The Indian Rupee closed the financial year 2021-22 (FY22) on a weak note, touching a new low of 76.98 against the US dollar in March. Overall, the domestic currency fell 3.53 per cent against the US dollar in FY22 compared to a 3.32 per cent rise seen in the previous fiscal.

The Russia-Ukraine war, surging crude oil prices and the US Federal Reserve’s aggressive plan to hike rates in all its upcoming six meetings were the major factors that weighed on the rupee. However, the domestic currency averted the danger of weakening below 77 and has recovered well in the last few weeks, thanks partly to the Reserve Bank of India’s (RBI) intervention. The RBI had been using its strongly built-up forex reserves to cap the weakness in the rupee. Th central bank’s reserves have come down from $631.92 billion in the first week of March to $617.648 billion as on March 25, 2022.

However, the broader picture has not changed much. First, the Russia-Ukraine war remains an uncertainty in spite of the ongoing peace talks. Secondly, Brent crude oil prices are showing reluctance to step down below $100 per barrel. And three, the US Fed’s March meeting minutes, released last Wednesday, indicates that there could even be a 50-basis points rate hike in some of their upcoming meetings. Under this circumstance, can the rupee stay afloat against the US dollar? How far can the RBI go to avert a fall below 77? We look at those factors that are supportive of the rupee and those that are working against it.

Trade deficit to widen

Exports may cool off - India’s exports have been robust in FY22. According to the latest preliminary data from the Ministry of Commerce, India’s exports for FY22 have risen 43.18 per cent to $417.81 billion from $291.81 billion in FY21. Imports bill, on the other hand, has increased 54.71 per cent in FY22. The country’s total imports for FY22 stand at $610.22 billion, up from $394.44 billion in FY21. Higher imports leave us with a deficit of $192.41 billion in FY22. The odds seem stacked in favour of a further widening of deficit this fiscal.

For one, fear of a global growth slowdown, increasing talks of a recession cast doubts on whether India’s export growth can retain the momentum in FY23.

The US Federal Reserve had lowered its growth forecast for 2022 sharply in March after the Russia-Ukraine war started. The Fed expects the US to grow at 2.8 per cent, down significantly from its earlier forecast made in December 2021 to see a growth of 4 per cent.

Even prior to the war, major institutions such as the International Monetary Fund (IMF) and World Bank had forecast a global growth slowdown in 2022. The World Bank expects the world to grow at 4.1 per cent in 2022, down from 5.5 per cent in 2021. Similarly, the IMF has projected the world to grow at 4.4 per cent in 2022 as compared to 5.9 per cent in 2021.

Chances for the pace of India’s exports to slow down look quite high this year, pointing to a widening of the deficit.

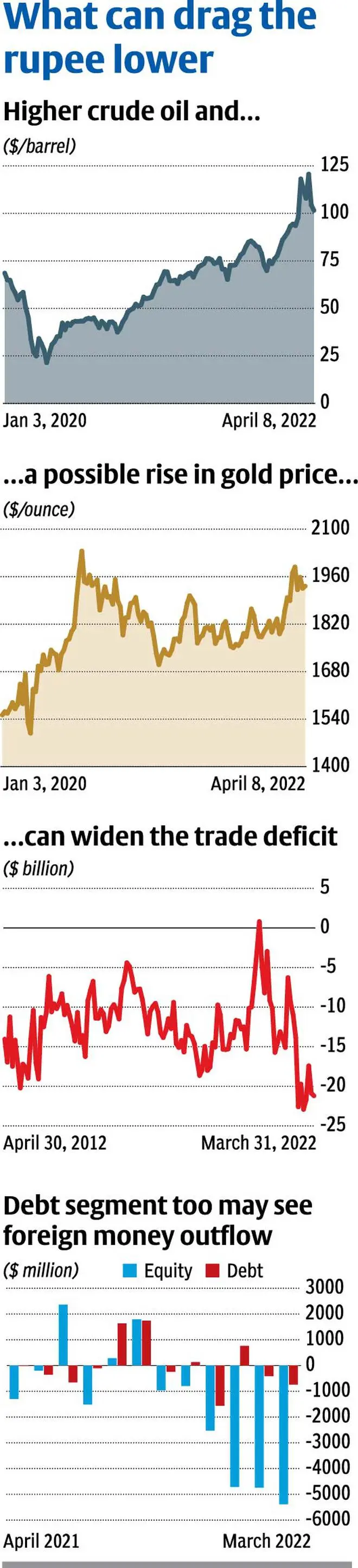

Headwinds from oil and gold imports - On the import side, oil accounts for about an average of 28 per cent of total imports. Brent crude prices spiked to $130 per barrel in the first week of March and have come off from there. The price is currently at $102.

The uncertainty over the Russia-Ukraine war and the fear of supply disruption can continue to keep the oil prices higher.

The fresh lockdowns in China, raising concerns of a demand slowdown, and the US announcing that it will release its strategic reserves have not been able to drag the prices below the $100 mark yet. Unless oil prices go below $90 per barrel, it is not likely to help India’s import bill. Overall, the charts show that the chances are high for Brent crude prices to stay in a broad range of $90-130 at least in the next two quarters. This can increase the oil bill for FY23 and, in turn, increase the trade deficit further.

Adding to this is the rise in gold prices. Gold is the third largest import component and accounts for an average of 8 per cent of the total imports. High inflation and safe-haven status on the back of the Russia-Ukraine war can keep gold prices higher this year. The charts show that gold, currently at around $1,920 per ounce, has the potential to rise towards $2,100 in 2022. This will add more to the import bill and the deficit.

Takeaway: Higher crude oil and gold prices can increase the import bill in FY23. This, coupled with a possible slowdown in exports, will result in the trade deficit widening further. That will be negative for the rupee and can result in the domestic currency weakening against the US dollar in FY23.

Slowdown in foreign money flows

FDI/equity flows fare poorly - Going by the latest available data until December 2021, foreign direct investment (FDI) into India seems to have slowed down in FY22. Data from the Department for Promotion of Industry and Internal Trade show that the total FDI in FY22 (up to December) stands at $60.591 billion. The FDI into equities, which forms a major part of the total flow, has been $43.175 billion, down 16 per cent over the same period in the previous year. FDI into equity account for an average of 70 per cent of the total FDI flows into the country.

Foreign portfolio investors (FPIs) have been pulling money out of India equities since October last year. The sell-off intensified from December. In FY22, the Indian equity segment has seen a net outflow of $17.68 billion, compared with an inflow of $37.75 billion in FY21. The debt segment saw a slight inflow of $185 million in FY22 after witnessing an outflow of $6.71 billion in FY21.

Wider trade deficit and slowdown in foreign money flows have resulted in the current account running into a deficit in FY22. As per the recent data release from the RBI, the current account deficit for April-December 2021 stands at 1.2 per cent of GDP. The current account was in surplus of 1.7 per cent over the same period in the previous year.

Stronger debt outflow expected - The debt segment, which saw a mild inflow in the last fiscal, looks vulnerable for a strong outflow this year. Surging US Treasury yields, coupled with an aggressive rate hike plan from the US Federal Reserve, can see money outflow from the emerging markets. A comparison between the FPI flows into the Indian debt segment and the Treasury yield over the years shows that there have been strong outflows at times when the yields hover at their peaks.

The minutes of the Fed’s March meeting released last week indicated that there are possibilities of seeing a 50-basis point rate hike from the central bank in the upcoming meetings. Also, the Fed will start reducing its balance sheet at a pace of $95 billion per month possibly from May.

Takeaway: The risk of foreign money outflows from the debt segment and the aggressive rate hike plan from the US Fed are negative for the rupee.

Fed hikes to strengthen dollar

The tone of the US Fed recently has turned completely more aggressive than earlier. There were hopes that the Fed could go little slow in its rate hike on the back of the Russia-Ukraine war. But the Fed seems to be more worried about high inflation rather than geopolitical tensions. Indeed, as seen from the Fed’s recent projections, the central bank has accounted for a slowdown, which has reflected in the growth forecast being revised lower.

The US dollar can gain from the rate hike cycle that has begun with a 25-basis point increase in March. The US dollar index, currently at 99.5, has been moving up gradually since June last year. It has a potential to target 101-102 in the coming months.

Takeaway: As the dollar index rises, the Reserve Bank of India might stay out of the market and allow the rupee to weaken rather than using its forex reserves to limit the fall.

To sum up, all the above factors can keep the rupee weak in this fiscal. The recent recovery in the domestic currency against the US dollar could be short-lived and is likely to be limited. A fresh fall in the coming months may have the potential to take the rupee to 78 and even lower in this fiscal.

What do the charts say?

The Indian Rupee (USDINR: 76.05) has been structurally on a downtrend against the US dollar. Though it has recovered slightly from the new low of 76. 98 against the greenback that it plunged to in March, the bigger picture still remains weak for the rupee. The recent recovery is likely to be short-lived and a fresh fall is likely going forward.

Short-term outlook: The short-term view is positive for the rupee. The currency has room to strengthen further in the coming weeks. Key supports are at 76.20, 76.50 and 76.80. As long as the rupee sustains above these supports, the chances are high for it to strengthen towards 75 and even 74.50 in the next couple of months. In case the rupee manages to break 74.50, the upside can extend up to 74.20 and 74. A fresh fall either from 74.50 itself or from 74, can take the rupee lower again towards 76-76.50 levels.

Overall, 74.50-76.50 (narrow) or 74-77 (broad) can be the range of trade for the next three months at least. The chance of an extended sideways consolidation in the above-mentioned range for even up to six months cannot be ruled out.

Long-term view: The downside is likely to be limited to 74 even if the rupee manages to break above the short-term support level of 74.50 mentioned above. Clusters of trendline and moving average supports in the 74.50-74 region makes it a very strong support zone. Rupee will need a strong trigger to break above 74. Considering the current situation of the geo-political tensions and rising interest rate scenario in the US, any new trigger looks less likely. As such the rupee is more likely to remain below 74 in the coming months.

Key support to watch will be the broad 76.50-77 region. A strong break below 77 will see the rupee weakening to 78-78.50 initially. Thereafter, a short-lived recovery towards 77 and a sideways consolidation between 77 and 78 or 77 and 78.50 is a possibility for some time.

Thereafter, the rupee is more likely to break below 78 and extend the fall to 80-80.50 by the end of this calendar year or in the first quarter of 2023.

Weak rupee’s impact on common man

From the equity market perspective, sectors that are export oriented such as IT and pharma can be gainers from the weakness in the Indian rupee. Rising commodity prices coupled with the rupee weakness can help the domestic metal producers as well. On the other hand, manufacturing companies, which have a big import component for their inputs, will face pressures from rupee depreciation.

Travelling and education abroad will become costlier for the a common man. The cost of airline ticket and the expenses abroad will increase.

The loan to be availed for education abroad can go up as the rupee weakens. That is, assume your course fee is $50,000 and the rupee exchange rate is at 75. So now you would require a loan of ₹37.5 lakh to cover the fees. When the rupee weakens to 78, this loan amount will increase to ₹39 lakh to cover the same $50,000-course fee. On the other side, those students who would have taken a loan at around ₹74 per dollar can benefit at the time of repayment when the rupee weakens to 78.

Electronic gadgets such as laptops, mobile phones can become costlier. This is because the accessories to manufacture these goods are imported from other countries. So, this will increase the manufacturing cost which, in turn, can be passed on to the customers.

The major winner of a weak rupee will be the families of Non-Resident Indians (NRIs). A $1,000 transferred today at say ₹75 per dollar will give ₹75,000. The same $1,000 will give ₹78,000 when the rupee weakens to ₹78 per dollar in the coming months and ₹80,000 when the exchange rate goes to ₹80 per dollar.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.