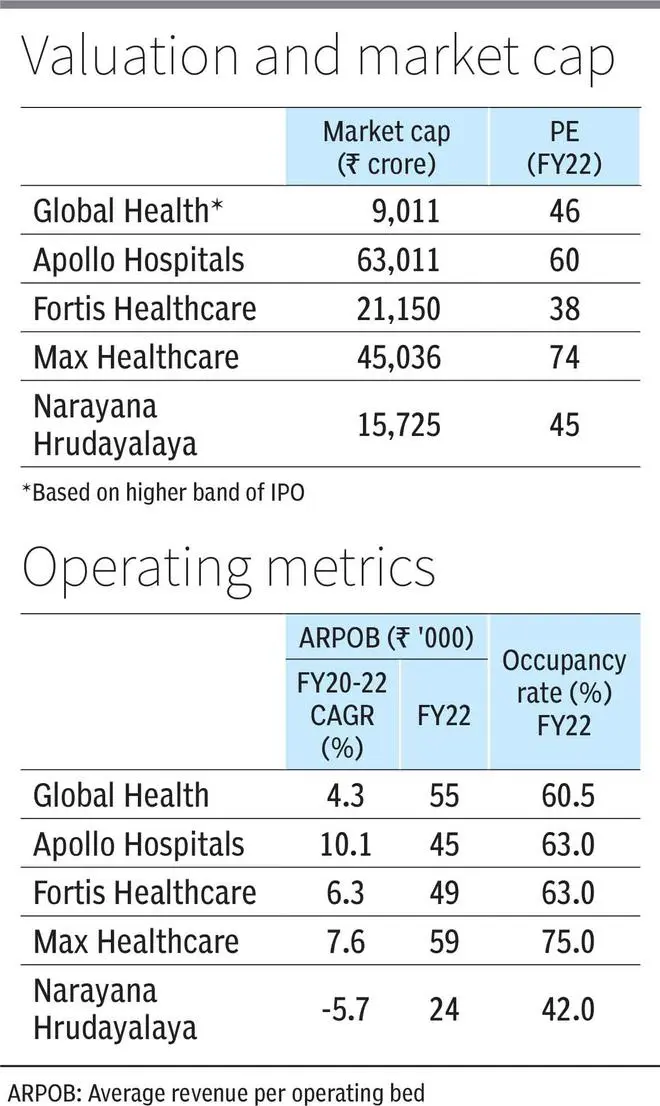

Global Health is the latest IPO from the healthcare services industry. The hospital sector has been re-rated post pandemic as they benefitted from the under penetration, improving affordability and higher insurance reach. Operating under the “Medanta” brand, Global Health operates five multi-speciality tertiary care hospitals in NCR and East India. The IPO is open from November 3–7, and is priced at 46 times FY22 earnings; comparable to industry peers. The IPO consists of fresh issue of ₹500 crore and OFS of ₹1,700 crore, where non-promoter (affiliate of Carlyle Group) is exiting and promoters and other shareholders, including a Temasek affiliate, continue to stay invested.

The long-term investors can subscribe to the issue as the Medanta brand continues to expand into regions where its brand recognition pays off.

Strong track record

Global Health has 2,467 installed beds as of June, 2022. Opened in 2009, its flagship hospital in Gurugram now functions with 1,391 operational beds. Indore (175 beds) and Ranchi (200) were later added in 2014 and 2015 constituting the established centres of the group. Lucknow (473) and Patna (228) are the developing centres, opened and operating since 2019 and January 2022, respectively. Lucknow has achieved EBITDA breakeven in FY22. Noida centre, with a planned capacity of 550 beds, is expected to be commercialised by 2025.

Founded and led by Dr. Naresh Trehan, a successful cardiothoracic surgeon, Medanta has built a strong brand in the region. The hospital chain operates at industry-leading AROPB of ₹59,000 (Average revenue per operating bed) driven by its focus on complicated cases in cardiology, oncology, gastroenterology, nephrology, and other departments. The management notes that the higher realisations are not driven by tariffs, which may rank it third or fourth when compared with peers, but by the product mix of complex procedures.

Operating and expanding in the North and East clusters, the branding is expected to benefit the institution. The hospital could benefit from the likely industry growth of 13-15 per cent CAGR for FY23-26 (as per CRISIL Research), especially from the Tier-II centres.

Growth drivers

The next three-year top line growth will be driven by capacity additions and price hikes. In the established centers, Global Health expects a low single-digit growth with addition of 100 beds in Gurugram. In developing centres such as Lucknow and Patna, 400-500 excess beds will drive growth. The company plans Noida centre to be operational by 2025 with 550 beds. The developing centers revenue contribution should increase to 25 per cent in the next three years from the existing 18 per cent in FY22, with strong 10-15 per cent CAGR growth in bed capacity.

ARPOB declined 5 per cent to ₹47,700 in FY21 in the pandemic year and recovered to ₹58,900 in Q1FY23. While the established centres reported an average ARPOB of ₹59,300, developing centres too reported a similar range (₹56,500). ARPOB growth in developing centers can be sustained by price hikes in line with the historical range of 5-6 per cent (held-back for last two years by the company). Overall, the company can generate low double-digit top line growth in the next three years, driven by volume and price.

During FY22 and Q1FY23, the EBITDA margin increased to around 21 per cent from 13 per cent in FY20. Developing centres turned profitable (FY20 loss to 20 per cent in FY22) along with cost-control measures across the group (flat growth on employee costs in FY20-22 against 20 per cent topline CAGR). Even as employee costs recover along with higher input material costs, Global Health should sustain margins in 21-22 per cent range. Along with price increases, improving occupancy at developing centres (estimated at 49 per cent in FY22 against 62 per cent for established centres) is another lever to improve profitability. The return of international medical travellers is an additional lever for profitability. This segment’s contribution improved to 5.5 per cent in Q1FY23 from 3.6 per cent in FY22 compared to 11.2 per cent in FY20.

Financials and valuation

With Lucknow and Patna centres aiding volume growth of 14 per cent, Global Health has reported ₹2,205 crore revenue in FY22 (FY20-22 CAGR of 20 per cent), along with ARPOB growth pitching in. The EBITDA margin saw a strong improvement as operating leverage kicked in. The company reported a 800 basis points improvement in EBITDA margin to 21 per cent in FY22, which supported the 130 per cent earnings CAGR in the FY20-22. The current debt of ₹850 crore in FY22 (net debt to EBITDA of 0.7x compared to 1.9x in FY20) will further decline by ₹375 crore as fresh issue proceeds will be utilised to repay the debt. The Noida centre funding may again increase the debt level which is likely to cost ₹700 crore.

In the next three years, investors can expect continued expansion of Patna, Lucknow and Gurugram centres along with addition of Noida starting from 2025. A good top line growth combined with marginal growth in operating margins and improvement in interest costs, supports the high valuations (post-issue valuation of 46 times the FY22 earnings).

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.