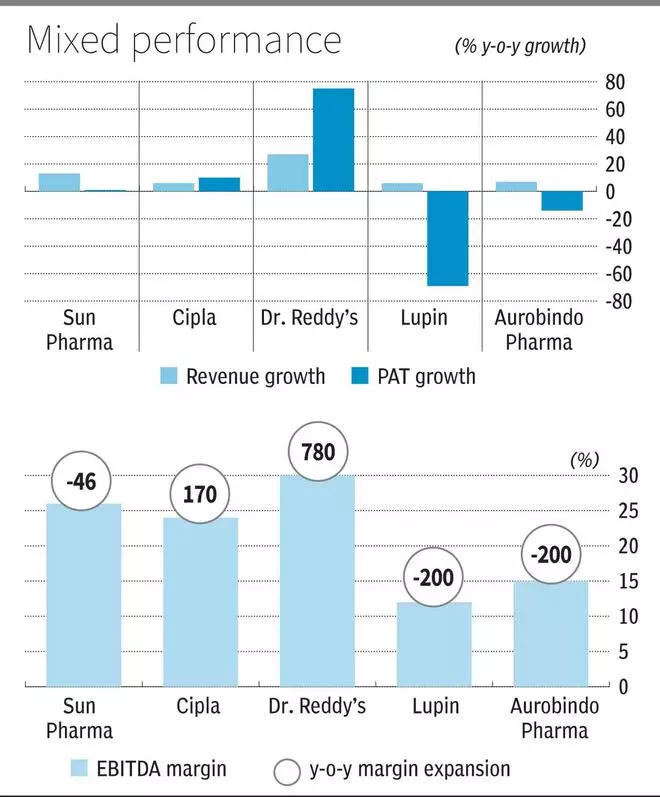

Top Indian pharma companies reported cumulative revenue/PAT growth of 12/2 per cent YoY in Q3FY23 results, as margins were weak across most companies. Amongst the leading companies (by market cap), Sun Pharma, Cipla, Dr. Reddy, the outperformance was driven by differentiated products in the US. For companies reliant on oral solid dosages (OSDs), including Lupin and Aurobindo Pharma, revenue growth indicated pricing pressure in the US. Indian segment performance was underwhelming across players. The sector outlook relies on better trends in India-branded generics and limited competition generics in the US.

Domestic performance

Overall Indian market growth at 7.7 per cent in Q3FY23 was weak. Sun Pharma (4.8 per cent YoY in India) and Lupin (3.3 per cent YoY) reported weak growth on account of loss of exclusivities, and Cipla reported a weak growth (1.8 per cent YoY) on account of the high Covid base effect. But investment in the geography through MR (medical representatives) addition, product launches, and product licensing continues to be on a higher note. Growth is expected to be higher (low double digits) in the following periods.

US market

In the US market, the saving grace continues to be a differentiated portfolio. The differentiation brought about by speciality, respiratory and regulated products has been re-emphasised this quarter as Sun Pharma, Cipla and Dr. Reddy reported US revenue growth of 16.6/42.3/63.9 per cent, respectively. The speciality portfolio continues to drive Sun Pharma, and new product acquisition is underway to expand the portfolio further. Concert Pharma’s Alopecia Areata treatment is the lead candidate in Phase-III trials, to be acquired for US$ 576 million plus additional contingent value by Sun Pharma.

gRevlimid sales have also aided the three companies. They are expected to contribute meaningfully in the medium term even as new players (Aurobindo by Q4FY24) enter at regular intervals due to the structuring of the agreement. Cipla’s approval process for gAdvair is progressing and is expected in the calendar year. Lupin’s gSpiriva target date has also been extended to FY24. In biosimilars, Sun Pharma and Aurobindo plan to expand the portfolio to target patent expiries in the second wave starting from 2025.

On the other hand, companies without much differentiated portfolio continue to face challenges. An OSD-heavy portfolio in the US, barely manages to grow, as was reported this quarter. Aurobindo Pharma (9.3 per cent YoY in the US) and Lupin (-3 per cent YoY) reported an improved quarter in the US as injectables fared better for Aurobindo, and pricing pressure was not cited as extraordinary in OSDs. Expectations for better pricing erosion in the US, cooling down to single digits, maybe early but are beginning to form as it has been a year of intense pricing pressure in the US for OSDs.

Margins under pressure

On the margin front, companies have reported input cost materials at elevated levels with some easing in logistics costs. Lupin and Aurobindo Pharma have reported a significant decline in EBITDA margins owing to the OSD portfolio in the US facing erosion. The revenue and margin support for Dr. Reddy and Cipla from gRevlimid is expected to moderate in the medium term as the product will face intense competition from 2026.

Amongst the leading companies, we had earlier given a positive view on Sun Pharma and Dr. Reddy, which are currently trading at 24.5 and 17.7 times FY24 earnings.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.