For a better experience, Read this story in our App

TO ENJOY ADDITIONAL BENEFITS

Connect With Us

Get BusinessLine apps on

Even as RBI’s rate hike cycle has been in place for a few months now, bank deposits don’t seem an attractive option yet for investors looking for the safest avenues. Barring a few small finance banks, most banks offer only sub-7 per cent returns on deposits across most tenures. Add to this the burden of interest being taxed at slab rates, the attractiveness for FDs dims even further, especially for those in the higher tax slabs. The case with post office small savings schemes is no different.

Target Maturity funds (TMFs), investing in Central and State government securities (g-secs and SDLs), fit in well here. With bond yields across tenures inching up in the last year, returns (yield to maturity or YTM for TMFs) are better than FDs/post office deposits for the same or lower risk profile. While like any other debt fund, NAV of TMFs is also subject to market fluctuations, holding the fund to maturity eliminates this interest rate risk and fetches the YTM disclosed at the entry point (post expenses). The bigger advantage is also the taxation. Being debt funds, TMFs with a holding period of over three years are treated as long-term capital assets and are taxed at 20 per cent with indexation benefit. Thus, post-tax returns are better for those in the higher tax slabs. While direct investing in g-secs and SDLs is possible through the retail direct platform, TMFs score once again on the taxation front and are more investor friendly (lower outlay, diversification of portfolio).

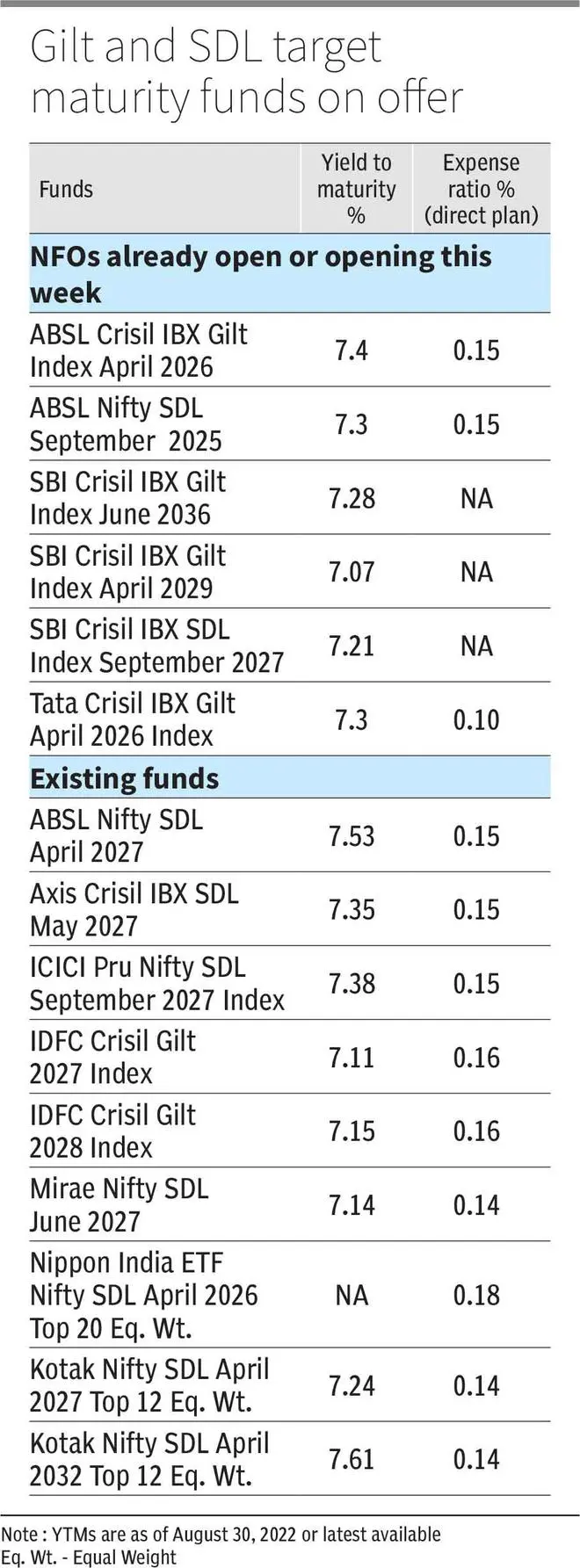

At least five TMF NFOs (new fund offers) are open currently and there are a host of other existing funds in the same category which have attractive YTMs as well. Here’s a lowdown:

NFOs of five gilt funds — those that invest in Central government securities, from the house of SBI MF, Aditya Birla Sun Life MF and Tata MF are open currently, with investment horizons ranging from 3-4 years (ABSL, Tata), 6-7 years (SBI) and about 14 years (SBI).

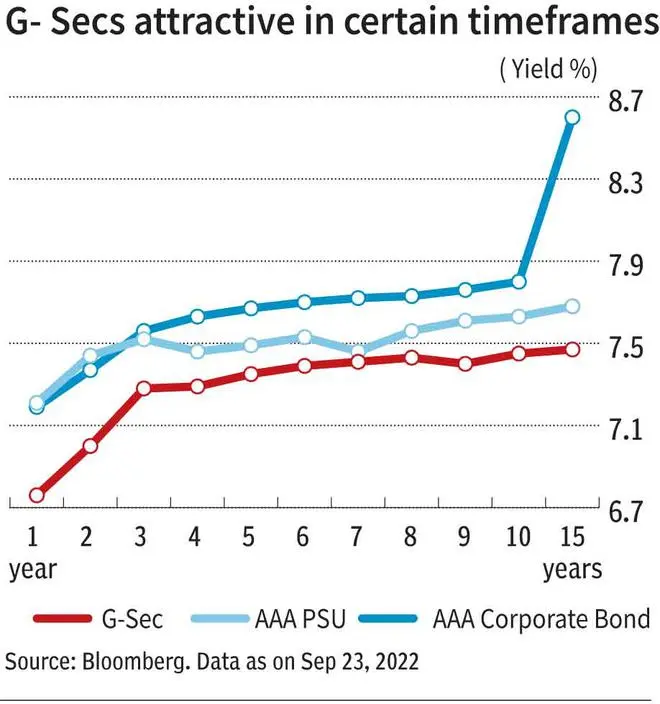

Yields on g-secs across the curve have moved up sharply in the last year. Today, yields on the benchmark 10-year G-Sec stands at 7.39 per cent, about 120 basis points higher than a year ago. Yields on the 4-year and 5-year G-Sec, for instance, are up by a sharper 172-204 basis points in the same period. Persistent inflation, the beginning of rate hikes after a pause due to Covid and global cues have helped in the upswing in bond yields so far. While it looks like the script may go in the same direction in the near to medium-term as well, how long the hikes will continue as well as the steepness cannot be predicted accurately. A 7 per cent plus YTM can be a decent return to lock into currently, in a fund that syncs with your time horizon.

The Tata and ABSL NFOs (April 2026 maturity) seem to be targeting the narrow spreads between g-Secs and the AAA PSU as well as AAA corporate bonds in the 3-4-year bonds. The SBI April 2029 NFO is cashing in on the spread of the 7-year AAA PSU bonds over g-secs being at just 0.05 basis points, providing almost no incentive to take additional risk.

Investors should note that there are also other existing TMFs in the same category — IDFC Crisil Gilt 2027 & 2028 index funds. If your time horizon matches with these funds, you can lock into these open-ended funds at their current YTMs as well.

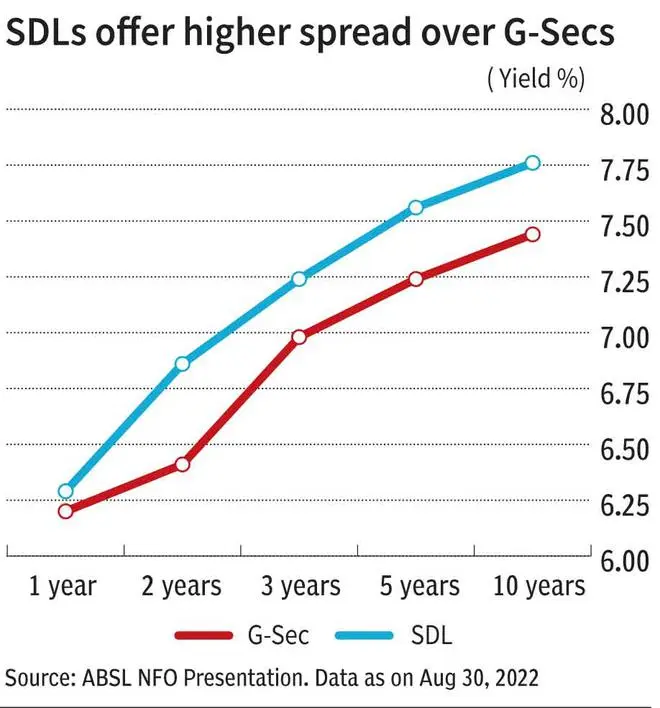

State government bonds too are sovereign instruments. Most existing SDL-based TMFs mature in 2027 and offer YTMs even as high as 7.5-7.6 per cent. In an earlier article in bl.portfolio on ‘Why you should buy SDL target maturity 2027 funds’ in the edition dated March 20, 2022,, we had indicated reasons for investing in SDL-based TMFs – higher spread over g-secs and improving liquidity being the key factors. The two SDL NFOs from SBI (September 2027) and ABSL (September 2025) offer YTMs of 7.2-7.3 per cent, going by the latest information available from the fund house. Other existing funds listed out in the accompanying table can also be good choices if they match your time horizon.

Final word, don’t invest all your surplus at one go now. Keep some powder dry and purses open for locking into TMFs if bonds yields rise further too.

Published on September 24, 2022

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.