Torrent Pharma has executed domestic branded business well and is replicating the same in the Brazilian market. But the issue in the last two years has been the generic side of the business operating in the US and German markets with 24 per cent top line contribution. Efforts to scale up in these markets have been unsuccessful in the last two years. While triggers to alter the status quo on generics top line may not be immediately available, margin improvement plans laid out by the company hold promise. This led to the post-result run-up in share price of 10 per cent on Thursday.

Following two years of erosion in generics, further downside should be limited. Investors can accumulate shares at every correction from here on margin improvement and sustained growth in Brazilian and Indian markets is expected from Q1 FY23. Investors, however, need to note that US FDA inspection awaited by the company is a critical risk to the share price even if US business contribution to valuations is minimal currently.

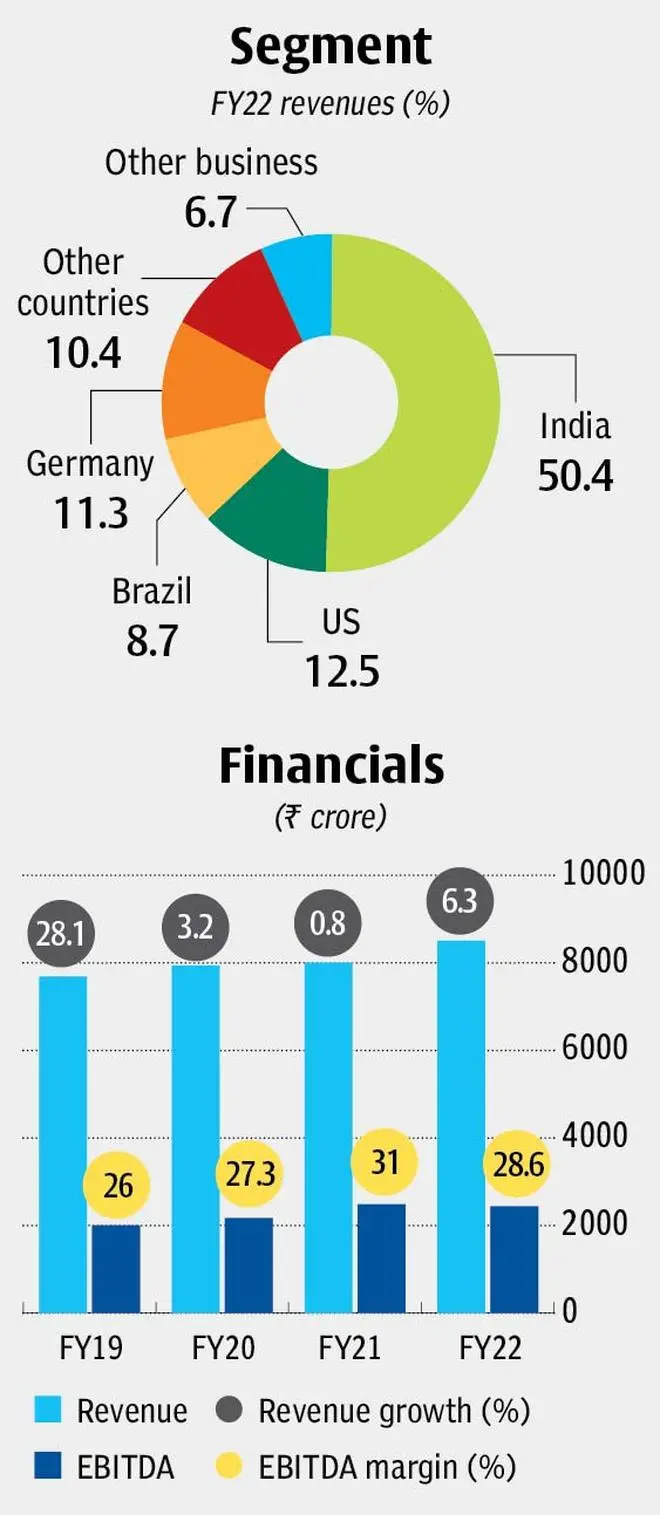

Segments and business

Torrent has a leading presence in Cardiovascular, CNS, Anti-Diabetes and Gastrointestinal markets in India (50 per cent revenue contribution in FY22). It has acquired and successfully integrated brands from Elder Pharma (₹2,000 crore in 2013-14), Unichem (₹3,600 crore in 2017-18) and more recently from Dr. Reddy’s (four brands). In Brazil as well (9 per cent of revenue), Torrent has a leading presence in branded generics markets for its mostly chronic portfolio. Similar branded generics portfolio is built in the Philippines and other developing markets as well which now account for another 10 per cent. This makes Torrent a 70 per cent branded generics manufacturer with a largely chronic portfolio, which bodes well from a pricing perspective. On the generics side, while price erosion is common across companies, Torrent reports high double-digit erosion in the US as lack of new launches is constraining the growth. Plant inspection and clearance by US FDA for Indrad and Dahej are crucial for new launches.

Revenue outlook

Branded: Torrent had optimised its product and personnel in India after Unichem acquisition and reported 15 per cent revenue growth in FY22 (following two years of mid-single digit growth) along with industry best sales force efficiency (close to ₹10 lakh per month per personnel). Now Torrent intends to drive new product launches in India supported by 13 per cent addition to the sales force to be completed by H1FY23 to increase geographic coverage and a larger basket. Four brands acquired from Dr. Redddy’s may add another 1-2 per cent growth in FY23 supporting a 13-15 per cent growth in India for next two years at least.

Brazil similarly added 5 products in CNS division in Q4FY22 accounting for more than half of the 32 per cent YoY growth in Q4FY22 and should ramp further in the next three quarters as well. In the long term, Torrent can track the mid-single digit broader market growth in Brazil; supplemented by cross-selling its portfolio from India, Torrent should drive above market growth in Brazil.

Generics: US generics business has accumulated 50-55 ANDAs (Abbreviated New Drug Application) of which 27 products are reportedly waiting for plant clearance alone. Torrent has also launched new derma product (Dapsone) with limited competition in Q4FY22. But lacking rapid launch capability till plants are cleared by US FDA, a high erosion in existing base can result in only a flat to negative growth for the segment even with the recent new launch. The high value Revlimid launch is not tied to plant clearance and can be a sizeable opportunity even in late-stage launch (which may be the case), and the only silver lining currently in US generics business. Similarly German tender market is also facing high competition suppressing pricing ability of Torrent which may be the case in the new tender cycle beginning in H2FY23 as well, leading to expectation of a flat sales growth.

Margin outlook

Torrent’s low revenue growth in reorganisation phase (4 per cent CAGR in FY20-22) may not be fully compensated by the 12 per cent expected CAGR in FY22-24 (combined 8 per cent CAGR in FY20-24). Despite a branded segments growth, US and German markets are holding back revenues.

Torrent has now announced a mix of measures to improve margins to supplement top line growth. It has closed its US liquid facility after a cost benefit analysis. Post impairment expenses in Q4FY22, operating costs of ₹135 crore per annum can be saved as per management, adding to the EBITDA margin line (by about 100-120 bps). Torrent is also in process of optimising production and reducing costs which should add another 80-100 bps to the margin even as freight, raw materials and energy costs remain high. Price increases in branded markets will be another addition. Torrent is expected to scale back up to 29-30 per cent EBITDA margin with these measures after slipping in H2FY22 to 26 per cent. Restarting US launches will add to margin growth instead of the downward pressure of the last two years, but that is dependent on plant clearance.

Financials and valuation

Torrent reported a 6.3 per cent YoY growth in FY22 revenues to ₹8,500 crore with EBITDA margins declining 240 bps to 28.6 per cent primarily driven US erosion and operating costs (RM and freight). Net debt to EBITDA stands at 1.3x (₹3,400 crore net debt) which the company hopes to clear in the next two years at which point Torrent’s acquisition play focussed on Indian market may resume.

Torrent trades at 26 times FY24 earnings and the premium is attributable to the branded presence of the company (23 times adjusted for amortization of acquired assets). This is in line with its last 5-year average valuation and a 15 per cent discount to last 6 months’ valuation range. Investors can ascertain the US FDA plant status and margin growth pattern in the short term and accumulate the shares of Torrent at every available dip in valuation.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.