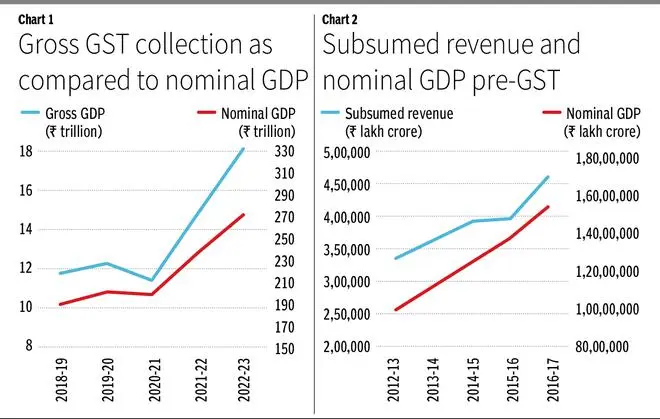

We take buoyancy over a five-year period to eliminate noise arising out of short-term comparisons. The average growth rate of gross GST revenues for the period 2018-19 to 2022-23 is 12.3 per cent as compared to average nominal GDP growth rate of 9.8 per cent, implying a tax buoyancy of 1.25, an impressive number for any tax, let alone a new one (Chart 1).

During first 20 months of its implementation, significant rate reductions were announced with a view to stabilise the new GST regime, and this was followed by severe macroeconomic and social uncertainties due to Covid pandemic. Despite this, buoyancy of 1.25 is impressive. The trend in the last two years is even more encouraging, with a buoyancy of 1.4.

In comparison, for the five-year period of 2012-17, the buoyancy of taxes which were subsumed in GST (subsumed taxes) was 0.9988. The reality is that GST collections in the last two years have been growing faster than the increase in prices and GDP. This is clear evidence of good performance and stability of the GST system.

Impact on States’ revenues

The analysis would be incomplete unless we examine whether the GST has benefited States, and, if yes, by how much. At the time of introduction, it was agreed that Centre would compensate States for any loss below 14 per cent year-on-year growth over revenue from subsumed taxes, taking 2015-16 as the base year. It must be understood that this benchmark rate of 14 per cent did not have any economic or empirical basis. It was part of the agreement amongst States and the Centre to introduce GST.

In fact, revenue of States from the taxes subsumed in GST witnessed a growth rate of a mere 8.3 per cent in the pre-GST four-year period 2012-16. In comparison, the GDP growth during the period was 11.5 per cent, signifying a buoyancy of 0.72, way less than 1 (see Chart 2). Thus, before introduction of GST, States’ revenues from subsumed taxes were growing significantly slower than GDP.

On the other hand, due to implementation of GST, during 2018-23, States’ SGST revenues (including compensation released to States) witnessed a buoyancy of 1.22. This totals to revenues of ₹37.7 trillion to the States in this period and include post-settlement revenues of over ₹29.2 trillion and compensation of ₹8.5 trillion released during this post-GST five-year period. Even without compensation, State GST revenues have witnessed a buoyancy of 1.15, which is significantly higher compared to pre-GST buoyancy.

Had GST not been implemented, applying the buoyancy of 0.72 of pre-GST period to the GDP growth rate of 9.8 per cent during the post-GST five-year period would have resulted in a growth rate in State revenues of only 7.1 per cent, that is, almost half the agreed rate of 14 per cent. This would have resulted in aggregate revenues of only ₹27.9 trillion to the States.

Clearly, States have benefited from the introduction of GST. This works out to almost ₹9.8 trillion in the five-year period of 2018-19 to 2022-23.

Sovereignty

Neither the Centre nor States have lost sovereignty. In contrast, they have pooled their sovereignty on decisions on indirect taxes. One of the biggest triumphs associated with GST is the spirit of cooperative federalism, with almost all decisions on GST being taken with consensus among members of the GST Council comprising the Centre and States. At the State and district levels, tax administrations of the Centre and States are working harmoniously.

Thus, the Centre and States have gained in terms of revenue. However, no reform can be said to be successful unless it yields benefits for its people at large. GST has brought about huge benefits for businesses in terms of elimination of cascading taxes, a simplified and digital compliance framework, savings in logistics cost and time, etc.

The GST@5 Survey conducted by Deloitte finds that 90 per cent of industry leaders view the transition to GST as largely positive. Most importantly, GST has brought about benefits for consumers by reduction and transparency in taxes. Clearly, GST is a success story for all Indians to cheer.

Malhotra is Revenue Secretary and Pandey is Joint Secretary, Department of Revenue, Ministry of Finance

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.