BL05_blggi_wholesale_col_NET.jpg

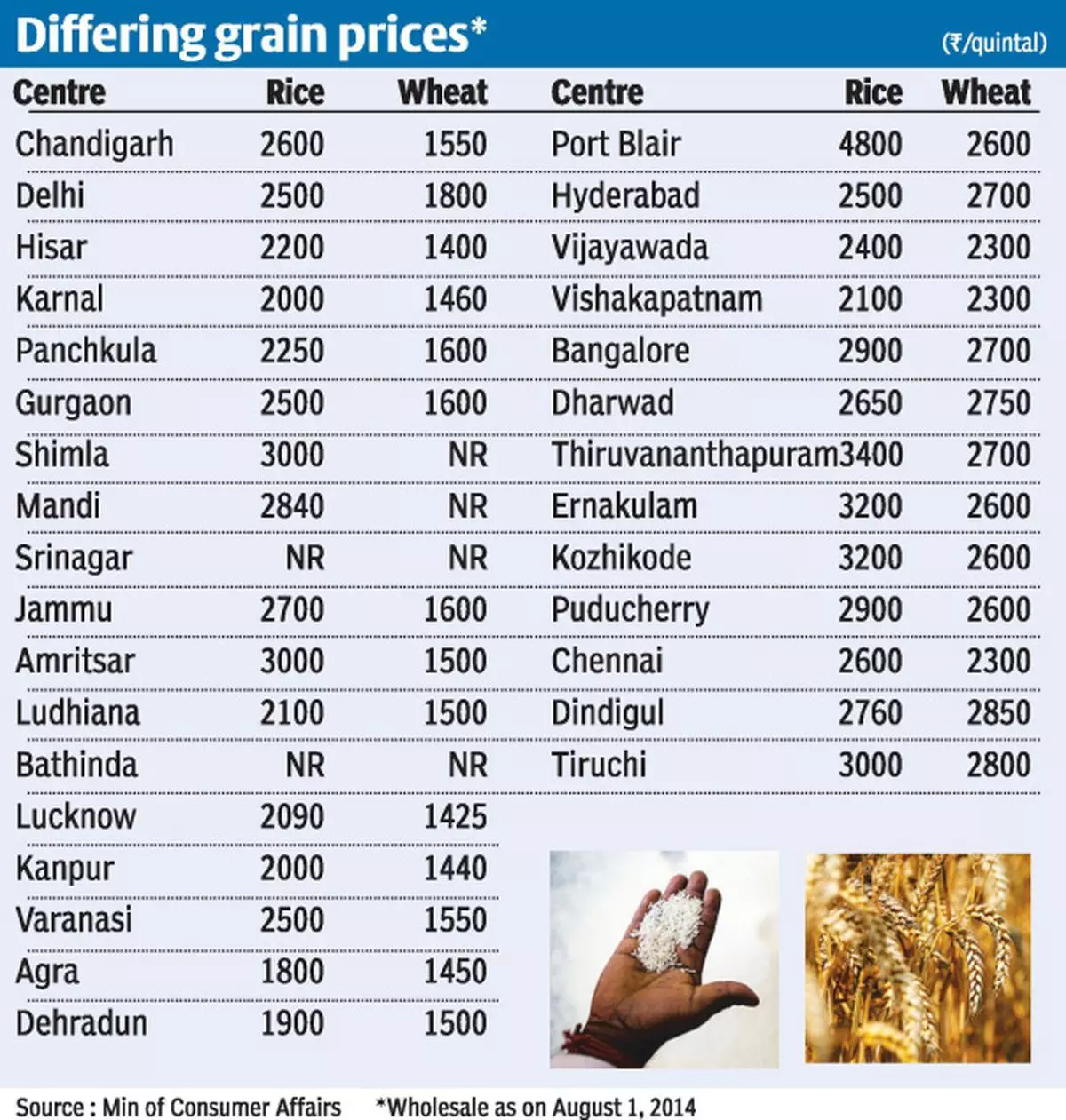

Wholesale prices of wheat on August 1, as seen in the Ministry of Consumer Affairs website, show a gnawing gap between values in North and South of the countrt.

In Punjab/Haryana cities wheat is quoted at ₹1,400/1,600 a quintal, while in Chennai/Hyderabad/ Bangalore it is between ₹2,300 and ₹2,750. Wheat in South is 70-90 per cent costlier than in North.

Is wheat indicative of a commercial divide within a country that distinguishes forces of supply/demand in the North and South? Apparent reason is that FCI/agencies wheat stocks in the North are 28.3 million tonnes (mt) vs 0.83 mt in South as of July 1, while the overall holdings with the FCI are 40 mt.

However, north-south difference in rice prices is within tolerable range 15-20 per cent. FCI/agencies stocks of rice in south zone are 6.5 mt against 10.6 mt in North zone.

Converting wheat prices in rupee into dollar, they are $383/460 in south India per tonne c.i.f – while Black Sea wheat can be accessed $265-270 and Australian APW at $310 on cif for 25-30,000 tonnes (mt) cargo.

Pakistan has already contracted about 7,00,000 mt at about $265-270 landed basis from Black Sea for August/September 2014.

Though the overall import tonnage may not exceed more than a one to two lakh tonnes by Indian importers/flour millers it shows that spread can be exploited if not compressed and values in South do not plunge.

World wheat market is bearish and may taper down further.

Flour miller may be willing get such cargos financed from multi-nationals such as Cargill, Louis Dreyfus, Concordia, Noble, Olam, etc on 6 months credit terms with nominal interest rates and guaranteed specified quality and delivery.

Regional offices of FCI have started notifying weekly tenders for disposal of 10 mt wheat under OMSS (open market sales scheme) formula with old crop at ₹15,000/mt and current crop at ₹15,700/mt price ex-Ludhiana plus rail freight, local depot handling charges, called “Reserve Price”, and local taxes.

A back of the envelope calculations show that e-auction landed price in southern States may be around ₹19,200/20,000 a tonne or about $317-330 for a flour miller with upfront payment and financing cost.

Supply is on “as is where basis is” and tenders do not specify adherence to any quality/specification and delivery period.

The case for importing wheat becomes more logical.

At least FCI should have one uniform comprehensive “tender document” region wise. To what extent such e-tender disposal will be effective will be revealed over the next 60 days.

But the Government could have exercised the option of calibrating “Reserve Price” ex-MP or ex-Bihar for freight calculations for south Indian States even though load depot could have been ex-Ludhiana.

The need to replenish wheat stocks with speed in warehouses of southern States also needs to be looked into.

Another implication under Food Security Act is that wheat/rice will be dispensed to PDS beneficiaries at ₹2 and ₹3 a kg – which lures illicit trade with a whopping premium of ₹25-30, due to which India’s multilateral negotiations at the World Trade Organisation has failed to make any head way because it distorts the market.

The odd feature is the multiplicity of prices for wheat on per quintal basis – MSP ₹1,400; economic cost ₹1,993; open market sale scheme ₹1,500-70; above poverty line ₹610; below poverty line ₹415 in addition those applicable under Food Security Act.

At macro –policy level, does not Indian Government need to consider “south-centric policy” for wheat?

It is worth pondering to bridge the divide.

Published on August 4, 2014

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.