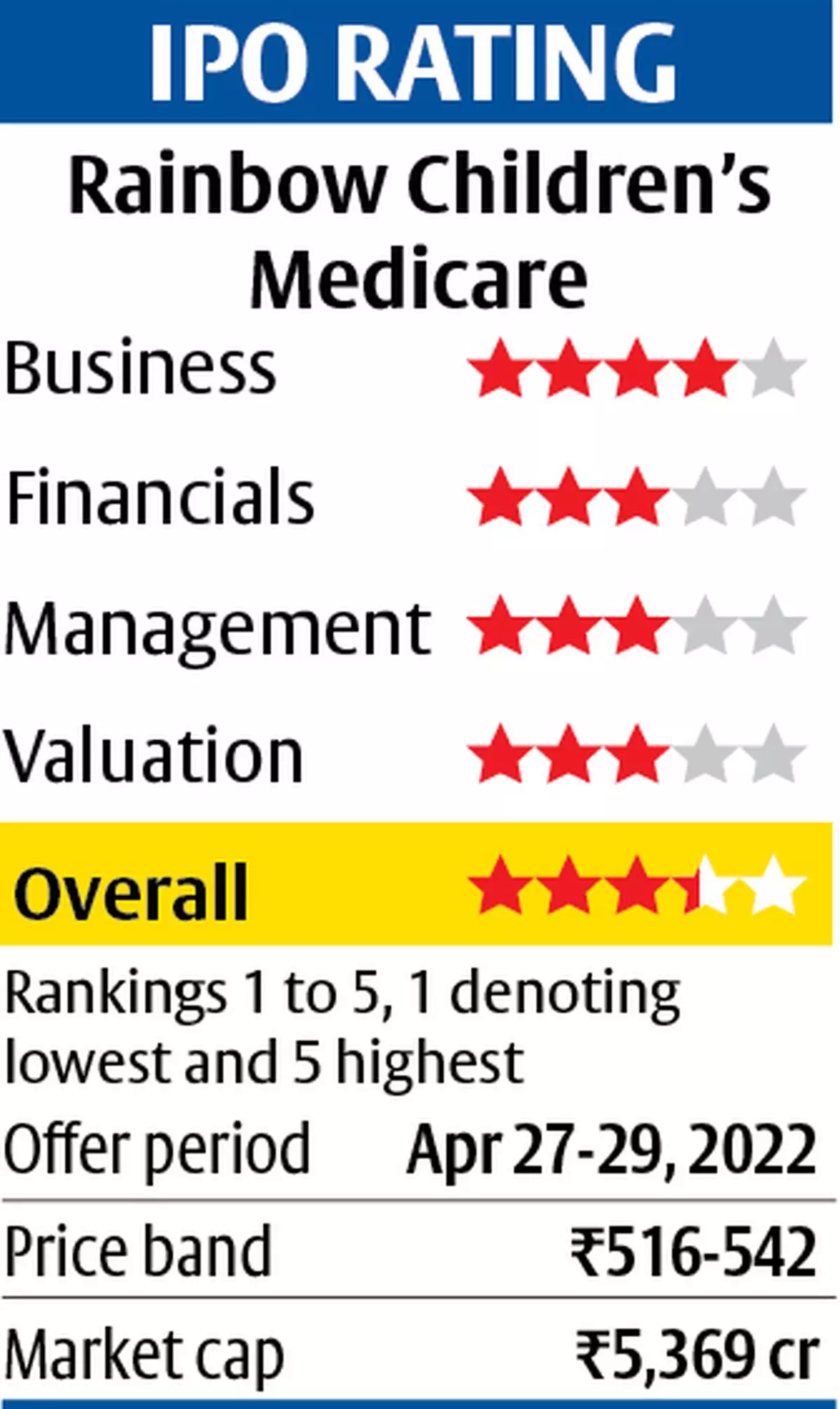

Rainbow Children’s Medicare (Rainbow) is a paediatric-focused multi-speciality hospital. It extended into Obstetrics and Gynaecology, primarily to provide care continuum in childcare. The Hyderabad-based hospital with 1,500 beds in 14 hospitals across four major cities, occupies a limited competition niche in advanced childcare. The IPO, valued at 31 times (annualised) 9MFY22 earnings, is priced fairly. It is comparable to valuation of KIMS (Krishna Institute of Medical Sciences) and is reasonably below larger peers such as Narayana Hrudayalaya, which trades at 40 times. Investors can subscribe to Rainbow IPO which is offering differentiated growth opportunity in a crowded healthcare market.

The IPO consists of ₹1,300 crore in OFS portion, of which 60 per cent is from institutional investor (British International Investment) and 36 per cent, promoter group. The fresh issue of ₹280 crore will be utilised for repayment of NCDs (₹40 crore) and expanding spokes in places with established main hospitals (hubs) - Hyderabad, Chennai, Bengaluru, and NCR region with an outlay of ₹170 crore.

Paediatric multi-speciality

Rainbow is differentiated from adult multi-speciality operators at one end and boutique mother-child care centres at the other. Rainbow’s Hyderabad hub offers 25 specialities, Bangalore - 16, Chennai and NCR - 10 each, across paediatric surgery, cardiology, oncology, nephrology, and other relevant disciplines. The 470 intensive care beds allocated for paediatric and neo-natal care at Rainbow far exceed other paediatric-focused institutes housed in larger chains (Apollo Cradle with 92) or smaller specialised hospitals (Surya with 282). This level of paediatric care helps differentiate its Obstetrics and Gynaecological services (in terms of being able to cater to complicated cases) as well, from other mother-child boutiques such as Cloud Nine, Motherhood and Mother’s Nest. Mature markets like the US and UK accommodate one paediatric-focused hospital for every 20 adult hospitals, which Rainbow is replicating here with its more than two decades of profitable operations.

Securing specialist workforce in a niche is a challenge which Rainbow must face. The company uses high retainerships, equity participation, rewarding career progression as a lever to secure good talent. One promoter has scaled the ranks from being an employee. The pre-IPO shareholding includes 16 per cent from employees (9 per cent of the said promoter-employee and 7 per cent from others).

Hub and spoke model

Rainbow operates via its hubs located at Hyderabad and Bengaluru, which serve dedicated patients and referrals from spokes (four in Hyderabad and two in Bangalore). The hub of each region provides comprehensive outpatient and inpatient care with capability extending up to tertiary and quarternary care (advanced medical care). The spokes provide up to secondary care in paediatric, obstetrics and gynaecology, and emergency services and referrals for the main hub.

Rainbow is planning to add spokes in Bengaluru, Chennai (one each) and two more in NCR region with IPO proceeds in the next three years. This should leverage the existing hubs in each of those cities, replicating the model, first perfected in Hyderabad and later implemented in Bengaluru as well. In this model, investors face lower risk of execution as spokes are being added to hubs which are already in place and commercialised.

Margin levers

Covid-impacted occupancy rates, at 56 per cent in FY20, declined to 34 per cent in FY21 and recovered to 46 per cent in 9MFY22. Out-patient volumes declined by 30 per cent in the period and are yet to return to normalcy. But ARPOB (average revenue per operating bed) and EBITDA margin improved from ₹30,000 and 27 per cent in FY20 to ₹46,000 and 34 per cent in 9MFY22.

Improved product mix primarily helped the metrics. Covid vaccination and cost control did its bit too. Lower OPD volumes elevated the product mix towards lucrative segments of Obstetrics, tertiary, and quarternary services. The traction from better product mix can sustain, but margin and ARPOBs can correct as soon as OPD volumes are restored. But better pricing growth (already implemented) and better utilisation can provide a cushion. The company added 23 per cent of its capacity right before the two-year Covid lull and the maturing facilities can bring better operating leverage. The largely-normalised quarter of Q3FY22 (with minimal one-offs) had an ARPOB of ₹42,000 and EBITDA margin of 34 per cent.

Company financials

Rainbow has negligible debt equity ratio of 0.06 times as on December 31, 2021, and will be debt-free post repayment of NCDs from IPO proceeds. The company reported 10 per cent CAGR in revenues in FY19-21 to ₹650 crore in FY21, which included a 10 per cent y-o-y decline on account of Covid. The recovery in FY22 has been strong with 9MFY22 revenues at ₹761 crores. Cost control aided profits to touch 9MFY22 to ₹126 crore from ₹44 crore in FY19. Addition of 300 new beds in the next three-four years and better utilisation of the 220 beds added in the last three years should sustain strong revenue growth. Qualitatively, the maturing profile of established hubs should also draw better obstetrics and paediatric in-patient volumes, which can be another lever for growth.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.