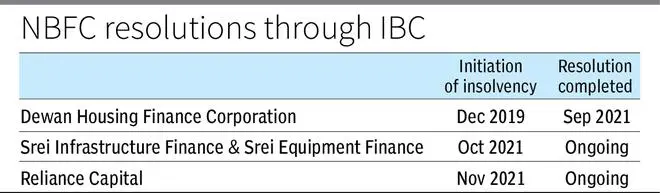

Since 2019 three notable non banking financial companies (NBFCs) have gone down the insolvency route. It started with Dewan Housing Finance Corporation when the Reserve Bank of India through an amendment to law included financial services providers (FSPs) in the IBC way of resolving stress. FSPs were not part of the initial list.

But today with resolution attempts at Reliance Capital and Srei group of companies stretching like slime, unsure of the final outcome, it’s pertinent to ask whether the inclusion of FSPs in IBC has yielded the desired results.

There are doubts around its efficacy given that the resolution process is complicated owing to the varied nature of the business, the underlying assets, and its customer facing business models.

One of the main differences is the absence of tangible assets such as land, factories, machinery and fixed assets in the case of manufacturing and allied sectors. Add to the fact that deterioration in financial assets due to business stagnation is faster compared with those businesses built on fixed assets because unlike the latter, for FSPs leverage and cash is what keeps them going.

Once that is cut off, which is bound to happen when the IBC proceedings are initiated, it makes the value realisation mechanism challenging.

As such, most resolutions under IBC take more than the 270-day timeline and the average realisable value is sub-35 per cent.

“For financial assets, it is difficult to ascertain a particular value because unless you resolve faster, it deteriorates much faster than other entities,” said Soumyajit Niyogi, Director, India Ratings.

Business and subsidiaries also suffer because these companies fall behind on strategic decisions that need to be taken at the holding company’s board and/or shareholders’ positions.

Uday Kotak, MD & CEO, Kotak Mahindra Bank who chaired the beleaguered IL&FS for over three years has a similar view. “NCLT process is tardy whether IBC or otherwise. In IL&FS too while recovery ratio is better, legal process takes long. Time for policy relook at financial sector resolution,” he said.

On an average, loans to NBFCs account for 11 – 13 per cent of total loans lent by banks. The domino effect that failure of FSPs could have on banks cannot be ignored and unlike brick and mortar companies going bust, the contagion impact on peers and the larger subsects due to failure of FSBs may be higher. It also increases the risk aversion towards the sector as public money is involved.

At the bidders’ end, resolution of FSPs demands the additional task of recoveries, collections and customer commitments. Depending on the nature of business and product mix, bidders may have to look at various options such as securitisation, one-time settlements and sale to asset reconstruction companies (ARCs) for resolution and integration, all of which point at an elongated and tiresome battle which bidders may want to avoid. Despite this, what if the asset is no longer as lucrative or entails a stiff haircut for lenders.

“Resolution becomes a long process because the prospective bidders also have to recover these loans, and then only can they pay the stakeholders and loan recovery may take a few years,” said Sudhir Chandi, Director, Resurgent India.

There is also the additional element of regulatory supervision in resolution of FSPs, which could add to the delays.

To be fair, a regulator-driven model for FSPs helps bypass frivolous applications while allowing informed regulatory decisions with respect to public money and securitised assets held by the entity.

However, additional compliances, regulatory clearances, requirement of a ‘no objection certificate’ and the appointment of a regulator-backed administrator may add to delays and possible tussles on resolution value and process, unlike in most other cases where the committee of creditors (CoC) has the only say. It is also possible that regulator-appointed administrator may not have the expertise or bandwidth to manage large corporates, especially when there are multiple subsidiaries involved.

RCap is a one-stop example which demonstrates what all can go wrong in the IBC-led process.

Consequently, with procedures taking priority, urgency in resolution takes the backseat leading to diminishing liquidation value.

For instance, in the guise of value maximisation how many times can the CoC (and it already has) invite bids or hold challenge mechanisms. As the process evolves, this is turning to be a major contention in the RCap resolution case.

Would then ARCs be better handled to deal with and turnaround stressed FSPs?

“The ARC model is time tested and has been working as they help liquidate those assets faster. Given the choice, it is the more efficient or relatively better model,” Niyogi said, adding that because financial assets tend to be fragmented, the preference is to consolidate them before opting for resolution or liquidation.

It may definitely be a better option vis-à-vis liquidation which could take longer as for the administrator to navigate through SARFESI or other recovery modes and then distribute proceeds to creditors.

But one of the main advantages of IBC-led recovery is that in the challenge mechanism bidders commit a substantial portion of the bids as upfront cash, thereby solving the short-term liquidity logjam. Another advantage is that intentionally, IBC is not just focused on insolvency and recovery but it also aims to ensure that the company remains a going concern upon finding a new shelter.

Perhaps then, the process is still in early days and one will have to give it time and bandwidth to grow.

“Whenever there is a new amendment, it’s through these litigations and processes that it ultimately settles down and the law becomes clear,” said Mukund P Unny, Advocate on record at Supreme Court.

“In that sense it is good that a few litigations are ongoing, where the SC will finally clarify how it has to be done,” he said adding with the apex court’s judgement on RCap expected in 3-4 months, things will become clearer on the aspects of the resolution mechanism.

Meanwhile, some support such as tweaks to speed up the insolvency process and clarity on regulations to avoid fragmented, biased and unsatisfactory outcomes could help FSPs.

“There could be some enabling provisions in the RBI Act to streamline the process in terms onboarding new promoters and expediting the process because speed is key,” Chandi said.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.