Indians’ love for savings bank accounts continues unabated, but for the first time, mutual funds have edged out FDs/RDs in terms of investor preference, according to the 2022 BankBazaar Savings Quotient. A lower proportion of women have direct stocks compared to men, but oddly, the percentage of women in riskier investments is also much higher. Meanwhile, rainy day concerns continue to motivate Indians to save. The study is based on a survey conducted on 1,675 salaried repondents aged 22-45 years. Here are the key findings.

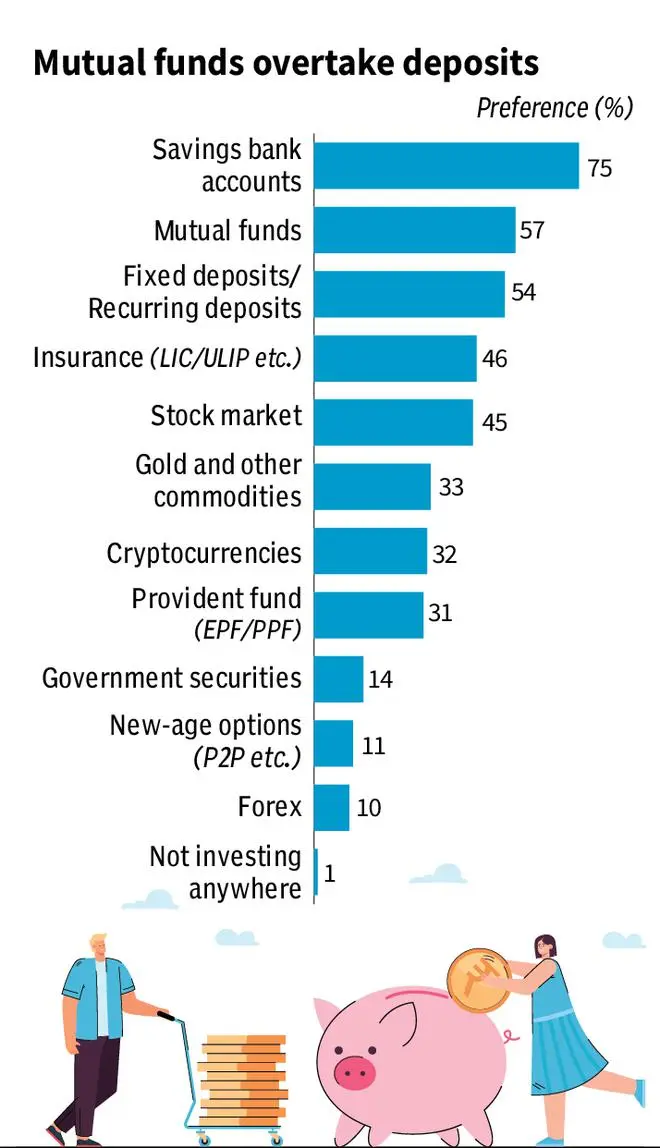

Look who’s beating deposits

This year, for the first time, more Indians said they are saving through mutual funds than fixed or recurring deposits — a minor gap which may expand over time.

About 57 per cent of respondents had mutual funds / SIPs running, compared with 54 per cent with FDs. Investment in low-return products such as endowment plans also remained high, with close to 46 per cent respondents invested in them.

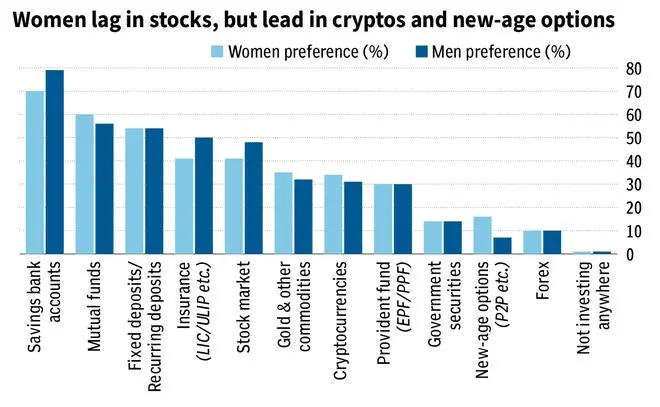

Women take the lead

Women are saving more actively then usually perceived. More women hold mutual fund investments – almost 60 per cent – compared with men 55 per cent. About 54 per cent women have FDs, compared with 53 per cent of the men. However, the percentage of men investing directly in stocks – 48 per cent – is much higher than women, only about 41 per cent.

But oddly, the percentage of women in riskier investments is also much higher. About 34 per cent have crypto investments, compared to 30 per cent of the men. About 16 per cent have invested in new age savings tools such as P2P, compared to about 7 per cent of the men

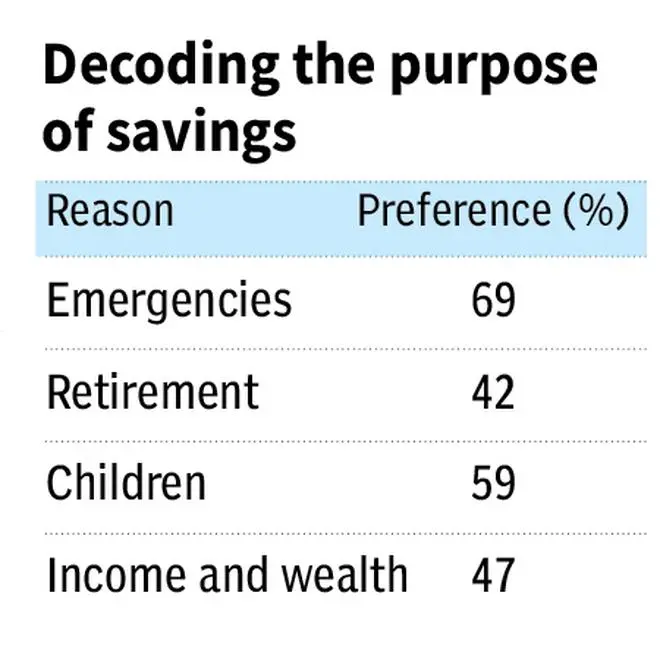

Why does India save?

Post-Covid, as savings reduced, saving for emergencies such as hospitalisations was the main reason to save across the board.

This was closely followed by children’s well-being and inheritance.

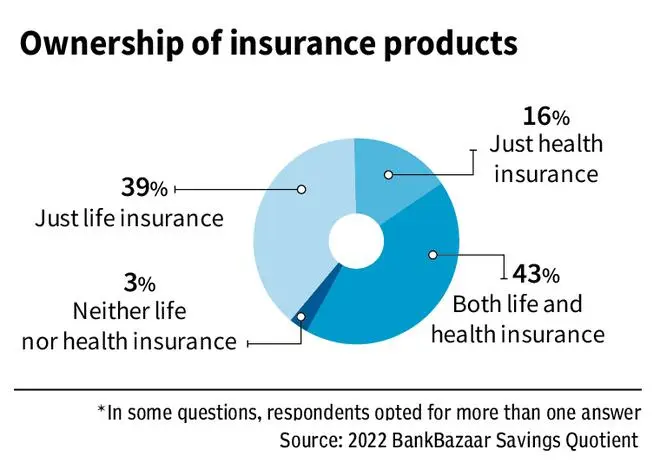

Covering well

Data shows only 3 per cent have no health or life insurance. About 43 per cent have both health and life insurance and 39 per cent have life insurance without a health cover. The splits are pretty even across age groups.

Reading this with the high investment numbers in traditional endowment plans, it seems plausible that most of these are not high-value pure term plans, but a mix of term and endowment plans. This points to a need for better understanding around insurance and its place in one’s financial life.

Graphics: Visveswaran V

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.