cargo.jpg

In the early 1990s, Indian shipping lines carried one-third of the country’s cargo. Two decades later, their share has slumped to barely one-tenth, reflecting the poor growth of a sector that is pivotal for the country’s economic progress.

While the volume of cargo grew six-fold over the past 20 years, the domestic shipping fleet expanded at a snail’s pace, just by one-and-a-half times. As a result, 90 per cent of India’s sea-borne cargo is handled by overseas carriers, causing a huge drain on foreign exchange in the form of freight payment.

Indian exporters and importers shelled out an estimated $50 billion last fiscal to foreign shipping lines, and the outgo would be higher this year even as the Government burns midnight oil to rein in the current account deficit that hit a record 4.8 per cent of GDP last year.

A major part of this freight outgo is on account of oil imports. Out of the 172 million tonnes of crude imported last year, Indian tankers carried only 16 per cent – a steep fall from 66 per cent in 1994 when the oil cargo was reserved for Indian bottoms.

It is a pity that a country, which has a cherished tradition of shipping and seafaring and is endowed with more than 7,500 km of coastline, dotted with 13 major ports and over 180 non-major ports, depends on foreign lines to carry bulk of its strategic oil cargo.

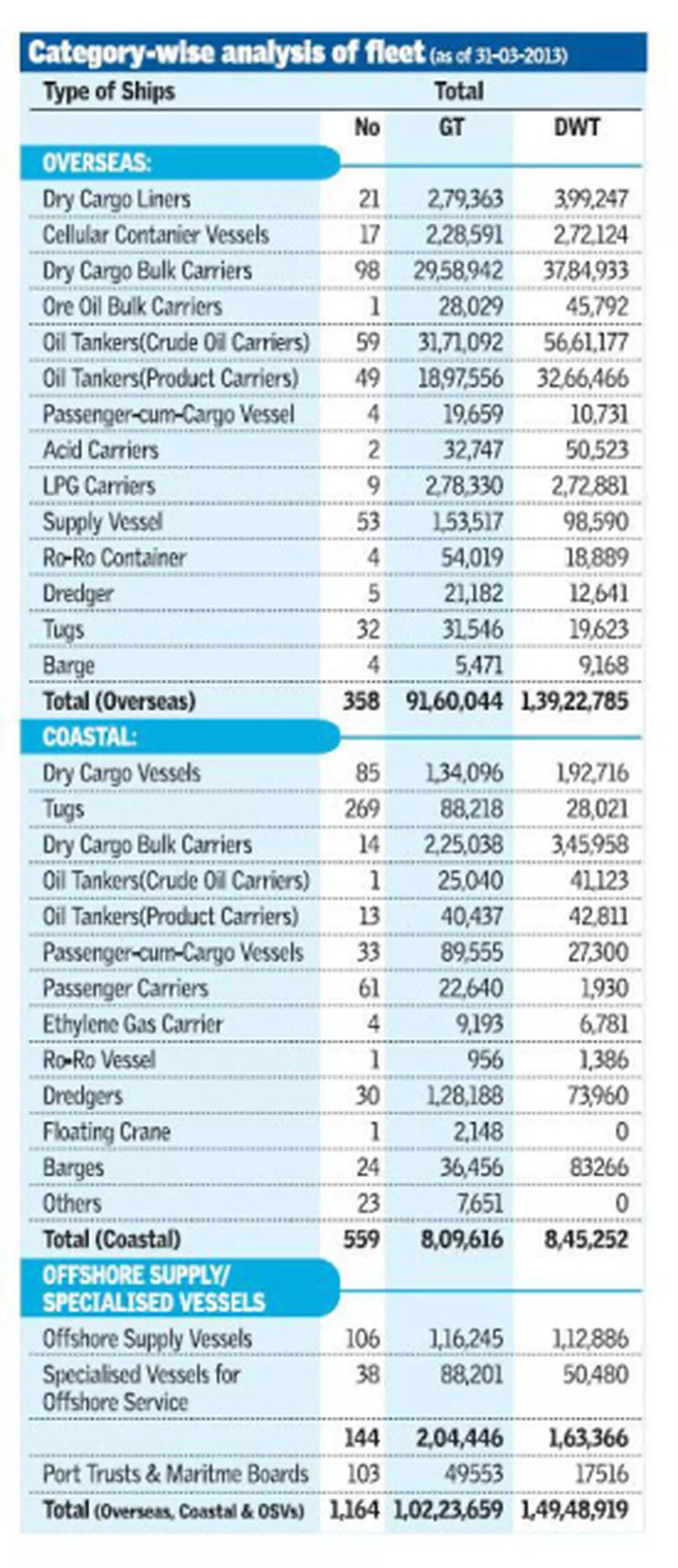

In the past two decades, the capacity of Indian merchant fleet expanded by four million gross tonnes (gt) — from 6.2 million gt in 1994 to 10.2 million gt as on March 2013. (Of the 1,164 vessels with an average age of 17 years, only 358 vessels of 9.16 million gt are engaged in international trade.) Its share in the global tonnage fell from 1.4 per cent to one per cent. It only shows that despite having a long-term assured cargo, India has not been able to keep up with the growth in world tonnage.

The Government’s shipping policy vows to increase the share of national carriers in handling the country’s cargo. That this is not happening should be a matter of national concern and a sad commentary on the officialdom in charge.

Cargo support

One thing that has remained unchanged is the shipowners’ demand for cargo support.

India followed a policy of import on free-on-board and export on cost-insurance-freight basis, to ensure that Indian ships carry the country’s cargo. However in the late 1980s, export cargo was exempted from this policy.

For import cargo, Indian lines continue to enjoy the first right of refusal. Transchart, the centralised agency in the Shipping Ministry, implements this for Government-owned cargo. However, over a period, the volume of Transchart cargo dwindled as many public sector undertakings opted out of the scheme.

Till 2002, oil cargo was reserved for Shipping Corporation of India on a cost-plus freight basis. This was discontinued following the dismantling of the administrative price mechanism for petroleum products. Oil companies are now free to make their own arrangements.

Indian ship owners are now seeking a 30 per cent reservation on all cargo though they do not have the capacity to carry half of it.

Funds crunch

A major grievance of shipowners has been that they are unable to raise funds for buying ships. Till the mid-1980s, they could get soft loans to buy ships through Shipping Development Fund Committee, which was later replaced by the Shipping Credit and Investment Company of India set up as a subsidiary of ICICI.

This dedicated financial institution for providing ship finance, was merged with its parent in 1997, but ICICI continues to provide ship finance.

Indian National Shipowners Association, the industry body, has been seeking a dedicated fund for tonnage acquisition.

FDI in shipping

As part of economic reforms, 100 per cent foreign direct investment was allowed in shipping and ports. Still, there has been hardly any FDI flow into shipping, though the situation in ports is different.

According to domestic shipowners, without cargo reservation, there is no advantage for a foreign investor to own an Indian flag carrier.

On the other hand, they are subject to several taxes and have to compete with foreign lines for the country’s own cargo. Foreign lines are free to come and pick up Indian cargo, shipowners argue.

Tonnage Tax

One of the best things that happened to Indian shipping was the introduction of tonnage tax in 2004 as a substitute for corporate tax. Under the tonnage tax scheme, the operating profit of a shipping company is determined on the basis of tonnage capacity of its ships. They have to keep aside a certain amount of profits for buying ships.

A large chunk of the global shipping fleet operates on tonnage tax, where the tax burden is just 1-2 per cent of their income, compared with the corporate tax rate 30 per cent or higher.

Initially, the tonnage tax helped domestic lines to expand their fleet. But subsequently, shipping lines were subject to several other taxes, including service tax, minimum alternative tax, sales tax, which nullified the benefits of tonnage tax. During the past two decades, global shipping witnessed its best and worst times. In the boom period of 2004-08, every shipowner made a fortune. The global economic slowdown hit the industry in 2008.

Prolonged recession

Since then, the industry has been facing one of the worst and the longest periods of recession in the last 50 years. New vessels ordered during the boom flooded the market and the excess tonnage brought the freight market to rock bottom level.

Indian industry was hit badly by the global downturn. Most firms have been reporting losses for several quarters.

Great Eastern Shipping was the only Indian line which could weather the storm. All others have been severely hit by the prolonged bad weather. Pratibha Shipping, a Mumbai-based tanker operator, collapsed with most of its nine vessels getting arrested by creditors. Varun Shipping, the country’s largest LPG fleet owner, has been facing cash crunch and not paid wages to employees for months.

The Government-controlled Shipping Corporation of India has been reporting losses for several quarters. The weak rupee added to its woes as it will have to pay more for its orders for new ships placed during the boom. Yet, SCI is the only company running liner services and LNG carriers.

Shipowners know that their business is subject to cyclical fortunes. Normally in good times, they save for the rainy day. This may not be the case with Indian industry as a whole. Many of them rejoice in the good times as if they would last forever. When the bad weather hits them, they are left floundering.

As a strategy, some companies flagged out and set up overseas subsidiaries. But they failed to acquire large tonnage and become global operators. They operated mainly for the benefit of the parent back in India.

Globally, shipping has been facing various challenges such as increasing incidents of piracy, technological changes, move towards green shipping, emergence of large container vessels and new laws on manning. Some of these could push up the operating cost of shipping companies, but eventually, that would be borne by the users.

Analysts feel that it may take at least another year for the global industry to come out of the choppy waters. The positive side is currently asset prices are 50 per cent lower than at the peak and it is the right time to acquire additional tonnage.

More than a third of the Indian fleet is over 20 years old and a large number of them require replacement. But shipowners are broke. Given the low level of domestic oil production, India will have to depend on imported crude for its energy needs in the foreseeable future.

The Government, oil and other PSUs, and the shipping lines should jointly work out a strategy to expand the domestic fleet. This will create a win-win situation for all stakeholders in the long run.

Published on September 27, 2013

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.