India Inc faced one of its toughest quarters in Q1 FY23. Crude derivatives, metals and logistic costs were simultaneously at peaks in the quarter along with a weak rupee which affected imports. We took a look at the results and the adjoining commentary in relevant sectors to assess the damage.

Unsurprisingly, the results reflected the ground reality and earnings growth has taken a breather in the quarter. The current valuation of Nifty 50 at 19 times one-year forward earnings will demand a higher earnings growth in the remainder of the year.

While cost pressures have eased in some pockets, worries still remain in others. Interest costs moving up will also be a concern henceforth. However, what can support earnings is better demand. Even as the managements acknowledged the high-cost environment, the commentary following Q1 results also reflected optimism on the demand outlook. The sharp recovery in broader index as the results season passed (Nifty 50 returned 8 per cent from mid-July 2022) has been supported by continuing plans for growth, either in capacity or in value delivery across sectors. Thus, while the print in Q1 FY23 is negative for investors, the larger demand outlook seems encouraging. Here’s a detailed look at the trends in this quarter and what could lie ahead. The analysis is for 1,268 listed companies whose Q1 FY23 numbers were out until August 7.

Revenues benefit from low base

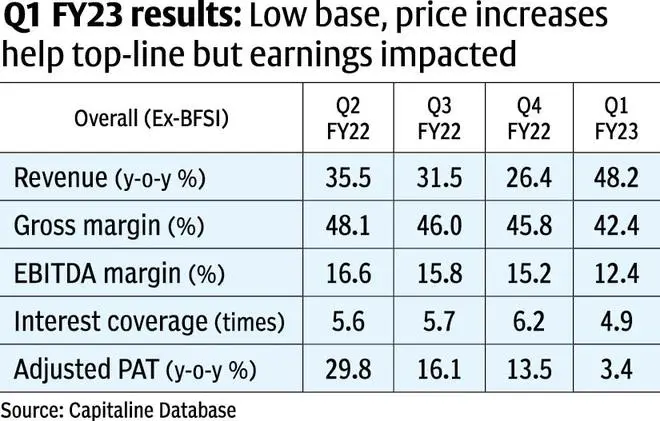

Revenue growth (excluding financials) was reported at 48 per cent year-on-year in Q1 FY23 compared to an average 31 per cent year-on-year growth in the previous three quarters. But considering the weak base of Q1 FY22 (peak second wave in May-June 2022), a sequential growth may be indicative. The revenue growth was at 7 per cent quarter-on-quarter in Q1 FY23, lower than the 9-13 per cent sequential growth seen in the previous three quarters. Viewed in conjunction with steep decline in both gross and EBITDA margins, explained below, it implies that the revenue growth was a function of price pass-through at the cost of volume growth. Segments riding on energy cost inflation — refineries, power and gas sectors reported sequential growth of 17, 19 and 32 per cent respectively, quarter-on-quarter. On the other hand, cement sector saw revenues falling 1.3 per cent quarter-on-quarter. Steel sector, which witnessed a sharp correction in steel prices, also witnessed 10 per cent quarter-on-quarter decline in revenues.

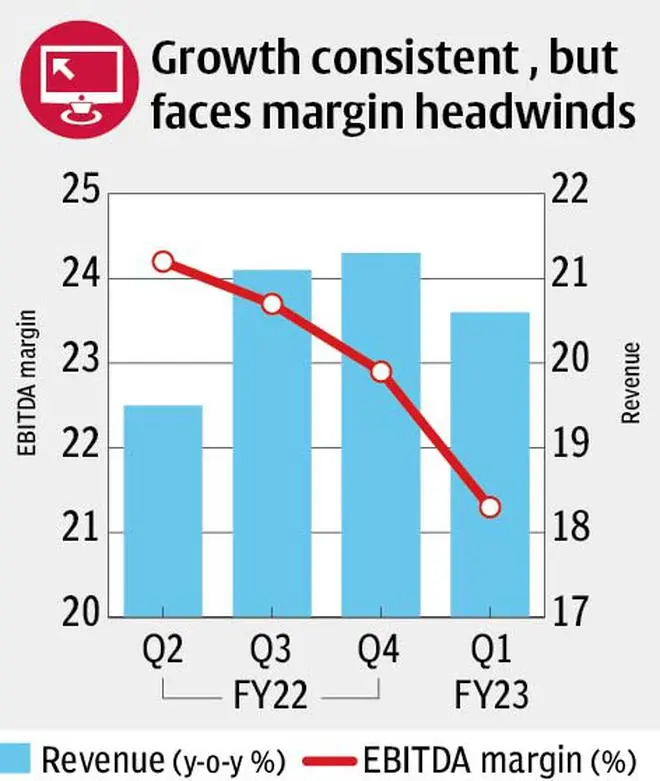

Margins under pressure

Excluding financials, gross margins have been on a constant decline in recent quarters owing to supply chain constraints earlier and significant commodity cost inflation now. From gross margins of around 50 per cent in Q1 FY22, every quarter witnessed continuous decline and reported 42 per cent gross margins in Q1 FY23. But at the operational level, higher asset utilisation and cost efficiencies had limited EBITDA margin decline till Q4 FY22 (only 140 basis points year-on-year decline). The current quarter witnessed EBITDA margins at 12.4 per cent, which is a 470-basis point year-on-year decline or 280 basis points quarter-on-quarter. So, despite passing on higher input costs to the extent possible which helped the topline, EBITDA margin declined as gross margins came down. Savings from employee and other expenses as a percentage of sales were limited this time around. Hence, the decline in gross margins reflected in EBITDA margins this quarter. All this weakness flowed through to the bottom line.

Earnings (growth) resilience finally cracks

Even in the face of consistent inflation from the middle of last year, India Inc was able to protect earnings growth until now. PAT (adjusted) growth (excluding financials) was at 14 per cent in Q4 FY22, declining from 30 per cent in Q2 FY22. But in the current quarter (Q1 FY23) when almost the entire basket of raw materials tested new highs, the PAT growth lowered to 3.4 per cent year-on-year growth (even on a weak base of Q1 FY22). Partial pass-through of input cost inflation and decline in sales volume impacted profit growth, apart from the increased debt financing costs. Since the pandemic, one of the reasons for improved outlook of India Inc was the deleveraging story. But if the profitability continues to remain pressured for the rest of the year, this factor may come into focus again. Interest coverage ratio had been ascending from 4.2x in mid-FY21 to 6.2x at the end of Q4 FY22, but it has contracted to 4.9x currently. This is even before most companies’ debt terms have reflected the higher interest rate trends that started only in Q1 FY23. The high capex plans announced, if unchanged, combined with higher debt-financing costs, on a shrinking profitability base can have a large enough impact. Capital-intensive sectors like cement and steel have a comfortable ratio of 6.7x and 5.7x respectively, but are 30 per cent lower than only the previous quarter. Automobile sector’s interest coverage ratio was at 1.7x in Q1 FY23, down from only a marginally comfortable range of 2.8x in Q4 FY22. Tata Motors, Ashok Leyland and TVS Motors could improve their financial leverage position as the recovery in Auto demand plays out.

Sectoral breakdown

The results analysis has some pointers towards a negative outlook owing to cost inflation. Some respite has been evident in input materials led by metals including steel. Even as other commodity costs remain volatile in the short term, the demand pick-up should aid most sectors. Going beyond reported numbers, the sectoral commentary on results performance has been positive. Here’s the outlook for key sectors which have faced strong cost headwinds in recent times.

FMCG

According to Nielson research, post-Covid FMCG growth has been price-led with flattish volume growth over a three-year period. In Q1 FY23, industry leaders such as HUL, Nestle and Dabur reported a strong price growth (12-15 per cent year-on-year) and lower volume growth (3-4 per cent year-on-year). The partial pass-through of the raw material inflation (15-20 per cent year-on-year) resulted in gross margin contraction of 240 basis points year-on-year in the sector. The only solace witnessed in prices by July-August 2022 has been from edible oils and packing materials to an extent. The subdued volume growth of the last three years should provide a softened base for volume growth when cost savings, if any, are passed on.

While the short-term outlook grapples with cost issues, the longer-term outlook is built on premiumisation and rural growth. Beyond price and volume, the industry is also aiming for higher contribution from premium product mix (HUL and Godrej Consumer products) and a stronger rural push (Nestle). The lack of downtrading even in high-cost inflation period points towards a strong demand environment and accordingly should support the next leg of growth, according to companies.

Automobiles

The demand outlook for Autos led by four-wheelers is strong. While the continuing chip shortages have created supply challenges, this is adding to the already-strong order book position of the companies. The industry has been able to reasonably pass on the higher commodity prices of Q4 FY22 (primarily steel) with 100-200 basis points price increases. Even so, the margins are under pressure owing to higher marketing spends and lower utilisation due to chip shortages in some cases. The 20 per cent correction of steel prices during March-August 2022 should be reflected in the second half of the year.

The demand for SUV vehicles has increased along with demand for many features (vehicle type, design and convenience). This is reflected in the product mix as well, driving higher realisations for companies. Led by launch of new models in the SUV category the topline growth should be led by higher volume and price realisations even as cooling input prices are passed on. Industry leader Maruti Suzuki is continuing with their capacity expansion plans unabated to serve increased demand.

The CV (commercial vehicle) market is also in the midst of a cyclical recovery in demand. The rural demand outlook is still weak which is reflected in bike sales with recovery dependent on better monsoon. The export market, even if diverse enough, is under systematic global stress leading to volatility in sales.

Cements and Paints

Supplying to the construction industry, paints and cements face varying prospects. Energy-intensive cement industry faced 50 per cent year-on-year energy cost inflation along with other raw material inflation in Q1 FY23. The cement industry passed on the higher costs through price increases varying from 25 per cent to 50 per cent year-on-year. The high cost pass-through impacted volume growth leading to weak revenue growth in the quarter. The energy costs (petcoke, crude and derivatives) have marginally eased currently compared to Q1 FY23. This should bode well for volume off-take. In the longer term, demand growth expectations are still high reflected in the capacity addition plans of companies. For example, UltraTech and Shree Cement expect to add capacity in the near term.

The paints industry continues to face strong growth as evidenced by the leader Asian Paints and other participants reflecting similar growth. The sector managed both volume and price growth as total revenue reported 14 per cent quarter-on-quarter growth in Q1 FY23, even after passing 300-400 basis point price increases in the quarter. The gross margins, nonetheless, declined marginally, but better control of employee and other costs controlled the impact on EBITDA margins. The softening of crude derivatives is expected to flow through to base chemicals, then to specialty chemicals before softening solvents costs which should aid the paints industry. This implies a gradual benefit from lower current crude prices. The improved product mix in tier-1 and tier-2 centres for Asian Paints is offsetting to an extent the weakness in remaining centres, which are also expected to pick up shortly.

If high interest costs don’t play spoilsport, the recovery in real estate demand, continued growth in affordable housing and government push on infrastructure should act as tailwinds in institutional demand for both paints and cements industry.

Information Technology

The top-line growth continues unabated for IT majors at 20 per cent year-on-year. The sequential growth from Europe was weak across most companies, while North American growth continues. The outlook commentary for the primary region (North America) can be characterised as positive with only a few qualifications as of now. Either growth of budget allocation or speed of deal finalisation are the visible sore spots. This implies a slight headwind for growth in book to bill ratio. While S&P earnings across US companies continue to grow, consumer facing industries are showing signs of stress. Infosys recently announced weakness in mortgage segment and there has been a slew of earnings revision in retail including Walmart in July 2022. A strong recovery from recessionary overhang in the US will be required by IT industry to overcome any lingering doubts on its sectoral outlook.

IT services majors reported 100-200 basis point EBITDA margin decline as primarily employee costs increased with further increases pending in Q2 FY23. Other costs, including subcontracting and normalisation of travel and visa expenses, have also impacted margins. The industry also reported a better scope for pricing growth in contracts based on cost-of-living index, trickling down in one or two quarters.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.