The role of the Monetary Policy Committee (MPC) in dealing with inflation gives rise to a few questions: Is the MPC overestimating its power and control over inflation (as measured by the Consumer Price Index)? What impact do the repo rate and reverse repo rate — henceforth the Standing Deposit Facility (SDF) rate — have on containing inflation? If the MPC’s target is to manage a measure (the CPI) which is more driven by supply side factors, the key issue is whether tinkering with the demand side by raising rates will add to the problem instead of resolving it.

Let us approach the topic from first principles. The MPC has been mandated to keep CPI inflation at a level of 4 per cent, with a variation of +/- 2 per cent, in terms of the RBI Act. In the last para of the relevant Gazette Notification dated August 5, 2016, the terms “due objectives of growth” are also included. So, there is need for the MPC to balance both growth and inflation, as per its mandate.

The MPC has been using both quantitative and pricing (rate-setting) tools in its bid to target inflation and spur growth. It also uses its statements/stance to tether inflation “expectations” . Thus in the immediate aftermath of Covid, the RBI cut interest rates to almost the lowest levels in the last three decades at least and the repo rate (benchmark at which RBI is ready to lend overnight money to banks) even now stands at 4 per cent. Along with this it also offered to infuse money supply through provision of liquidity cumulatively amounting to about ₹17-lakh crore. The RBI says that about ₹11-lakh crore of this was availed or was infused into the system.

Inflation inching up

Of late, however, the inflation rate (CPI) has been inching up. This week it has been reported that inflation for March was close to 7 per cent. This is in line with international trends.

The CPI in India is measured by the Ministry of Statistics and Programme Implementation on a monthly basis. Out of 100, the weightage for food and beverages is 45.86, Clothing and Footwear 6.53, and Housing 10.07. The items clubbed under Miscellaneous constitute 28.32, while fuel and light is 6.84, and Pan/Tobacco/Intoxicants, 2.38.

Ultimately it is the prices/cost rise of the above items which the MPC/RBI has to keep between 2-6 per cent through the use of monetary policy tools. In this list, except for Pan, etc (weightage 2.38) and recreation/amusement (under miscellaneous, weightage of about 5 per cent), the rest are all essential items, with absolutely no elasticity in relation to the availability of money. Just because someone has money on hand, he/she is not going to stack up on rice, vegetables, groceries beyond what is required. So the price rise is not demand-driven (in other words, not driven by loose/cheap money)

On the contrary, it is “supply-side, cost-push” factors which affect the prices of most items constituting the CPI. If onions are in short supply, the prices go up. The same for pulses. (Remember that the RBI coined the term “protein-inflation” around 2012-13 to explain the inflation induced by high prices of pulses!). And it is universally acknowledged that commodity price spikes and fuel rate hikes have been the reason for the high CPI.

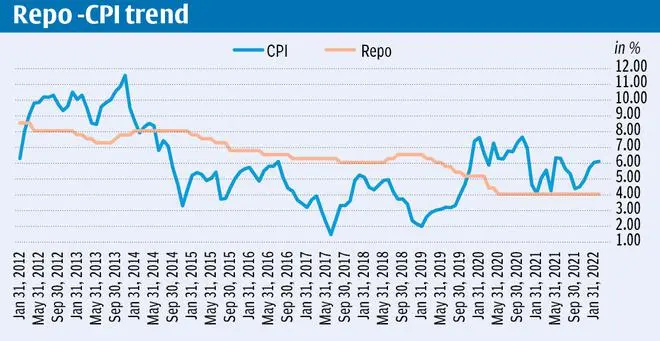

Apart from these intuitive observations, it is further found that the correlation between the repo rate and the CPI is moderate to weak. The actual figure is 0.37, over a period of 10 years (See graph).

There have been periods (2012-14) when the repo rate was consistently below the CPI as also during the recent period (2021-22). Even if we were to think in terms of lag effect, the coefficient is not strong enough to support a repo hike as an antidote to inflation.

Inversely, a high rate regime may indeed aid inflationary pressures by adding to costs, just when we should be trying to reduce them. Just look at how the 10-year yields have spiked by 20/25 basis points within a day of the effective reverse repo (SDF) being hiked by 40 bps.

That one public sector bank has already raised its lending rate is indication of what it can do to the overall cost of money for all borrowers, particularly the MSME segment. The clear worry is that the recent MPC move could potentially raise costs for all borrowers and lead to further price increases.

To rein in inflation and push growth, risk weightages can be used as a tool. Raise the risk weightage (even drastically) to sectors where you don’t want cheap money to flow/lead to price spikes and simultaneously even go to the extent of lowering risk weightages (say for the priority sector) where you want support to be extended.

This course of action will go against asset price rises, without hurting other sectors where growth impulses are needed. While acknowledging that the MPC/RBI’s role is complex and its track record has been exemplary, it may well consider such options in these uncertain times over a non-discriminatory, across-the-board increase of cost of money.

The writer is a top public sector bank executive. The views are personal

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.