With markets being volatile due to macro economic as well as geo-political factors and likely to remain so for a while going ahead, cautious stock picking is the way to protect/build portfolio. Usually during such uncertain volatile periods, value stocks tend to outperform. Companies with attractive, stable and sustainable dividend yields come in this category.

One such stock is Indus Towers. Trading at one year forward PE of 11.3 times (Bloomberg estimates) versus 5 year average 17.2 times) and EV/EBITDA of 6 times (5 year average at 7.2), its valuation is reasonable based on a relative as well as absolute basis. Company’s dividend yield (based on current share price) for FY21 was 8 per cent, and analysts expect it to be between 6-7 per cent for FY22. Company’s payout ratios have been at 111%, 82%, 43% and 117% respectively from FY18 to FY21. Except for the blip in FY20, the payout ratio has remained high. Dividends are usually linked to annual free cash flows (FCF) and company’s estimated FCF yield (FCF/marketcap %) of 9 per cent for FY22 and 11 per cent for FY23, indicates dividends are likely to increase and remain attractive going forward. This will offer decent downside protection for the stock, with scope for appreciation as industry fundamentals improve driven by 5G investments and potential revival of Vodafone Idea.

Long term investors can look to accumulate the stock on dips as broader market volatility will offer attractive entry points in the stock.

Business and prospects

Indus Towers in its present form was formed by the merger of Bharti Infratel and erstwhile Indus Towers (which was a tower joint venture between Bharti Airtel, Vodafone and Idea) in 2020. Following the merger, Indus Towers is the largest tower infrastructure provider in the country and one of the largest globally.

Its primary business is to acquire, build, own, operate and maintain tower and related infrastructure. Tower infrastructure refers to equipment such as towers, shelters, power regulation equipment, battery banks, diesel generator sets etc required at sites where towers are installed. This type of facility is also know as passive infrastructure in the telecom context. These facilities are utilized by wireless telecom service providers on a shared basis, under long term contracts. Leasing external tower infrastructure frees valuable capital for telecom service providers to invest in their core operations and improving service quality. All wireless telecom service providers in India are customers of Indus Towers.

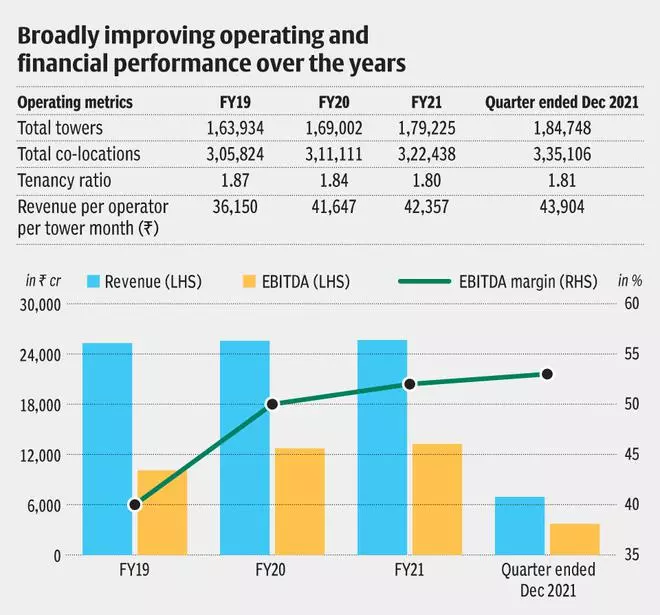

With 1,84,748 towers and 3,35,106 co-locations (more than one entity utilizing same tower), Indus Towers has nationwide presence with operations in all 22 telecom circles.

Prospects for the company depend on a combination of increasing demand for towers as telecom density increases as well as increasing utilization of/co-locations in towers as newer and enhanced offerings like 5G drive demand. Given this, two recent developments support improving business prospects for the company.

The first supporting factor is the increasing probability of revival of Vodafone Idea. With the government converting its AGR dues into equity in Vodafone Idea, the uncertainty that was stalling fund raising prospects for the company has been lifted. Markets still reflect possibility of duopoly in the wireless telecom services market and this is reflected in the valuation of Indus Towers as well. Further clarity on prospects for Vodafone Idea could be a positive catalyst for Indus Towers as it will drive demand which so far has been tepid from the key third player due to its financial issues. In the current scheme of things a Vodafone Idea that survives would be a good enough positive for Indus Towers, even assuming it is a weaker third player in a market dominated by Jio and Airtel.

The second positive factor is the dawn of 5G services in India with the recent Union Budget paving way for 5G spectrum auctions and roll out of services in FY23. While 5G services in India will require time to scale up, nevertheless given its mass adoption is matter of when and not if, the long term prospects for tower business is positive on this front. 5G will drive exponential growth in data utilization, increasing the need for densification of networks that in turn will increase tenancy ratios (co-locations/towers). This in turn will boost revenue and more importantly profitability as tower companies get more bang for the buck with the same tower. Trend in tenancy ratio would be a key metric to track going forward.

With Indus Towers trading at a one year forward PE valuation of 11.3 times, the risk reward is favourable given the potential for the above mentioned positives to play out. Besides with low tariffs in India, the need for service providers to save on capital by utilizing third party passive infrastructure is stronger. The company has no pure play listed comparables in India. Tower companies listed in the US markets – American Tower Corporation, Crown Castle International Corporation and SBAC Communications Corporation (all of them REITs) trade at one year forward PE of 42.1, 41.8 and 71 times respectively

Recent performance

In the recently concluded December quarter, Indus Towers reported revenue of ₹6,927.4 crore, EBITDA of ₹3,704.1 crore, and net profit of ₹1,570.8 crore. This was growth of around 3, 3, and 15 per cent respectively over December quarter 2020. There was one concern in results regarding increase in receivables to around 97 days versus around 75 days at end of Q2 (which in itself was higher than expected). This is primarily driven by delays in payments from Vodafone Idea. However with some of Vodafone Idea’s financial issues getting sorted out recently, it is reasonable to expect good progress on this front going ahead.

For FY23, analyst expectations are for the company to show largely flattish to mid-single digit percentage growth in revenue and EBITDA. While in general growth for tower companies is low, stability in earnings/ cash flows and dividend yields are factors that drive investor interest for these stocks. Company’s balance sheet is strong with net debt/EBITDA at a low multiple of 1.35 times.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.