For a better experience, Read this story in our App

TO ENJOY ADDITIONAL BENEFITS

Connect With Us

Get BusinessLine apps on

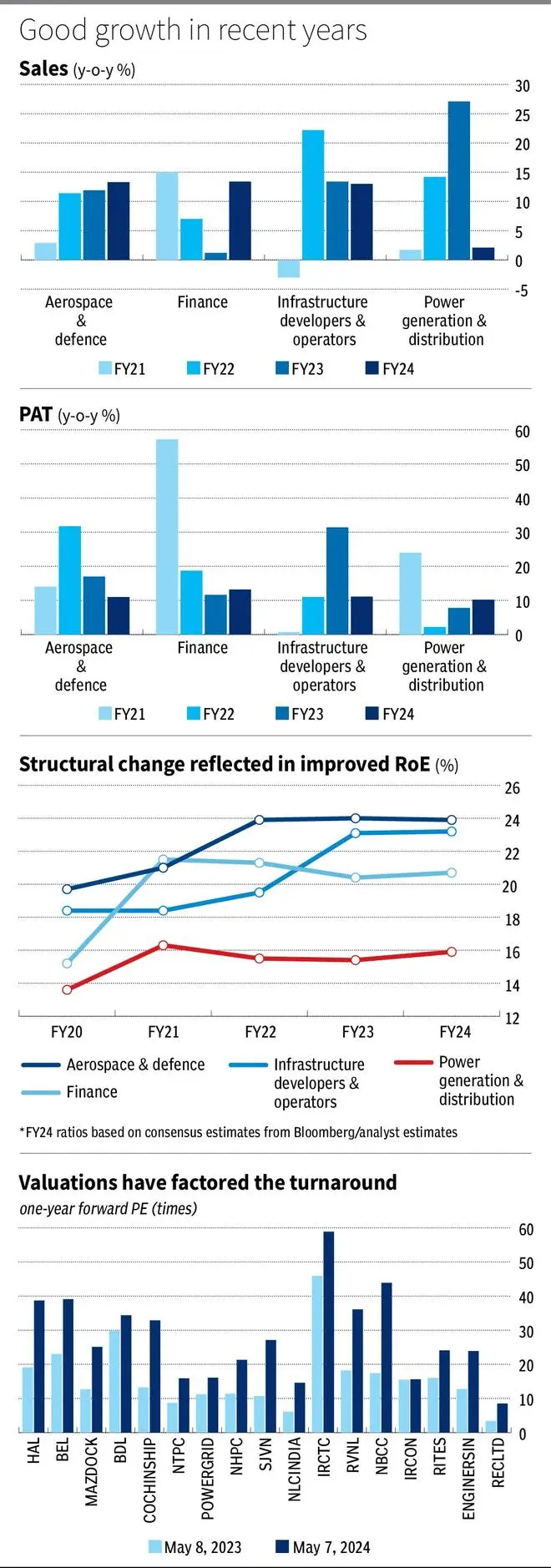

PSU stocks were amongst the best performers of FY24, rallying 88 per cent (BSE PSU) compared to Nifty-50’s 20 per cent returns. The reasons ascribed for the rally range from the last bastions of value to structural changes, which have changed the earnings trajectory for the good. Though much of the structural changes were planned much before FY23-24, the perceptible change in earnings growth, return metrics and improved leverage ratios have powered the rally in the last year.

We analyse the top four PSU segments based on stock returns in the last year and try to map them to the changes in policy, the current demand environment, and the financial strengths.

Under the aegis of Atmanirbhar Bharat (self-reliant India) and Make In India, there is an effort to encourage indigenous design, development and manufacture of defence equipment. Not only has the Defence procurement budget increased 20 per cent YoY in FY24 to ₹1.72 lakh crore, but also favourable policies have allowed domestic PSUs a higher share in the defence procurement pie.

In order of priority, availability, and due considerations, the procurement shall prefer indigenously designed and developed products with least preferance for globally developed products.

There is also a Positive Indigenisation Lists which embargos imports of 209 Services and 2,851 items. The government has also planned for two Defence Industrial Corridors, one each in Uttar Pradesh and Tamil Nadu, to improve the defence manufacturing ecosystem.

The PSUs that stand to gain the most from the changes are the ones with unique capabilities in the domestic space, including military aircraft (Hindustan Aeronautics), submarines and destroyers (Mazagon Dock), and Drone (Bharat Dynamics), and radars and sensors (Bharat Electronics).

The companies have an enviable order book as well. Hindustan Aeronautics has 3x order book (3 times trailing revenues), which includes 83 Light Combat Aircraft-Mk1A or Tejas Mark-1A in the medium term and developing Advanced Medium Combat Aircraft (AMCA) and helicopters in the longer term. BEL has 4x order book, which is diversified amongst Electronic Warfare, Communications, Weapon System, and Radars. Mazagon Dock delivered five submarines in 2017-22 and its order book is at 4.5 times. The company is also working on P76 class of submarines after P75 laying the ground for future order book.

A significant momentum in order inflow and delivery can be expected post-election. Cochin Shipyard, for instance, can expect further clarity on IAC 2 (air craft carrier), a repeat order of INS Vikrant, after elections, which is a ₹5,000 crore per year contract for 10 years.

The segment is expected to report 13 per cent growth in FY24 despite supply issues from Israel and Russia. The segment continues with a high RoE of 24-23 per cent owing to improved asset utilisation of 4.3 times for FY24 from 3.3 times in FY20.

The segment valuations have doubled over the past year, reflecting the structural changes. But the premium valuations are not factoring risk of project execution at the current stages. Investors may accumulate the stocks operating in high-end technologies, which are in a growth trajectory, but at reasonable valuations that factor for risks.

The central policy on power has set targets on overall capacity, renewable energy share and limiting losses and improving efficiency. India peak demand grew from 119 GW in 2009 to 221 GW in 2023-24 at a CAGR of 4.5 per cent. But the Power Ministry expects growth at 7 per cent CAGR growth for the next decade as peak demand is expected to grow to 366 GW by 2031-32 (Electric power survey).

The established capacity has to go up to 900 GW, from about 417 GW today, more than doubling its capacity, which is around 10 per cent CAGR growth. Currently, fossil-based power generation capacity accounts for 57 per cent, primarily driven by Coal (50 per cent). Renewable energy (RE) accounts for 41 per cent of the installed capacity, including solar power (16 per cent), Hydro (11 per cent), and wind (10.3 per cent).

The government has also mandated that 50 per cent of the cumulative electric power installed capacity should be from non-fossil fuel-based energy resources by 2030. This implies that the future power generation will be heavily tilted towards RE-based generation. Total installed thermal power capacity is expected to be 283 GW and non-fossil-fuel-based capacity to be 500 GW by 2031-32, according to Power ministry.

On the tariff side, there is policy continuity. Reimbursement is based on cost-plus model with a target of 15.5 per cent RoE for thermal projects and 17 per cent for hydro, which was recently revised upwards to incentivise production.

On the production side, NTPC accounts for 17 per cent of the total installed capacity with 73 GW in FY24, which it plans to increase to 120 GW by 2030-31, of which 60 GW will be from RE. This is a 7.3 CAGR growth visibility in capacity. NTPC will be commercialising 16 GW in the next 3-4 years and on the RE front, NTPC has 3.3 GW existing RE capacity, 7.8 GW under construction and 11.9 GW in pipeline.

NHPC accounts for 15 per cent share of installed Hydro capacity in the country. But owing to higher RE focus, the capacity addition for NHPC is at a faster pace. Compared to 7 GW of installed capacity, NHPC has 10 GW under construction and 7 GW under clearance stage. This should triple its capacity on commercialisation in the next 10 years with a capex outlay of ₹10,000 crore per year.

Power Grid, which has a 67 per cent market share in transmissions, is equally invested in expansion. The company is looking at ₹1.9 lakh crore capex outlay till 2032 of which a large part is interstate (₹1.2 lakh crore). The next three years capex outlay is at close to ₹50,000 crore, implying a strong head start.

The sector is expected to deliver revenue growth of 2 per cent in FY24, but that is on a high base of last two years when revenues expanded by 22 per cent per year. Despite this, the segment reported a 10 per cent PAT growth owing to lower leverage costs as Net debt to EBITDA reduced from 4.1 in FY20 to 3.7 times now and improved asset utilisation, which improved 31 per cent from FY20. The RoE of the sector, at 15.9 per cent, is inching up over the years. The three stocks are trading at an average 18 times forward earnings (1.7 times last year valuation), the sector is not at a premium to private players. The strong scope of expansion does not share the same risk of execution as defence companies but only timing risk.

Power Finance Corporation and Rural Electrification Corporation are two major financiers to power companies. The focus on higher share of RE power generation while sustaining thermal power implies a higher financing need. The large capex outlay to push the RE power implies a capex outlay of more than ₹2 lakh crore, of which a third or more must be supported by credit.

The financiers have strengthened lending norms, which is reflected in the NPA ratio contracting to around 1 per cent for both companies starting, from more than 3 per cent in FY20. All the while the companies have maintained a healthy yield (NIM) of more than 3.5 per cent.

The healthy metrics are in part driven by Late Payment Surcharge (LPS) and Revamped Distribution Sector Scheme (RDSS). RDSS, launched in July 2021, aims to improve credit standards at Discoms in evaluating their customers with the aid of smart meters. The LPS allows for concrete action on late payments from discoms. Along with timely subsidies and receipts from the state governments and the above regulations, the financial health of power supply chain has boosted growth and profitability metrics for financiers.

The segment has reported 13.4/13.2 per cent YoY revenue and PAT growth in FY24 and the RoE has improved to 21 per cent for the sector. With a valuation of 1.6-2.3 times price to book value, the stocks are not priced at a premium. The credit growth visibility, a strong control on credit costs and attractive yields at a lower valuation imply that Financier PSUs should interest investors.

Railways budgetary allocation and policy support have been on a high, although temporarily on hold in view of the elections. After a significant 48 per cent increase in FY23 (albeit on a lower base), the railway budget increased by 6 per cent in FY24 as well and is now at ₹2.6 lakh crore. Allocation to rolling stock and new lines has similarly kept pace.

While the earlier Dedicated Freight Corridor (DFC) is nearing financial completion (90 per cent as of December ‘23), several other projects totalling 3,500 km are under various stages of project planning as an extension of the DFC. The Centre will implement three major economic railway corridor programmes targeting energy, minerals and cement corridors the details of which should crystallise in the post-election Budget session.

The National Rail Plan is still on track to increase share of rail traffic in freight to 45 per cent by 2030, from the current 21 per cent, by improving average speed to 50 kmph from the current 37 kmph.

Further, on the passenger side, with the initial success from Vande Bharat, other bogies cannot be behind. Over the next five years, the Railways Ministry is planning to overhaul 40,000 train bogies to provide a better passenger experience similar to that of the Vande Bharat trains. The entire exercise is expected to cost ₹15,200 crore.

RVNL, RITES and IRCON have gained significantly owing to policy emphasis and investor excitement around government initiatives. RVNL order book is at 3x revenue and, more importantly, the order wins in 9MFY24 are a diversified mix of rail — 20 per cent, metros — 26 per cent, irrigation — 14 per cent and power —30 per cent. Vande Bharat and city metro projects will continue to drive revenues for RVNL as connecting seven more cities is under execution. International projects in Uzbekistan, Kyrgyzstan and UAE-Saudi Arabia (under a JV) will add geographic diversification as well.

IRCON is expecting to double revenues in the next fiveyears with mix of Rails/ Roads & Highways (HAM) projects in execution. Order book faced sluggish growth in FY24 and is expected to be at 2x FY24 revenues as geopolitical tensions and delay due to elections have impacted order book growth. But over longer term IRCON is looking at high speed train corridors which resonates with the National Rail Plan.

The segment financials show a similar improvement in return metrics. The valuations have similarly doubled for the sector with the exception of IRCON, which continues to trade at 16 times forward earnings . While the segment can be in focus post-election with a renewed budget and proposals getting clearance, the high valuations especially in the case of RVNL could hinder any further appreciation for now.

Published on May 11, 2024

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.