Investors with a two-to-three-year horizon can consider investment in the stock of India’s largest defence aircraft maker, Hindustan Aeronautics Limited (HAL).

Incorporated in 1940 and nationalised in 1942, HAL has a strong portfolio of products ranging from fighter jets, helicopters to other components such as radar systems, radio navigation equipment, missile inertial navigation, etc, to name a few. The company also derives service revenue for maintenance of aircraft and helicopters, sales of spares and accessories.

Investment rationale

Robust order book, indigenisation of defence manufacturing and higher defence spending by the Government are expected to bode well for the company. The stock currently trades at an attractive 15.2 times its trailing twelve-month earnings. We believe the stock to be an interesting investment idea for four reasons.

First, HAL, which is the pioneer in defence aircraft manufacturing and maintenance, boasts of a strong order book. The company’s order book as of February stood at ₹84,000 crore, according to the management. In March, Defence Minister Rajnath Singh and the Defence Acquisition Council announced proposals worth ₹70,000 crore for purchase of defence equipment. This includes 60 UH Marine choppers from HAL to the tune of ₹32,000 crore, which is in addition to the order book.

The Government’s resolve to strengthen domestic manufacturing capabilities under the Atmanirbhar scheme will continue to benefit defence-focussed companies, including HAL, both in the near term and medium term. According to the management, there is an additional ₹20,000-crore-worth order that is under discussion and will materialise soon.

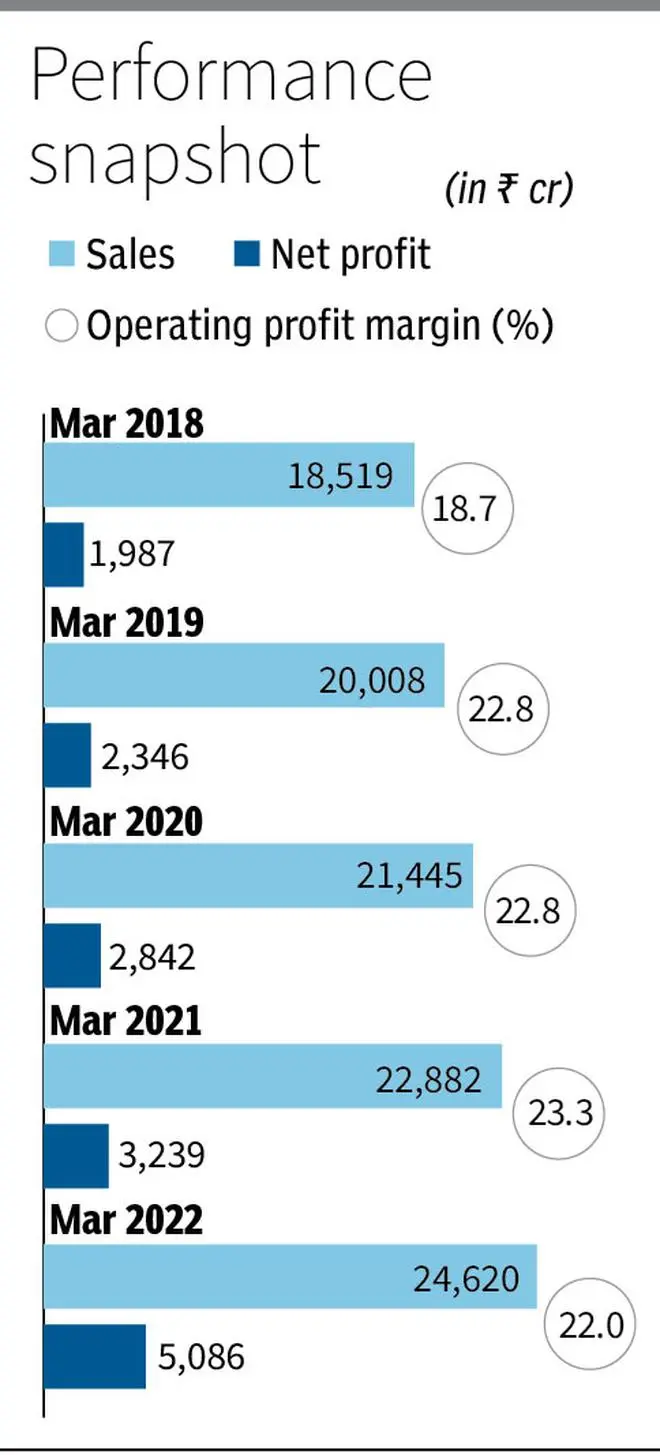

HAL had reported revenue of ₹24,620 crore in FY22. The current order book of ₹84,000 crore and new defence order of ₹32000 crore is about 4.7 times its FY22 revenue.

Second, the company is expanding its wings outside India. India is strengthening its manufacturing capabilities in the defence space, not just to reduce dependence on imports but also to position itself as a reliable exporter. The country is eyeing exports of $5 billion by 2025 and companies such as HAL will play a large role in India firming up its position as a leading exporter of defence technology and goods.

According to HAL’s management, the company is in discussion with Egypt, the Philippines, and Argentina for supply of aircraft and helicopters. HAL has offered 15 LCA Mk-1 to Argentina, 20 LCAs to Egypt, and six helicopters to the Philippines.

These should further add to the order book and revenue visibility over the next 3-5 years. Besides offering higher margins, exports will help the company geographically diversify its customer base and also reduce dependency on the Indian defence industry, even as the latter will continue to remain an integral part of HAL in the foreseeable future.

Third, a strong balance sheet with zero debt and strong operating cash flow generation further adds to the strength of the business. As of September 2022, the company did not have any borrowings.

Thanks to the improvement in its working capital, the company in the April-September 2022 period managed to clock operational cash flow (after working capital adjustments) of ₹3,309 crore as compared to a post-tax profit of ₹1,841 crore, for the same period. It had cash of ₹16,783 crore, which is almost 18 per cent of its market capitalisation of over ₹92,000 crore. This is higher than the ₹14,344 crore cash in the books as of FY22.

The stock trades at an impressive 15.2 times its trailing twelve-month earnings. Given the management’s guidance of 10-15 per cent growth, the stock is currently available at 13.2 times and 11.5 times its estimated FY24 and FY25 earnings. Given the company’s strong moat and robust order pipeline, we believe HAL to be a good investment opportunity from a two-to-three-year horizon.

While the order book is impressive, timely execution will be critical for HAL to sustain the growth momentum. While the reduction in the company’s cash conversion cycle over the last few years — from about 996 days in FY19 to 581 days in FY22 — is suggestive of improving execution and reduction in inventory, continuing the trend of working capital efficiency and execution will be critical to the stock’s performance.

In the nine-month period ended December 2022, the company reported revenue growth of 10.5 per cent to ₹14,433 crore compared to ₹13,062 crore in the 9MFY22 period. Operating profit grew faster at 17.2 per cent to ₹3,420 crore for the April-December 2022 period, compared with ₹2,918 crore in the same period last year.

The company reported operating margin of 23.6 per cent for the 9MFY23 compared to 22.3 per cent in the 9MFY22 period. Besides strong operating performance, sharp jump in other income also helped the 50 per cent jump in Net profit to ₹2,969 crore for the 9MFY23 period, vis-à-vis ₹1,984 crore in the same period last year.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.