For a better experience, Read this story in our App

TO ENJOY ADDITIONAL BENEFITS

Connect With Us

Get BusinessLine apps on

Combating pollution from industries is the challenge | Photo Credit: engabito

With the Energy Conservation (Amendment) Bill 2022 having been passed in the Lok Sabha on August 8, the much-awaited carbon trading market is expected to take shape.

While this is welcome, there is a caveat that it will be initially limited to ‘hard to abate sectors’ (HtAS). The term ‘hard to abate’(HtA) raises several questions on the scope and efficacy of the policy. Besides, the existing Perform, Achieve and Trade (PAT) scheme also purportedly incentivises carbon emission (CE) reduction leading to an obvious question — why have two policies with similar objectives? Why has the carbon market been restricted to HtAS?

The term HtAS pertains to a sector where the transition to net zero emission (NZE) status is difficult because of lack of technology and/or prohibitive cost. CE occur during the burning of carbonaceous fossil fired fuels, or in industrial manufacturing processes of cement, steel, chemicals etc. CE can be eliminated by substituting energy source/fuel- renewable solar/wind energy for thermal power; electric vehicles for petrol/diesel vehicles; and domestic electric appliances instead of kerosene/gas. However, industrial processes where the nature of chemical reaction is such that carbon dioxide is an inescapable output, such as in the production of cement clinker or iron in blast furnaces or chemicals and petrochemicals, CE can at best be reduced with better process efficiency.

For example, India’s cement industry is perhaps the most efficient in the world with the emission intensity reduced to 576 kg of CO2 per tonne of cement against the global average of 634 kg but has limited potential for further process efficiency and continues to be a HtAS.

Limitations of the PAT scheme: The underlying logic of the PAT scheme was to curb energy demand in 13 energy intensive areas — thermal power plants (TPP), cement, aluminium, iron and steel, pulp and paper, fertiliser, chlor-alkali, petroleum refineries, petrochemicals, distribution companies, railways, textile and commercial buildings — by improving their energy efficiencies.

By reducing energy consumption below a threshold limit that begets tradeable energy certificates (each certificate is for reduction of 1 MWH over a set target), an entity indirectly reduces CE and concurrently earns revenue. However, the PAT scheme does not incentivise efforts for the major direct CE reduction in HtAS emanating from industrial chemical processes. Over and above improvement of energy efficiency, HtAS would entail R&D-led alternative technologies/processes, or substitution of raw materials, the technical feasibility and commercial viability of which are yet to be established.

Hence, as such, there is no potential for additional benefit from the PAT scheme for most cement plants in India. Further, an integrated steel plant switching from the conventional blast furnace route to scrap based electric furnace steelmaking, may increase its electricity consumption but substantially reduce CE (by elimination of coke required for blast furnaces), would not qualify for energy certificate in the PAT scheme. The scope of the PAT scheme being limited, only 70 million tonnes CE reduction (2.5 per cent total CE) was possible at the end of PAT-II cycle in 2019-20.

Carbon Capture and Storage (CCS) is often portrayed as a pathbreaking solution for decarbonisation. However, CCS does not curb the CE in HtAS but merely captures the unavoidable CE and transports over long distances to store underground at depths of +2 km. It is an extremely expensive proposition (the operating cost placed by the International Energy Agency typically at $50/tonne) and calls for investment subsidy for most entities barring very large companies. If HtAS do invest on CCS the carbon trading market becomes an incentive.

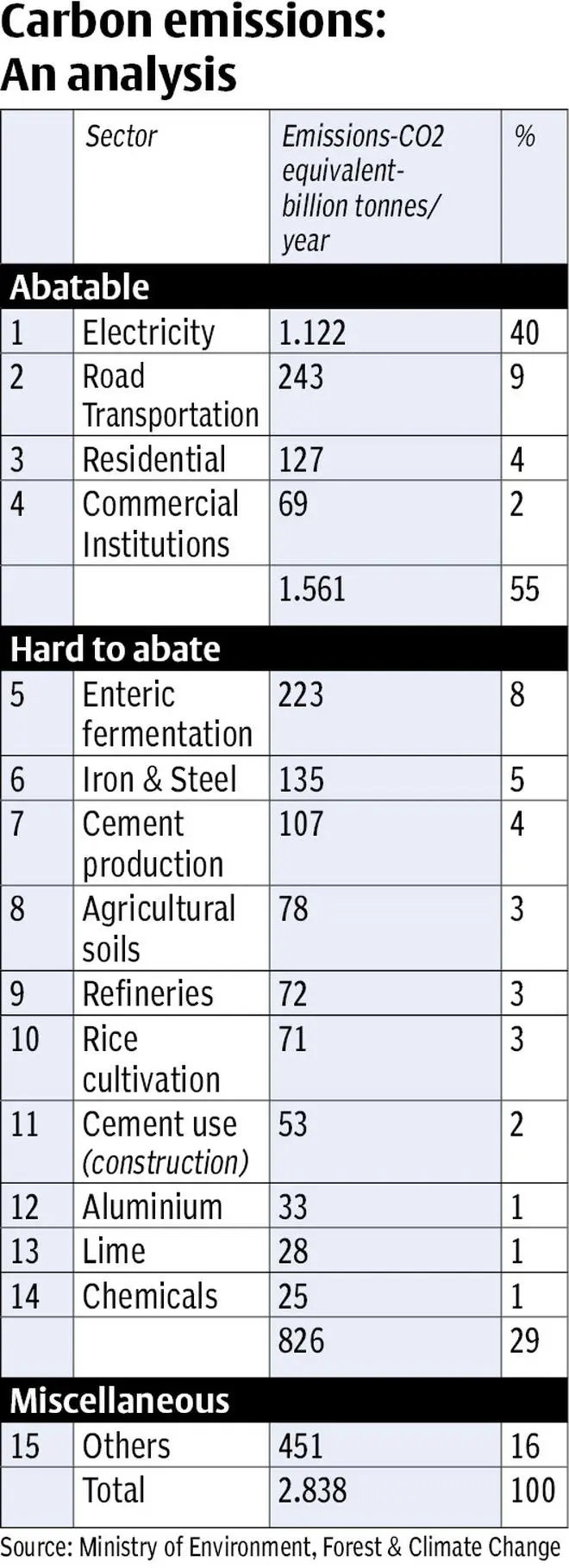

Volume of HtA emissions: India’s annual CE (expressed in terms of CO2 equivalent) is 2,838 billion tonnes accompanying Table, of which abatable CE is about 1,561 billion tonnes including: (a) 1,122 billion tonnes (40 per cent) through substitution of thermal power by renewable solar and wind energy; (b) 439 billion tonnes (15 per cent) by switching over to electric road vehicles; and electric appliances in residential and commercial establishments. The balance 1,277 billion (45 per cent) tonnes from process industries, animal husbandry and agriculture are ‘hard to abate’.

In the future, the CE of the energy sector will reduce substantially with gradual phase down/phase out of thermal power plants (by 2045). However, the needs of India’s rapidly growing economy will lead to quantum increase in demand for cement and steel-by 2050, the cement capacity is expected to increase from 330 million tonnes to 1,000 million tonnes and steel from 125 million tonnes to 440 million tonnes.

In this business-as-usual scenario, the aggregate CE are expected to increase to 6,033 billion tonnes and the HtA emissions could increase from 45 per cent to 76 per cent. This threatens to derail the achievement of NZE by 2070 and hence, the introduction of the carbon trading market for HtAS is a step in the right direction.

The carbon trading market revolves around the presence of: (a) permissible threshold limits of CE for each industry, (b) market players’ success at decarbonisation, reducing CE to below threshold levels, and/or attained lower net CE by investing in carbon sequestration or afforestation, (c) polluting/inefficient market players whose CE exceeds the permissible threshold levels, and (d) pricing mechanism that acts as an incentive for sale of credits by efficient market players and purchase of credits by inefficient market players.

In Europe, which has the largest carbon market operating for over 16 years, industry has been lukewarm, barring the power sector wherein carbon credits have helped expedite a switch from coal to gas-fired electricity. Steel companies offset their CE by buying cheap credits from China, East Europe and other emerging economies and continue to pollute the environment. It is generally accepted that carbon prices should be double of current levels to trigger a behavioural change and be attractive for renewable technologies like ‘green hydrogen’.

According to the Paris agreement, the UN Panel on Climate change has indicated a price range of $40-80 per tonne of carbon dioxide if global warming is to be pegged within 2 degrees by 2050. However, the prices till the last quarter of 2021 were way below, in the range of $2 to $12 per tonne CO2. In December 2021, the price crossed €50 per tonne and touched €56.35 ( $68/tonne) which is encouraging.

While many analysts believe that the carbon credit price would touch $80/tonne level only by 2030, some are predicting a price of €110 ($136/tonne) in the near future.

The idea of a carbon market presupposes that market dynamics will enable optimum price discovery that is a deterrent for polluters and incentive for entities who invest on protecting the environment. This objective does not appear to have been realised so far.

Although, these are early days, if the proposed carbon market in India does not become vibrant and robust quickly, there is a danger that HtAS will buy carbon credits at low prices and continue to increase their CE defeating the very purpose of a market linked mechanism that determines a deterrent cost for pollution. Hence, it is to be hoped that the carbon trading policy including the permissible threshold limits in each industry are carefully crafted to meet the twin objectives of growth and quality of life.

The writer is Advisor, Rajagiri Vidyapeeth and Miles School of Branding and Advertising, and a member of the ‘IIT Madras Alumni Association – Societal Impact Action Group’’

Published on August 29, 2022

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.