Though funds focusing on the growth style of investing have outperformed the last decade, the tide is now turning in favour of value investing. Rising interest rates are triggering a reduction in equity multiples and input cost inflation is threatening earnings growth. In this situation, stocks trading at low to moderate valuations offer a higher margin of safety for investors. This makes value and contra funds a good choice, both for investors looking to add new equity funds to their portfolio, and those already owning growth-heavy portfolios.

SBI Contra, a 23- year-old equity fund, is a good buy given its significant outperformance of its benchmark and peers in the last five years, its differentiated low PE portfolio and focus on out-of-favour stocks and sectors.

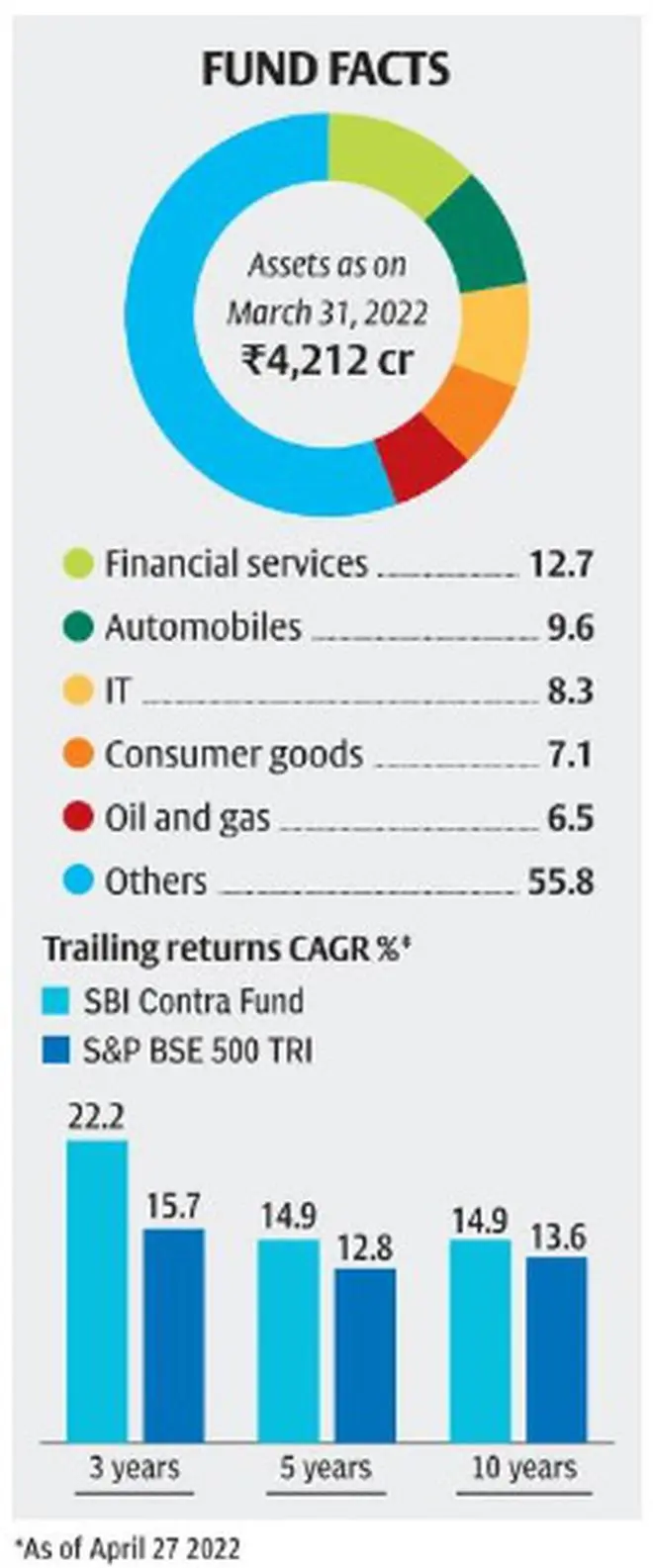

Performance improvement

The value and contrarian styles of investing are generally better evaluated over multiple market cycles, given that the value and growth styles outperform at different stages of the market cycle.

Of the 22 value-oriented funds in the market, only 10 have a 15-year record.

SBI Contra Fund, after being a middling performer earlier, has pulled ahead of peers in the last five years. This has lifted its CAGR since inception to 18.9 per cent. The fund’s regular option has delivered a 15 per cent CAGR in the last five years against 11.3 per cent for the value funds category and 12.8 per cent on the benchmark S&P BSE 500 Index.

Over a decade, on a one-year rolling basis, the fund has beaten its benchmark about 53 per cent of the times with average returns at 16.8 per cent. The fund gained 122 per cent in its best year, while losing 36 per cent in its worst year.

Value leanings

Though both contra and value funds are bucketed in the same category, the two strategies are not the same. Value funds try to pick stocks trading at a discount to their intrinsic value or the market, while contrarian funds hunt for stocks that the markets currently dislike. Therefore, contra funds need not necessarily own a low PE portfolio.

But despite its recent outperformance, SBI Contra owns a reasonably-valued portfolio. By end-March, its portfolio PE was about 17 times, at a significant discount to its benchmark - the S&P BSE 500’s PE of over 24 times. Other contra funds tend towards stocks trading at higher valuation multiples with Invesco Contra reporting a portfolio PE of about 25 times by end-March, while Kotak Contra featured 22 times.

The presence of more reasonably-valued stocks in the SBI Contra portfolio makes for a better risk-reward equation for long-term investors entering now.

Differentiated portfolio

In the Indian context, funds labelling themselves as contra or value do not necessarily stick stringently to their mandates. But SBI Contra in recent times has adhered to its mandate of owning out-of-favour stocks and sectors. Four of its top five holdings of GAIL, HCL Technologies, Tube Investments, ICICI Bank and Neogen Chemicals were, for instance, materially different from the ICICI Bank, Reliance, Infosys, HDFC Bank, SBI held by both Kotak Contra and Invesco Contra as their top exposures.

SBI Contra’s sector choices by end-March were also significantly different. Financials were just a 12 per cent exposure in the portfolio, with autos (9.6 per cent), IT (8.3 per cent), consumer (7 per cent), oil and gas (6.5 per cent) being the main sectors held. Other contra funds held higher weights of 24-25 per cent in financials and 11-13 per cent in IT.

Multi-cap approach

Today small and mid-cap stocks in the market offer more contrarian stock picking opportunities than the over-tracked and over-owned large-cap universe. SBI Contra follows a truly multi-cap approach with just a 34 per cent allocation to large-caps, 18 per cent to mid-caps and 25 per cent to small-caps by end-March 2022. It also holds mandates for foreign equity exposures and held cash to the extent of 7 per cent.

Negatives

Compared to other long-running funds in the category, SBI Contra tends to deliver higher returns in its good periods but suffers higher losses in the bad periods. The fund has delivered a 10 per cent plus return over 51 per cent of the times, but suffered losses 28 per cent of the times. Peers such as Invesco Contra and Kotak Contra have suffered losses 18 and 14 per cent of the times respectively. This makes SBI Contra suitable for investors with a higher risk appetite.

The fund owns rather fragmented positions with top holdings at not more than 4 per cent. This may prevent good bets from making a big difference to returns. The fund’s expense ratio is high at 2.11 per cent for the regular plan and 1.29 per cent for direct.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.