RBI Governor Raghuram Rajan said recently that when central bankers say they are the only game in town, they, in fact, become the only game in town. Other policy-making institutions and regulatory bodies then find it easy to pass the buck. To be charitable to such bodies, they may not be aware that they have an important role to play — along with the central bank — in sorting out things. The price is paid by the industries/sectors the other bodies “regulate”.

Rajan made that remark at a global meet (to honour him); but, interestingly, it would seem to apply quite closely to the current Indian situation.

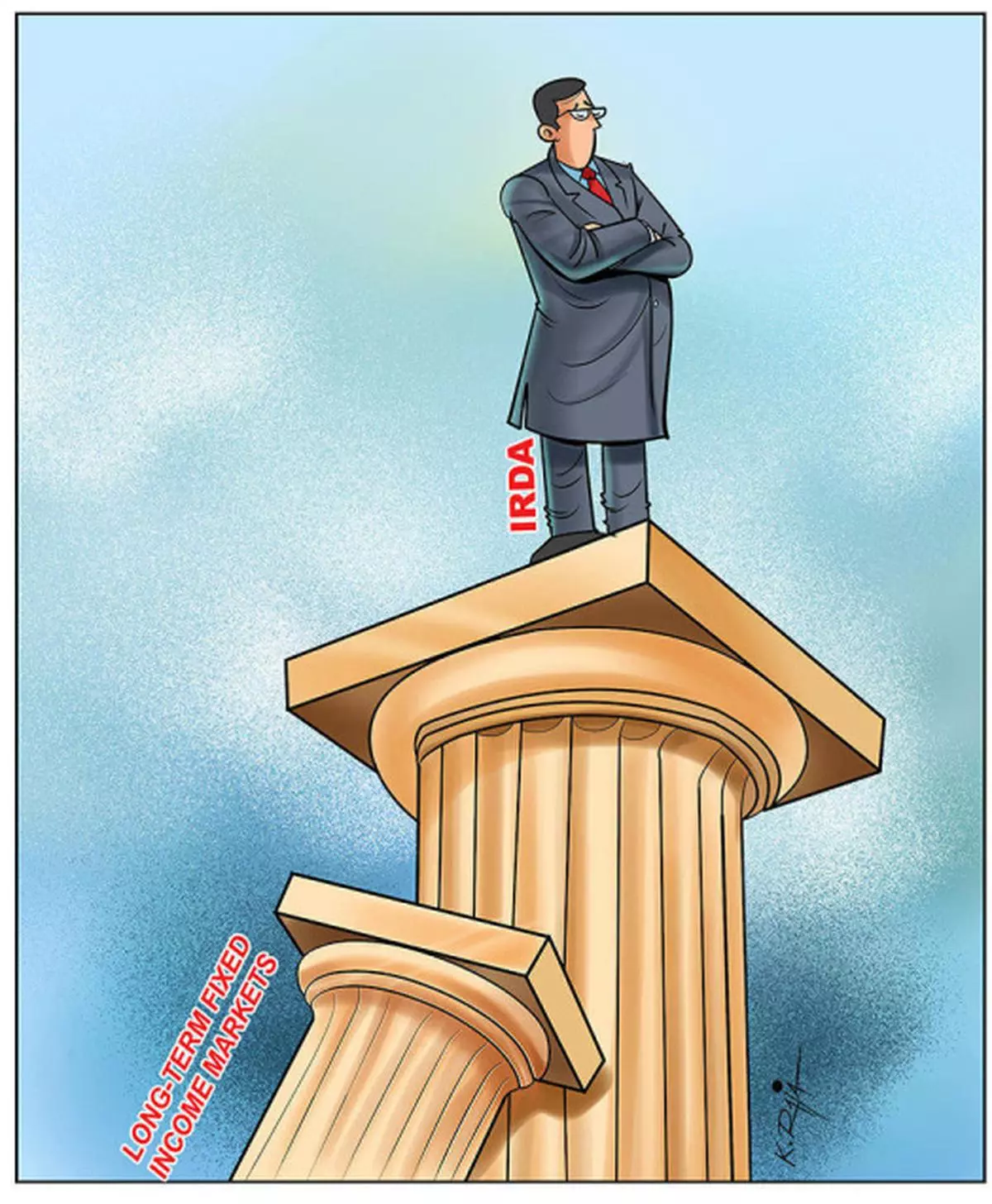

Applies to IRDA

In the Indian context, one (financial) regulatory body which should be working very closely with the RBI in developing long-term financial markets, long-term financial instruments and products (primarily fixed-income markets of long-tenor such as 15 or 20 years) is the Insurance Regulatory and Development Authority (IRDA). That would serve the interests of the insurance regulator well. The potential of intermediating between savers such as households and borrowers such as infrastructure projects can create a great business future for India’s fledgling private sector insurance companies.

It helps RBI as well: Through such markets, India’s banking sector can de-risk itself of large-scale project finance risks. They will allow banks to sell assets that they have no comparative advantage in holding --- such as long-term loans to completed infrastructure projects, which are better held by infrastructure funds, pension funds, and insurance companies.

India’s life insurance industry, after a promising start in the early 2000s on the back of booming stock markets, is now battling a significant slowdown in business growth. The underlying investment environment for life insurers — dominated by exposures to the equity markets in the 10 years up to 2010 — has turned decidedly unfriendly, with India’s stock markets remaining true to their long and well-known reputation: That they are a high-risk investment avenue for the average household. That, coupled with over-zealous regulatory moves to counter supposedly aggressive business and marketing practices in the industry, has nearly sent the industry into hibernation. The perceived difficulties in the business environment have also led to a number of foreign investors (at least six) exiting their Indian JVs in the recent past.

Unfortunately, we hear almost nothing from the IRDA on the development of long-term fixed income markets in India. What are IRDA’s views on the role of other policy-makers such as the RBI and Finance Ministry in developing credible long-term bond markets in India?

Should the RBI be completely divested of its public debt management function? And should it deal in government securities only to implement its monetary policy moves? Across countries, has life insurance growth been facilitated by the existence of credible fixed-income markets? What is the impact of sustained, “positive” real interest rates on the growth of fixed-income markets and wholesale investors such as insurance companies, pension funds? That is the kind of public pressure that the IRDA should be applying on other policy-makers to force action.

Given the long-term financial markets space in which the IRDA (and its regulated companies) operates, it (IRDA) has all the locus standi to publicly air its views and assessments on this issue.

The RBI may well welcome such assessments and public pressure emanating from other financial regulators — for its work is then being done by the others!

If that is too much to ask for, can’t the IRDA at least latch on to overall market/product development and see how that can be applied to the insurance industry?

In particular, one would have wished that the IRDA would lobby strongly for the proposed CPI-linked savings certificate to be a permitted investment for wholesale financial institutions such as insurance companies. The CPI-linked savings certificate would qualify as a “bang on the dot” kind of long-term financial instrument which can potentially draw in large amounts of retail investor participation — precisely the market which the life insurance companies should be capturing for growing their business on a long-term and sustainable basis.

But, here again, we get only thunderous silence from the IRDA.

Large Potential

All this could well be construed as blasphemy by Indian public sector financial institutions. They are not used to such public airing of even professional view points. For instance, a former SBI chairman, recently, wrote-off the RBI’s policy rate moves as immaterial — but only a few days after his retirement.

But, blasphemy may well be required if things are to change fundamentally.

For, look at the potential in household savings in India and how much of that can be captured by long-term players such as life insurers — in the form of credible fixed-income products rather than as stock market investments.

There are only around 1.3 crore demat accounts in India currently — though, there can potentially be 40-50 crore accounts (assuming only urban households participate in stock markets).

But, Indian individuals hold as much as Rs 31,00,000 crore of deposits with banks. One-third of such deposits are in the rural/semi-urban areas.

A sure way to tap into that large corpus of savings — which are perforce bottled down with the banks in the absence of other credible institutions and instruments — is the development of credible fixed-income markets. IRDA should be the prime player here.

(The author is a Chennai-based financial consultant.)

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.