It looks like there’s never been a better time to hit the road. The Centre’s infrastructure push is facilitating road travel, in particular, significantly.

Consider these numbers: Under the National Infrastructure Pipeline (NIP) plan launched in 2020, roads and highways projects account for ₹32.9 trillion, constituting 22.3 per cent of total envisaged outlay for the programme. Budget 2023 saw overall allocations for capital expenditure for FY23-24 pegged at ₹10 lakh crore, within which the allocation to Ministry of Road Transport and Highways (MoRTH) stands at ₹2.7 lakh crore. This number is 35 per cent higher than the allocation for 2022-23. In addition to this outlay, the Centre’s investment in NHAI for 2023-34 is ₹1.62 lakh crore, which is around 21 per cent higher than the previous fiscal. The increased allocation to MoRTH and NHAI brightens the prospects for the road sector, going forward.

Here are the key metrics to watch when investing in road infra stocks:

Project mix

To understand the roads sector, it is essential to know the kind of road projects that are usually awarded to companies. In India, road construction projects are broadly of three types — EPC (Engineering, Procurement and Construction), BOT (Build, Operate and Transfer) and HAM (Hybrid Annuity Model).

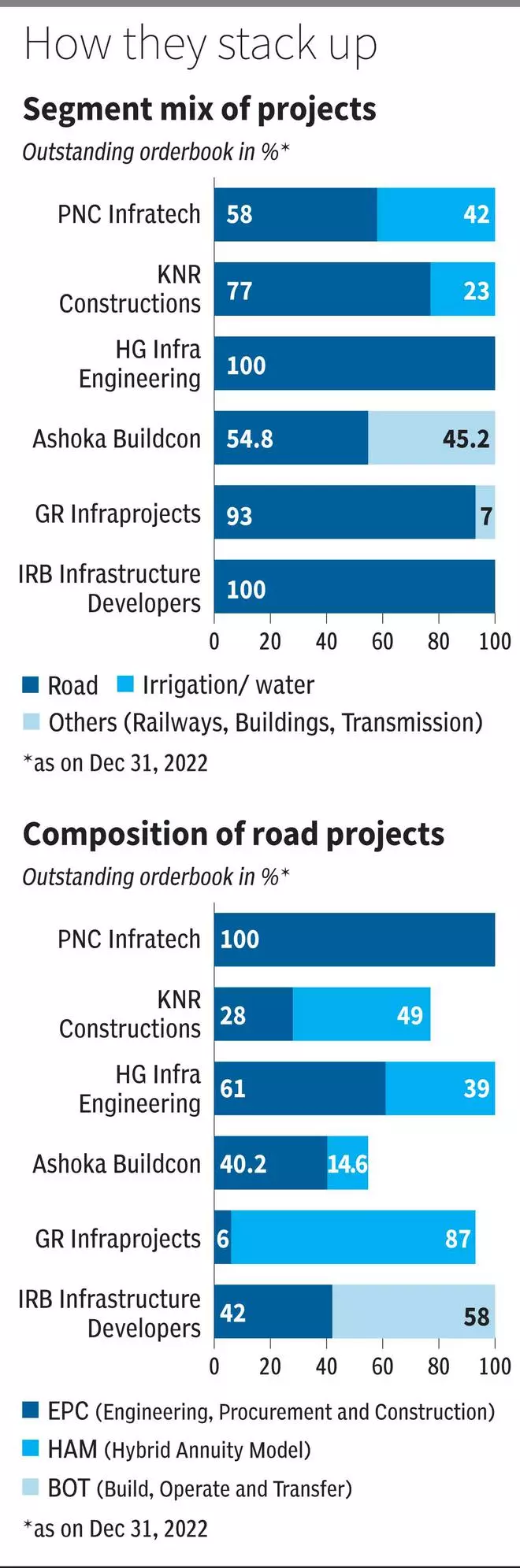

EPC contract is a straightforward one where the complete cost of the construction of the road is borne by the government. The private contractor designs and lays the road and hands it over to the government. The payment to the contractor is as per the progress of the construction. These projects have relatively low margin but are considered very secure as the amount is paid upfront and is not dependent on factors like traffic and toll collection. PNC Infratech, Ashoka Buildcon and H.G. Infra engineering are among companies that have an EPC-heavy order book.

BOT contract is a PPP (public-private partnership) model. Here, the contractor constructs, operates and maintains the road for a certain time frame, called the concession period. During this period, the developer collects toll charges from the people who use the road. In this model, the developer needs to arrange the financing, acquire the land, build the project, and hand it over to the government, post concession period.

This is the most preferred model when it comes to awarding of government projects. The long gestation and staggered revenues are a drawback. . However, since the developer has to recover the investment from the toll revenue, the scope for profitability is high, which appeals to some players. IRB Infrastructure has a BOT-heavy order book (58 per cent). IRB enjoys decent rewards for the risk taken and has an EBITDA margin of 50-55 per cent at consolidated levels.

HAM model was introduced in 2016 as an alternative to BOT, which had started to become unviable. Here, the government bears 40 per cent of the bid project cost, which will be paid in five equal instalments linked to project completion milestones. The remaining 60 per cent of the capital brought in by the developer will be repaid through semi-annual annuity payments by the government. The government will also service the interest on the loan taken by the developer — bank rate + 3 per cent. Since regular annuities are paid under HAM agreements, companies can expect a regular stream of cash flows. The margins in HAM are higher than EPC contracts but lower than BOT projects — a key reason being that in HAM, the contractor doesn’t collect toll revenue.

Going by the proportion of projects awarded, HAM and EPC models are equally popular now. As per an HDFC Securities report, out of 127 projects awarded by NHAI and MoRTH in FY22, 62 (49 per cent) were HAM projects, while 63 (50 per cent) were EPC and balance 1 per cent were BOT projects.

Order flows and execution

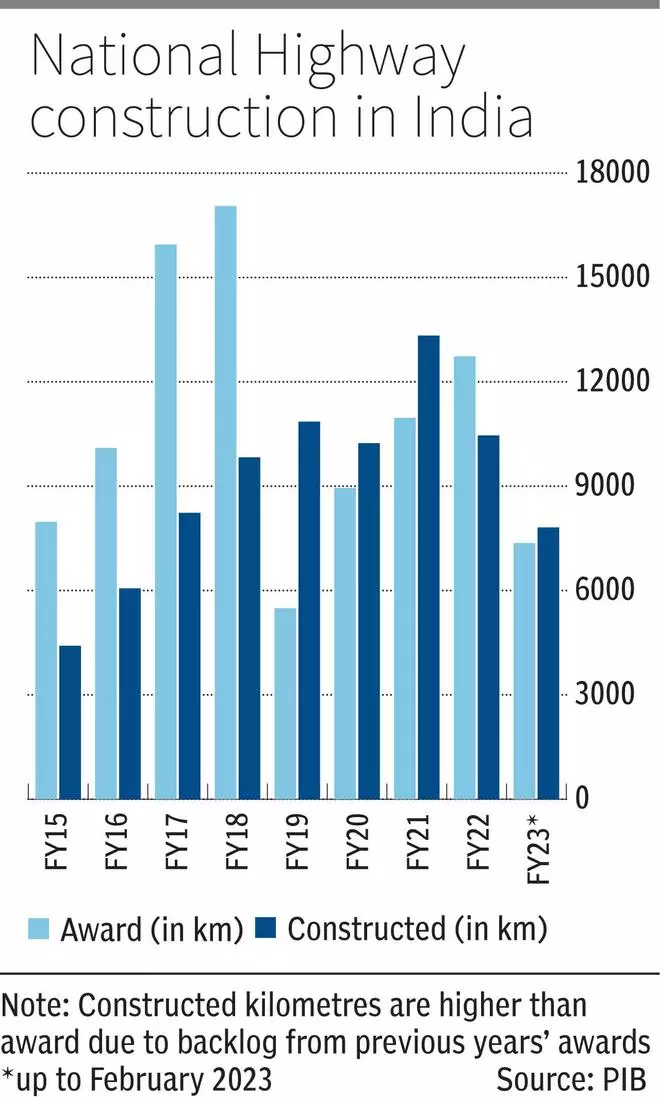

While NHAI contract awards from FY19 to FY22 grew at a CAGR of 32.33 per cent (from 5,493 kilometres in FY19 to 12,731 km in FY22), the awarding in FY23 (April 2022-February 2023) saw a 2 per cent decline year-on-year to 7,497 km. On the back of increased budgetary allocation to MoRTH and NHAI, companies expect the order inflow to pick up in the coming months.

The execution pace from FY15 to FY21 was decent as the average construction per day of National Highways rose from 12 km in FY15 to 36 km in FY21. But there was a drop in FY20 — as companies faced execution delays due to multiple reasons including embargoes related to pollution control and State-level political upheavals.

In FY23 (April 2022-February 2023), the average construction per day further dropped to 24 km — this slowdown in highway construction has primarily been due to the prolonged monsoon in some parts of the country, spike in raw material prices and land acquisition issues, amongst others. However, companies seem confident on the pace of execution picking up in FY24, going by the management commentary of listed players such as Ashoka Buildcon, H.G. Infra Engineering and PNC Infratech.

The order book of a road construction company is the outstanding work it has to execute. When seen in the light of how many years of revenue it covers, order book gives an idea of the revenue visibility of the company.

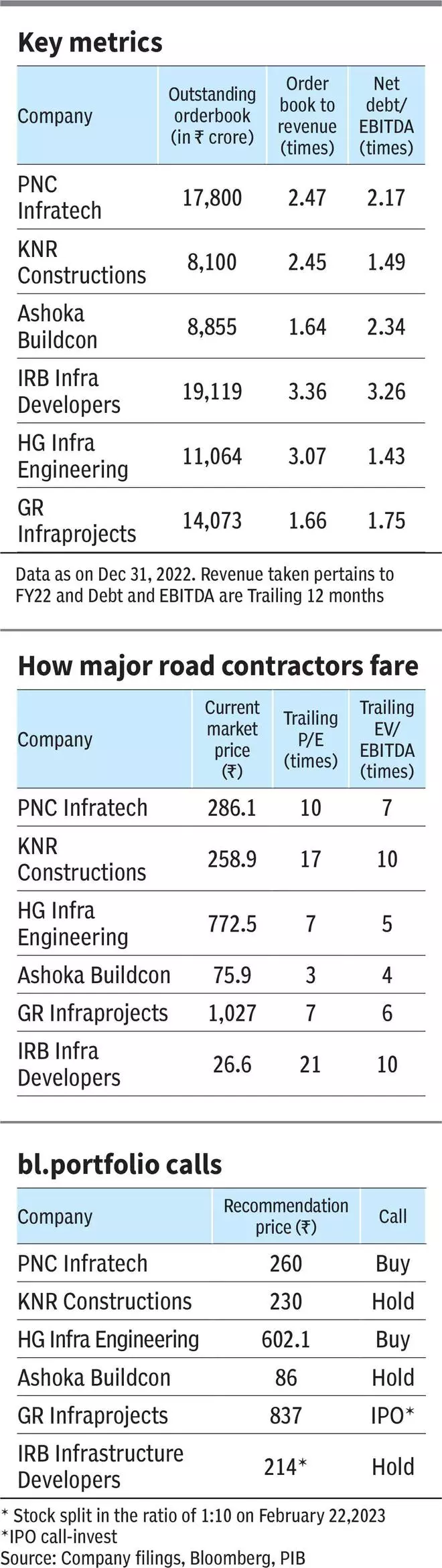

As of quarter ending December 31, 2022, Ashoka Buildcon and G R Infraprojects have an order book to revenue ratio of 1.64x and 1.66x. IRB Infrastructure, H.G. Infra Engineering, KNR Constructions and PNC Infratech have a higher ratio of 2.5 to 3.5 times.

Profitability

Bitumen, asphalt, concrete and metals such as steel are key raw materials for road players, with the costs being linked to petroleum products and energy prices.

Usually, government projects come with a price variation clause that compensates the contractors for any spike in input costs. In case of EPC contracts, the price variation clause hedges the contractor as the amount is paid as and when project progresses. However, in case of HAM projects, although the price variation clause is available, the payments are made semi-annually; due to staggered cash flows, the contractor may face pressure on the margins.

Consider KNR Constructions, for instance. The company has 49 per cent of its order book from HAM projects with the remaining being EPC/BOT and Irrigation contracts. The management stated that the steep price rise in steel and cement has put pressure on the margins (in 9 months FY23). The cost of materials rose 24 per cent while the revenue rose only 14 per cent (in 9 months FY23). This seems to have caused a decline of 90 basis points in the EBITDA margins YoY during 9 months ending December 31, 2022, and 350 basis points decline on QoQ basis. On the other hand, PNC Infratech has an order book of 58 per cent road EPC while the remaining are irrigation projects, which seems to have helped in maintaining margins. The EBITDA margins of the company saw a 191 basis points rise YoY in Q3FY23.

The management of KNR Constructions has stated that their EBITDA margins would be 15-16 per cent (annually) without irrigation project but 19-20 per cent, with it. PNC Infratech has 42 per cent of its order book from irrigation/canal projects and Ashoka Buildcon 45 per cent of its order book from Railways, Buildings and Transmission projects.

Leverage

Road construction is capital-intensive and long gestation debt is not uncommon in these companies. However, higher leverage in a rising rate scenario may have a detrimental impact on the profitability of the business. The rising interest rate scenario is particularly an issue for HAM and BOT projects as these require significant debt for project execution and the cash flows are staggered over the concession period of anywhere between 15 and 20 years. Companies sometimes resort to monetising the assets by transferring to InvITs to repay the debt and free the equity capital to invest in newer projects.

For instance, IRB Infrastructure Ltd. had a consolidated debt of ₹14,290 crore as on September 30, 2022, but in December 2022 quarter the company sold its HAM asset VK1 to IRB InvIT for ₹340 crore. The consolidated debt as per the management is ₹13,260 crore as on December 31, 2022. The interest expense of the company at consolidated level also reduced by ₹350 crore in 9 months FY23 against the same period the previous year. KNR Constructions is another company that has reduced its consolidated debt to ₹456 crore from ₹1,864 crore in September 2022 quarter, backed by sale of three SPVs.

Investors must therefore weigh companies on the basis of the above parameters — along with the overall activity of government project awarding and interest rate cycles — in order to shortlist road infrastructure stocks.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.