Globally it has been a brutal year for technology sector investors. The bellwether index for global technology stocks — Nasdaq Composite — is down 33 per cent ytd. Closer home, the Nifty IT index is down 27 per cent ytd, significantly underperforming the broader Nifty 50, which is flat ytd.

While the correction in the Nifty IT index, which is dominated by the large-cap IT services stocks, has resulted in froth in valuation settling down to some extent, many of the stocks are still trading expensive relative to their historical levels and global peers. With IT services being a largely global business, there may be no merit in the ‘India growth premium’ versus global counterparts. Hence, investors keen to increase exposure to the sector can consider accumulating on dips the stock of Accenture — the NYSE-listed global leader in IT consulting and services.

After correcting by 34 per cent ytd, Accenture is now trading at a one-year forward PE (Bloomberg consensus) of 23 times. This is at a more than 10 per cent discount to its five-year average of 25.9 times, and also cheaper than TCS trading at 25.5 times and Infosys trading at 24 times. Besides valuation, Accenture may also be a relatively safer bet than its Indian peers given the fact that it has outperformed its large-cap Indian peers in revenue and earnings growth in recent years. Its higher exposure to consulting and high-end services also works to its advantage.

Investors, however, need to be mindful of the increasing probability of recession in western economies next year, which will negatively impact businesses and stocks. Hence investments can be spread out over the next six months.

Business

As a global leader in professional services, Accenture has a diversified business with exposure to strategy and consulting (24 per cent of revenues), technology services (62 per cent) and business process outsourcing (14 per cent). Its strategy and consulting business differentiates it versus Indian IT services players. In this segment, Accenture works with C-suite executives and boards of the world’s leading organisations, partnering with them in helping them formulate strategies and accelerating enterprise reinvention to drive growth and value.

Accenture’s focus on higher-end services can also be gauged by revenue per employee metric. For FY22, the revenue per employee (average) for Accenture was around $92,000. In comparison, the same for TCS was at $47,568. This difference is due to some of the differentiated focus of the two companies and versus Indian IT services in general. Thus, for Indian investors, Accenture also offers a good diversification within the IT services/consulting space.

In terms of size and scale also it leads peers by a big margin. In recently concluded FY22 (August ending), it generated 2.5 times TCS’ revenue. It has a long track record of successful execution and strong customer relationships that has enabled it to maintain and build on its industry leadership. For example, it has partnered with 99 out of its top 100 clients for more than 10 years.

In terms of geographic exposure, its business is well-diversified with 47 per cent of revenues from North America, 33 per cent from Europe and balance from the rest of the world.

Financials and recent performance

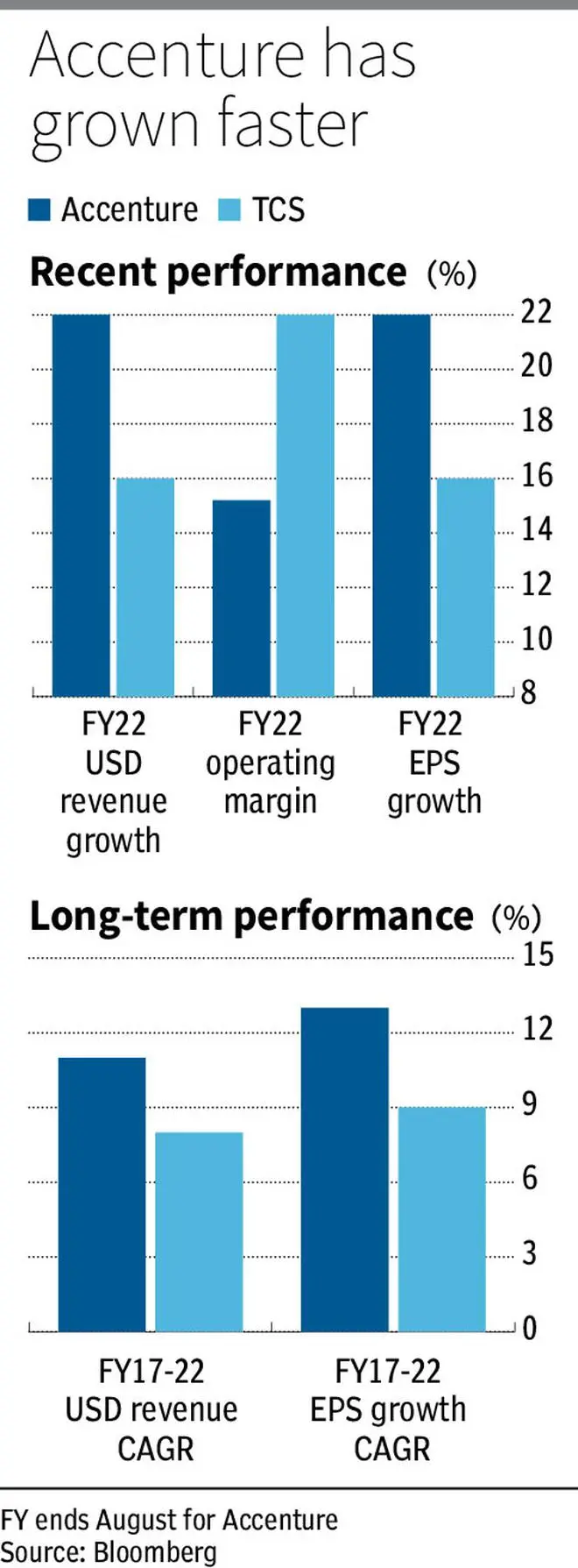

Accenture has been a beneficiary of the increased focus on business and digital transformations since the onset of Covid-19 and has capitalised on it well. During FY20-22, the company delivered a solid revenue and EPS CAGR of 18 and 20 per cent respectively. This is better than the FY20-22 USD revenue and EPS CAGR of 8 and 7 per cent respectively delivered by TCS. Even though the fiscal year-ends are different (August for Accenture, and March for TCS), the difference in growth appears significant. Accenture is of a strong view that they are market share gainers in the industry, something that they have been re-iterating in their quarterly releases, and their better growth appears to validate the same.

In its recently concluded FY22, Accenture reported revenue of $62 billion and EPS of $10.71; Y-o-Y growth of 22 per cent in both. Where Accenture lags Indian peers like TCS and Infosys is in its operating margins. For FY22, Accenture’s operating margin was at 15.2 per cent versus TCS’s 25 per cent. The lower margin is a price to pay for focus on growth and higher-end business opportunities that come with higher employee costs and more onshore presence. However, on the positive side, this focus has also enabled the company to defend its margins. In the recently concluded August Q results, Accenture’s operating margin was at 14.7 per cent and saw marginal increase Y-o-Y versus more severe contraction in operating margins witnessed by Indian IT peers.

The company also has consistent and robust capital returns policy. In FY22, it returned $6.6 billion (4 per cent of market cap) to shareholders via dividends and buybacks. This it has done after allocating some cash for growth initiatives as acquisitions have been integral to its strategy. The company’s FY23 free cash flow yield (FCF/market cap) based on consensus estimates is at 5 per cent and higher than that of Indian peers. This makes it better positioned to outperform in terms of capital returns to investors.

The company has guided for FY23 revenue growth of 8-11 per cent (in local currency, Accenture is headquartered in Ireland). Given the dollar strength, the growth in USD will be lower. Factoring the negative impact of a stronger dollar (which it estimates to be 6 per cent), the company has guided for EPS growth of 4-7 per cent. It expects to return at least $7.1 billion to shareholders during the year (4 per cent of current market cap). While stronger dollar is negative for Accenture results, Indian investors will see offsets as they will benefit from the same.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.