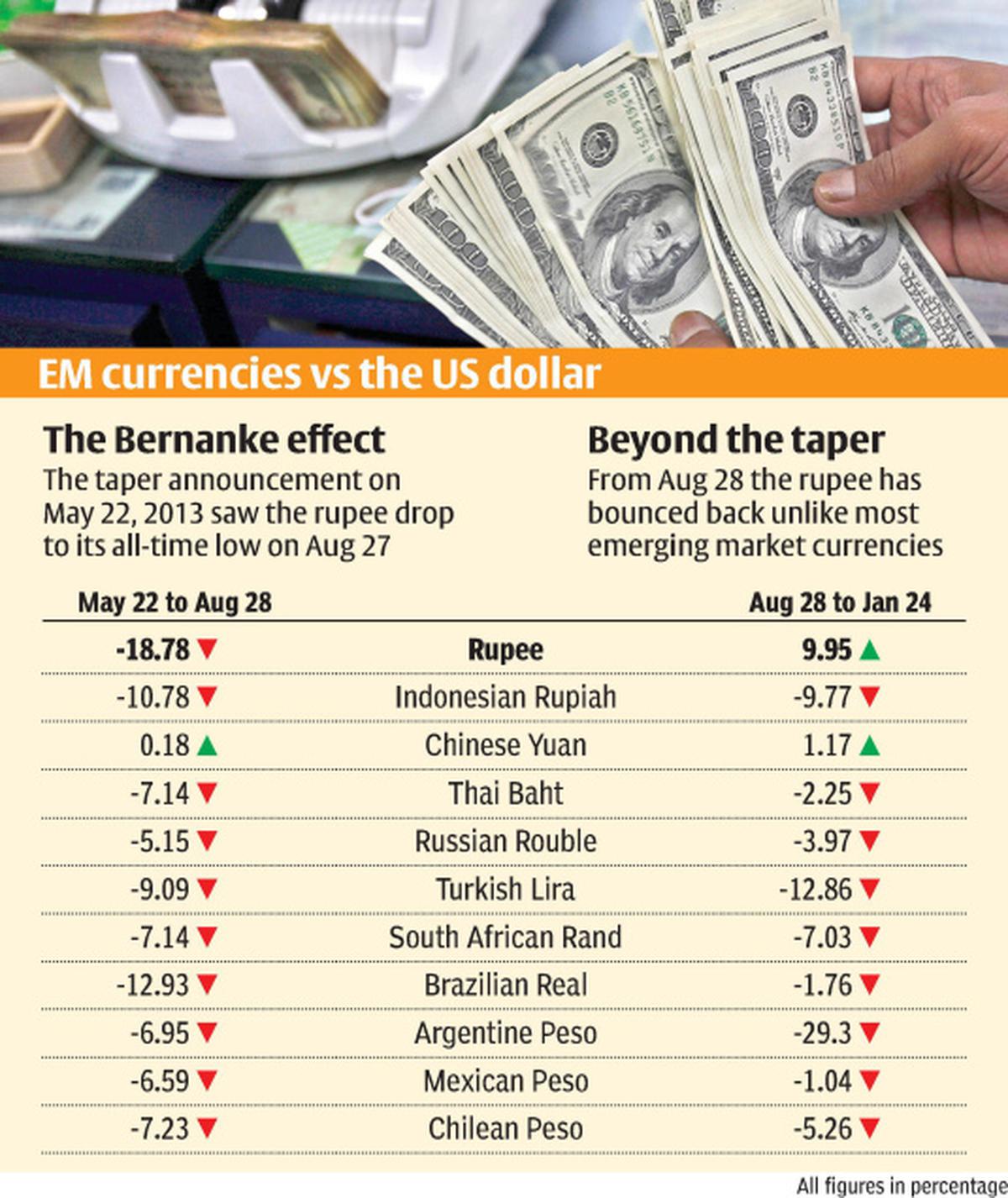

The rupee was the worst-performing emerging market (EM) currency from May 22, 2013 when Ben Bernanke first talked of tapering the US Federal Reserve’s monthly bond-buying programme, through August.

But since then — after hitting an all-time low of 68.36 against the dollar on August 28 — it has gained almost a tenth, trumping every other EM currency.

Even taking the entire period from May 22 to January 24, the rupee has been among the better-performing currencies, with a cumulative loss of 10.7 per cent, below only the Chinese Yuan, the Mexican Peso, the Russian Rouble and the Thai Baht (see table).

Deft management Vikram Murarka, Chief Currency Strategist at Kshitij Consultancy Services, attributed the rupee’s strengthening to the Reserve Bank of India’s deft demand-and-supply management of the currency since September.

While the market demand from oil importers was removed by opening a special dollar-swap window for them, the demand from gold importers was curbed through various curbs, including a requirement to re-export a fifth of every consignment brought in.

The supply side was managed by offering a 3.5 per cent per annum concessional swap facility for dollar funds through non-resident deposits and overseas capital mobilised by banks. This window raised some $34 billion.

Only a correction However, Pramit Brahmbhatt, CEO of Alpari Financial Services (India) Pvt. Ltd, felt that the rupee’s appreciation since September was only a correction of its previous very sharp (almost 20 per cent) depreciation.

“The measures by the RBI have helped, but the rupee has started weakening again over the last two sessions. We expect this weakness to continue,” he said.

But how does one still explain the rupee cutting its losses over a longer period relative to most EM currencies?

While a reduction in India’s spiralling current account deficit has certainly been a factor, there are some who believe the country’s relative lack of dependence on exports to China may work in its favour.

The China factor China is a major importer of coal, iron ore, copper, chrome and soyabean from many EM economies, whose currencies are bearing the brunt of China’s growth engine showing signs of sputtering.

“The China-powered super-cycle in commodities is finished. China was the world’s largest construction site. It demanded steel, metals and all the rest of it. But now it is moving away from that,” is how Geoff Lewis, Executive Director of JP Morgan Asset Management, put it in a recent interview to Business Line .

India is relatively insulated from China’s slowdown, as its merchandise exports are just a quarter of what it imports from the dragon.

Further, a weakening of the Chinese demand, as indicated by a contraction in the HSBC Purchasing Managers Index in January, even benefits India by lowering global prices of crude oil, coal and all other commodities it now heavily imports.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.