For a better experience, Read this story in our App

TO ENJOY ADDITIONAL BENEFITS

Connect With Us

Get BusinessLine apps on

Banknotes | Photo Credit: Getty Images/iStockphoto

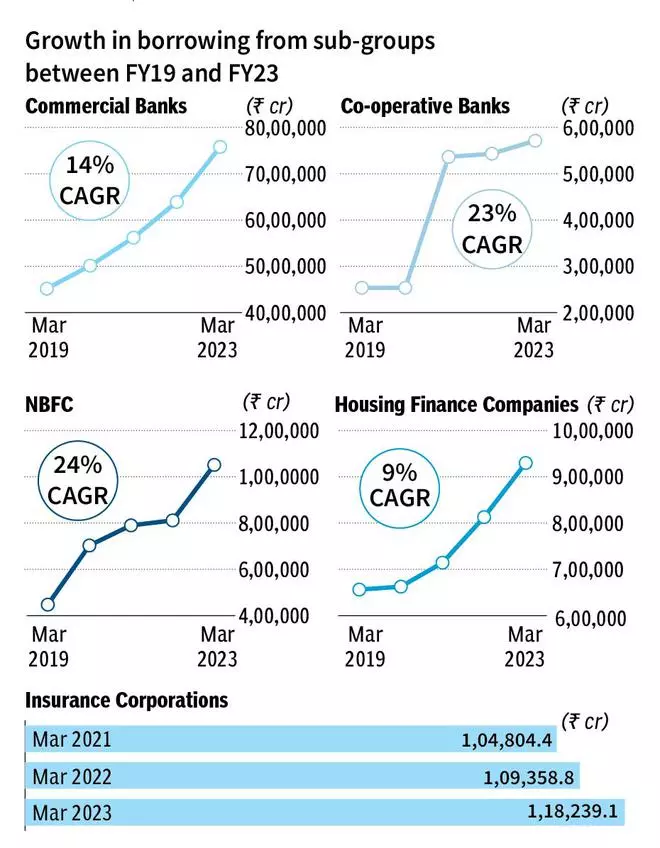

Indian households are fairly conservative and tend to limit their debt to the extent possible. But their borrowing has been increasing sharply of late. Household debt, as a percentage of GDP, was 28.5 per cent in FY18, but it has surged to 37.6 per cent by FY23. Of note is that borrowing from NBFCs and co-operative banks has recorded higher growth, compared to commercial banks or housing finance companies.

Data from RBI bulletin indicate almost doubling of overall household financial liabilities over six years, from ₹52.3-lakh crore in March 2018 to ₹102.5-lakh crore in March 2023. There has been a sharp surge of 18.3 per cent in FY23.

Madan Sabnavis, Chief Economist at Bank of Baroda, attributes the surge in household financial liabilities to increased demand and supply dynamics. He notes that “the financial sector’s heightened confidence in retail lending, coupled with a rise in post-Covid consumption and demand, has driven individuals to take loans for smaller-ticket purchases. This trend is contributing to elevated household financial debt by stimulating both demand and supply.”

Household borrowing from NBFCs has been growing strongly at a compound annual growth rate (CAGR) of 24 per cent between FY19 and FY23. The other segment which witnessed a sharp increase is loans from co-operative banks. It grew from ₹2.5-lakh crore in FY19 to ₹5.7-lakh crore in FY23 at a CAGR of 23 per cent.

Subha Sri Narayanan, Director, CRISIL Ratings Ltd, said: “In terms of segments, within retail, home loans and vehicle loans formed around 37 per cent and 21 per cent, respectively, for NBFCs as on March 2023, and have been growing at a good pace. Unsecured loans of both banks and NBFCs are also growing.”

“Borrowing from NBFCs is more accessible than traditional banks due to their widespread presence, better connectivity, and faster turnaround times. However, NBFCs, relying on both market and bank borrowings, tend to have higher interest rates compared to traditional banks,” says Sabnavis.

He adds that “liabilities in cooperative banks might appear higher, but it’s essential to consider that their overall volume is comparatively less”.

The fintech revolution and the army of new borrowers, with no credit scores, would also be contributing to the growth in NBFC loans.

Scheduled commercial banks, which account for over 75 per cent of household debt, recorded a far sedate growth of 14 per cent annually. Loans from housing finance companies too grew at a slower 9 per cent in this period.

The RBI thinks that the increase in household liability does not pose systemic risk. “The increase in financial liabilities was driven by a steep rise in borrowings from financial institutions, with a large part in physical assets creation (mortgages and vehicles). Thus, the overall savings of households may still hold steady with a compositional shift in favour of physical savings. This would directly add to gross capital formation, supporting an upturn in private investment cycle and, eventually, the prospects for growth,” states the RBI Financial Stability Report 2023.

Published on February 27, 2024

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.