Manufacturing works as a growth-engine when its growth is higher than GDP growth. China is an excellent example. During the last 30 years, its high manufacturing growth drove a big jump in per capita income — five times more than India’s.

India has undertaken a host of policy initiatives and reforms, besides fiscal and business-friendly measures for accelerating manufacturing growth. These include National Manufacturing Policy 2011 (NMP), Make in India (2014), Startup India (2015), Atmanirbhar Bharat Abhiyan and Production Linked Incentive Scheme (2020), concessional corporate tax, GST, etc.

The NMP and Make in India envisaged annual manufacturing growth of 12-14 per cent and its share in GDP rising from 16 per cent to 25 per cent by 2022. However, the growth in manufacturing IIP index was far below GDP growth during FY 2012-20. Its share in GDP declined to 13 per cent and share in exports declined from 80 per cent to 60 per cent. Persistently, the manufacturing growth and investment remain subpar relative to their potential.

Subdued Investment

The RBI’s Report on Currency and Finance, FY 2022 (RCF) discusses the secular stunted capital formation in industrial sector except for a few resource-based industries over the last two decades. The report highlights the declining share of electronics, computers and traditional labour-intensive industries like textiles in aggregate capex. It analyses how the persistent structural constraints result in overall low value addition.

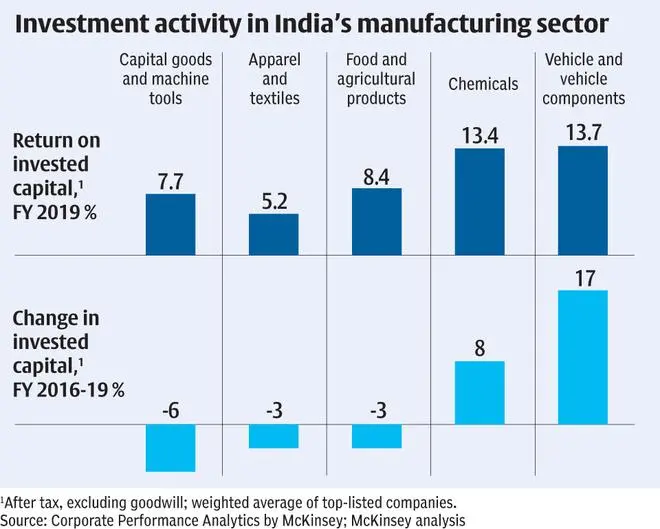

An article (‘A new growth formula for manufacturing in India, 2020’) by Rajat Dhawan and Suvojoy Sengupta of McKinsey finds that “nearly 700 of the top 1,000 manufacturers produced returns that were less than their cost of capital in 2018, thereby destroying value. By contrast, the sectors that generated healthier returns saw increases in invested capital during the four years from 2016 to 2019”.

The decline in invested capital in case of top-listed companies in capital goods, textiles and food industries over FY 2016-19 is pronounced (see chart).

All these developments go against the various credible policy reforms and pro-growth measures taken over the years to accelerate the sector’s growth.

The stark ground reality is that covert Chinese imports have led to this situation. Unequal and unhealthy competition from massive mis-invoiced/covert Chinese imports has destroyed Indian manufacturing. Surprisingly, this reality is grossly overlooked. Further, the information opacity relating to price, quantity and quality of these covert imports make a project’ risk assessment difficult. These imports encourage trading and assembling business at the cost of manufacturing investment.

Chinese Import menace

Steady growth in Chinese imports began since mid-2000s following China’s WTO entry and our removal of quantitative restrictions on import of consumer goods. CAGR of officially recorded Chinese imports were 48 per cent over FY 2003-08 and 25 per cent over FY 2003-18. The value of covert imports can be manifold vis-a-vis this value. Even with subdued consumption and GDP growth, disruptions in world trade and strained relations with China, imports from China were at a record level of over $80 billion in FY 2022.

The surge in scale and range of Chinese imports, aided and abetted by unscrupulous means including connivance among exporters, importers, clearing agents and customs, has sapped the performance, vitality and innate potential of the sector. An import-dependent consumption, production and trading structure has evolved, characterised by imports of final products, assemblies and critical components.

These suppress value addition and capex. A study by Chidambaran Iyer, Centre for Development Studies, (bit.ly/3xfZKV3), finds the average value addition by mobile assembling units was 5.4 per cent in FY 2018. Anecdotally, IGST from imports continue to be much higher than CGST. These reflect shallow manufacturing base.

China’s predatory approach to trade as seen in dumping, currency manipulation, intellectual property theft, production of counterfeits of global and local brands, wide-range of export incentives and mis-invoicing. Economies of scale and cheap imports create colossal damage and entry barriers for Indian manufacturing. Other visible and invisible costs include industrial sickness, generation of black money, underdevelopment of skill/technology, growing unemployment and loss of tax revenue.

Many of these critical points are documented in the following: the 145th Report of the Parliamentary Standing Committee on Commerce, 2018; the Report of Directorate of Revenue Intelligence (2015) to the Supreme Court-appointed SIT on black money; India: Potential Revenue Losses Associated with Trade Misinvoicing, Global Financial Integrity 2019; Illicit financial flows between China and developing countries in Asia and Africa, George Herbert 2020; Estimates of Trade Mis-invoicing and Their Macroeconomic Outcomes for the Indian Economy 2014, Raghbendra Jha and Duc Nguyen Truong.

Spill-over effects

The number of corporate debt restructuring references spurted from 225 to 622 during FY2010-14, with corresponding aggregate debt spurting from ₹95,815 crore to ₹4,29,989 crore.

Non-oil trade surplus of $6.4 billion in FY 2003 rapidly turned into a massive deficit of $37 billion by FY 2008 and $91 billion in FY 2018. Surge in trade deficit driven by import-intensive consumption leads to lower savings and investment (as percentage of GDP). Savings declined (35 per cent to 28 per cent) and gross capital formation (from 34 per cent to 28 per cent) over FY 2012-22.

The RCF mentions pre-pandemic deterioration in share of manufacturing in gross value addition. The CAGR in manufacturing IIP index was only 0.8 per cent over FY 2018-22. Following demonetisation and Covid waves, disruptions in trade credit (TC) or inter-firm credit and its repayment flows aggravated the manufacturing sector’s woes and contributed to the structural imbalances like excessive system liquidity, low credit demand and surge in corporate liquidity holdback.

Although institutional credit support is abundantly available, given the predominance of TC in financing the input-output chain this lack is not easily addressed. Millions of day to day B2B commercial transactions are impaired by credit repayment fragility. Credit inadequacies impact macro-level output and aggregate credit. The causality runs from disruptions in trade credit network to investment and output vulnerabilities. Additionally, banking sector imbalances also set in.

Way ahead

We need to take well-calibrated action against covert imports without creating sudden and large disruptions in the production structure. Make in India strategy needs to be synchronised with planned phasing out of these imports and spurring domestic capex and capacity. Random, surprise and thorough checks of illicit imports at the ports need to be intensified. More international cooperation is required to curb hawala dealings.

For smooth flows of TC and its repayment, it is necessary to engender trust which can create a sound ecosystem of secured credit-based B2B transactions. In these matters, including self-regulation/self-discipline, industry associations’ role is critical and effective. Their reputational weight can work more effectively and efficiently than legal remedies in resolving the dysfunctional TC network.

The writer is former DGM, SIDBI

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.