The Indian telecom sector has been in a state of turmoil over the past three years, with regulatory tangles, intense competition and falling tariffs.

But after all this churn, select incumbent players seem to be emerging as clear winners from a scenario where there were once as many as 13-14 operators in every service area.

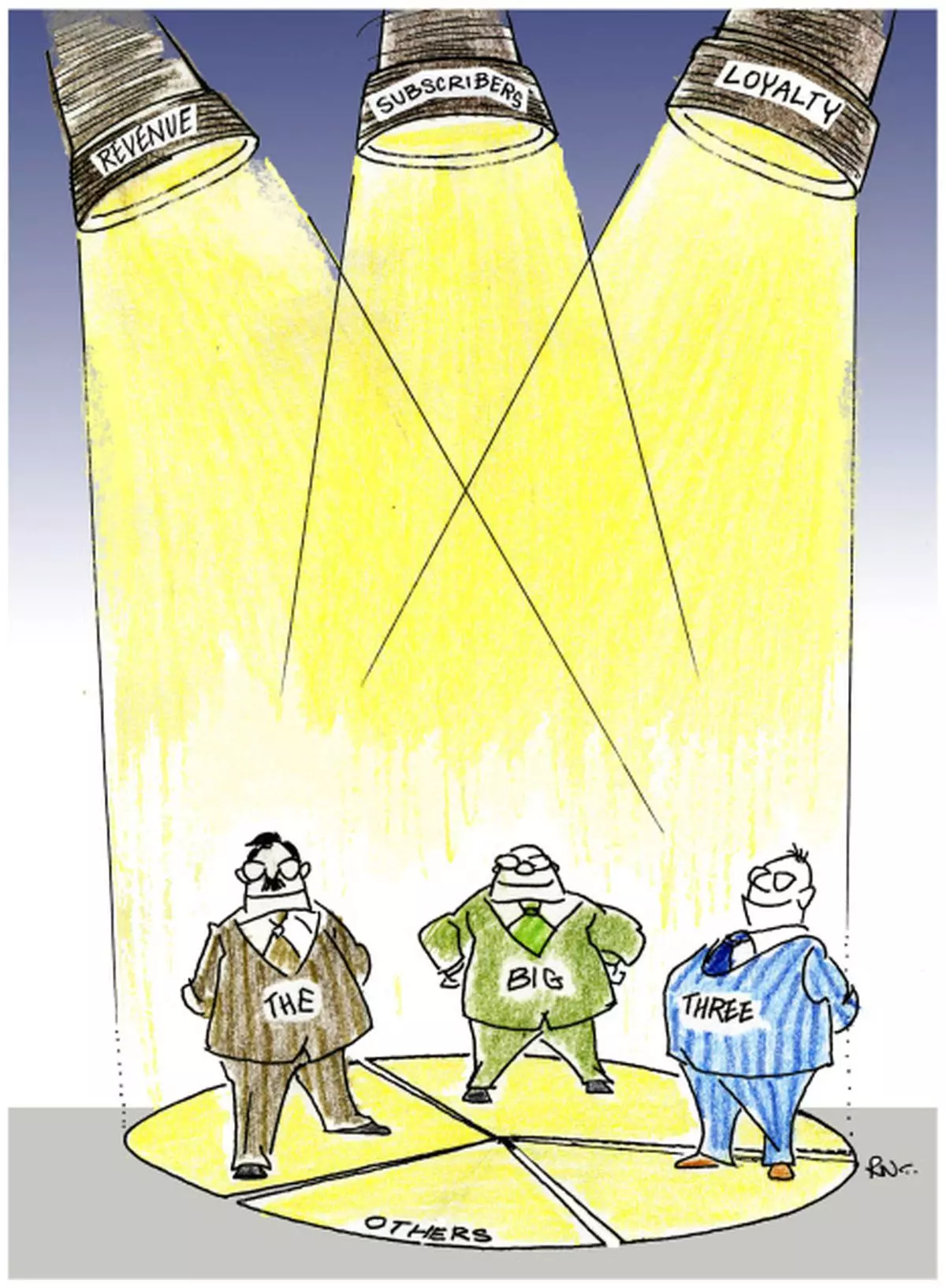

Bharti Airtel, Vodafone and Idea Cellular seem quite ahead of competition in criteria such as revenue market share, subscriber market share and also in terms of proportion of customers who are loyal to their networks.

Other incumbents such as Reliance Communications and BSNL have slipped considerably across parameters.

Here’s an assessment of the tangled web that is the telecom sector and the four trends that investors should look out for.

Revenue matters more than subscribers

Where subscriber share was all the rage a while ago, it is revenue market share or RMS (the share of revenues that an operator is able to garner), that is the key metric to track today. RMS has become important as mere addition of subscribers does not seem to be contributing to the topline of players.

Vodafone and Idea Cellular lead the way in revenue market share. The former has steadily increased its RMS over the past two years and now has a share of 22.5 per cent. Idea Cellular has been even better, recording constant improvements to register RMS of 14.9 per cent.

Bharti Airtel, on the other hand, witnessed some decline in RMS over the past few quarters, but has bounced back in the latest one. Its RMS has always been above 30 per cent and is currently at 30.1 per cent.

The top three players thus control more than two-thirds of the overall industry’s revenues.

Bharti Airtel, Vodafone and Idea Cellular have subscriber market share of 20.1, 16.5 and 12.5 per cent, respectively.

A difference of 2.5-10 percentage points between RMS and subscriber market share (SMS) clearly suggests that the three players have a fairly high proportion of regular and lucrative subscribers.

The data released by the Telecom Regulatory Authority of India (TRAI) indicates that 83-92 per cent of subscribers on these three operators’ network are active and recharge regularly and use their services. This proportion is a good 20-40 percentage points ahead of other players.

All the three have also not been averse to increasing tariffs over the past few quarters, without too much of a churn, indicating the return of pricing power. They have thus been able to keep their realisations per minute at a stable level, generally over 40 paise.

On the other hand, players such as BSNL and RCom have steadily been losing RMS over the past three years.

From mid teens, these two players now have RMS of 6.9 per cent and 7.7 per cent, respectively, while their SMS is 10.5 per cent and 16.6 per cent.

Clearly, subscriber addition isn’t translating into revenues for these players.

Tata Teleservices has struck a better note with both RMS and SMS of around 8.6 per cent. This may be attributed to the reasonably successful GSM operations over the past few years, though the company still thrives on tariff sensitivity.

The other key player, Aircel, has RMS of 5 per cent but SMS of nearly 7 per cent.

Time for consolidation

The consolidation that everyone has been talking about for a long time actually seems imminent now.

For one, the top 7 players now control 92 per cent of the industry’s revenues, with the other 6-7, barring Uninor, becoming fairly insignificant. With BSNL, Tata Teleservices and Aircel still reporting losses, and Reliance Communications still struggling with huge debt obligations, Bharti Airtel, Vodafone and Idea Cellular are likely to be the dominant players for the foreseeable future.

The other contenders are dropping out of the race. Etisalat, Loop and STel are likely to shut down operations in India. There are reports that Sistema is in talks to buy out Aircel.

Videocon, a minor player with barely 6 million subscribers, was expected to shut down operations. But in a surprise move, the company has decided to bid for the upcoming 2G spectrum auction.

Telenor, which split from Unitech Wireless (and their JV Uninor) is likely to bid afresh and transfer existing assets to itself after a settlement with Unitech.

So, from a 15-player industry in 2009, we may have utmost 8-9 players in the future.

But unlike the scenario pre-2008 when there were as many as 6 profitable players, we now have only four such players, including a struggling Reliance Communications. State owned companies — BSNL and MTNL — are now loss-making entities.

For the industry in general, and for the top three players, in particular, this signals the return of pricing power and also easing of tariff wars. Operators may now stick to realistic tariffs without making a dash to acquire subscribers at any cost.

3G yet to click

3G services were expected to be the next big wave for telecom companies. Only in India, it hasn’t panned out that way.

Despite bidding aggressively for 3G auctions, mobile operators have not seen any significant traction in terms of subscriber additions or ARPUs.

Bharti Airtel and Idea Cellular have less than 2 per cent of their overall subscriber base as 3G customers, after more than a year of operations.

What this tepid addition of customers indicates is that India may still not be a market where customers may pay heavily for high speed data access or for other value added services.

That even this segment is price-sensitive is borne out by the fact that even a significant reduction in 3G rates by the top four players barely made a dent in subscriber additions.

Clearly for the foreseeable future, the industry is likely to be 2G-voice-led, which may further weaken the case for new entrants or proxy entrants.

Regulatory overhang hasn’t gone away

The proposal to levy a one-time charge on operators that hold excess spectrum and re-farming of airwaves are key challenges for the entire industry.

The EGoM had decided last month that it would levy a fee on operators that have more than 4.4 MHz spectrum (in case of GSM) and 2.5 MHz (in the case of CDMA).

For the top 6 operators this would entail an outflow of Rs 2,200-10,000 crore, with BSNL/MTNL having to pay the maximum. The total outflow for the industry is estimated to be Rs 27,000 crore. This would have to be paid for the balance period of their existing licences. The outflow is linked to the base price of Rs 14,000 crore set by the government for the upcoming 2G spectrum auction for pan-India operations.

The other more complex overhang is on re-farming of spectrum where incumbent operators must vacate the entire spectrum in the 900 MHz band when their licences come up for renewal over the next few years and would be moved to the less efficient 1800 MHz band. The EGoM has now indicated that companies can retain 2.5 MHz of spectrum in the 900 MHz band by paying market linked price.

Most operators may challenge these orders, if passed, legally.

In any case they may bid very selectively. Also, the top three-four players have the option of using spectrum won in the 3G bidding in the 900 MHz band for future voice usage and can migrate their top revenue generating customers to this band.

Stick with the top

So what does all this add up to for the investor who is keen to bet on telecom?

Idea Cellular and Vodafone (when it lists in India) may offer the best prospects for investors as they increase footprint and also their operating margins.

Bharti Airtel may be retained by investors with a long-term perspective. Its mobile business may be under pressure in the near-term as it expands its African footprint. But the company has multiple businesses where value could be unlocked. Its tower business Bharti Infratel is set for an IPO soon.

Also, the prospect of listing of Indus Towers would benefit all the three top players in unlocking value and improving cash flows.

Both the tower companies have seen rising tenancies inching up to the ideal 2 per tower levels, and also fairly stable rentals.

The debt:equity ratio for Bharti and Idea remains quite manageable.

>Venkatasubramanian.k@thehindu.co.in

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.