For a better experience, Read this story in our App

TO ENJOY ADDITIONAL BENEFITS

Connect With Us

Get BusinessLine apps on

istock

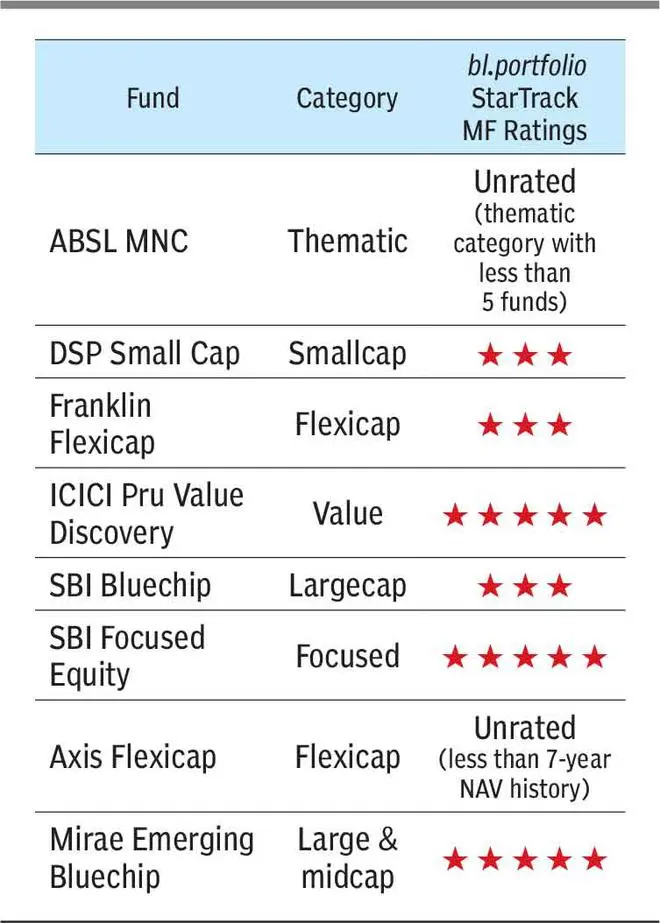

I have been investing through monthly SIPs in the below-mentioned funds (direct, growth) for over five years — Aditya Birla Sun Life MNC, DSP Small Cap, Franklin Flexi Cap, ICICI Pru Value Discovery, SBI Bluechip, SBI Focused Equity, Axis Flexicap (30 months) and Mirae Asset Emerging Bluechip (30 months).

To begin with, I started investing ₹5,000 per month in each of the funds, but have been topping up the instalments from time to time. Currently, the amounts of investment are increased to ₹7,500 per month.

I would like to continue my investments for another five years, with the aim of creating wealth.

However, on review, I found that the return from the ABSL MNC fund does not look as impressive, compared to its benchmark fund returns.

I seek your advice on whether to switch from this fund, especially after investing for over five years. If so, would it impact the benefit of compounding? And finally, what should the target fund be?

Balakrishna Rao K, Visakhapatnam

You have a fairly diversified portfolio in terms of exposure to different mutual fund categories. Most of your funds are rated 3 to 5 star by bl.portfolio Star Track Mutual Fund Ratings, and hence you can continue your investments in them.

Your time-frame of 10 years for wealth creation works reasonably well for equity funds. A 12 per cent CAGR in your portfolio is a realistic expectation to hold. If you have a goal to meet five years from today, you need to redirect the funds to safer avenues a year or so earlier, to preserve your gains. Otherwise, if your time horizon is a bit flexible, you can continue holding the investments for a longer period, if need be.

Step-up SIPs are a good way to buffer for lower-than-expected returns on your portfolio as well as inadequate estimation of corpus requirement at the time of starting the investment. To illustrate, a SIP of a constant ₹5,000 over 10 years, assuming a 12 per cent CAGR return, will lead to a corpus of ₹11.6 lakh. If the monthly SIP is stepped up by ₹500 a year, then the corpus grows to ₹15.7 lakh, assuming the same 12 per cent CAGR return. Even if the return comes down to a lower 10 per cent, the corpus with step-up SIP of ₹500 a year, will still be higher at ₹14.1 lakh vs ₹11.6 lakh without the step-up. You can continue to step up your SIPs as and when your investible surplus increases.

Coming to ABSL MNC, data from ACE MF shows that ABSL MNC’s one-year average daily rolling returns in the last five years (direct plan), at 10.5 per cent, is lower than all peers — ICICI Pru MNC (36.1 per cent) and SBI Magnum Global (16 per cent) and UTI MNC (12.4 per cent). It is also lower than Nifty MNC TRI’s 14.2 per cent return. In fact, the Nifty MNC TRI itself has underperformed the Nifty 50 TRI’s 16.6 per cent returns in this period.

This shows that thematic funds work well as part of our satellite portfolio for sub-goals and may not be suitable for long-term wealth building/compounding. Tactical entry with lump-sums in a few instalments when the theme is in vogue and exit when the winds turn out of favour is the approach to be adopted here.

You can stop fresh SIPs in ABSL MNC and distribute the amount being invested here among the 5-star funds in your portfolio.For the existing corpus in the MNC fund, it can be moved out to an aggressive hybrid fund such as ICICI Pru Equity & Debt and Canara Robeco Equity Hybrid in few instalments. Given that you have only five years from now on, this will also balance out the risk factor in your portfolio a bit. Currently, apart from SBI Bluechip which is large-cap oriented, the rest of the funds carry slightly higher risk within the equity category.

Keep an eye on the funds rated 3-star by us (DSP Small Cap, Franklin Flexicap and SBI Bluechip). If the rating slips further in future, you can move out to a better fund in the same category, in case of the small-cap and the flexi-cap fund. In case of the large-cap fund, move to a passive fund. The unrated Axis Flexicap also needs a watch and a move is warranted, if it is rated below 3-star in future. In fact, instead of having two flexi-cap funds, you can merge your investments into one, going forward. We revise our ratings every six months, on an average. The last revision was on June 1, 2022.

Published on September 24, 2022

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.