For a better experience, Read this story in our App

TO ENJOY ADDITIONAL BENEFITS

Connect With Us

Get BusinessLine apps on

Archean Chemical Industries (Archean) will eliminate its second biggest expense - interest costs with the IPO proceeds. This will provide IPO investors an immediate bump up in potential earnings. But long-term investors should examine the long-term growth potential of the company, that is dependent on capacity expansion. Archean has turned around its earlier expansion project in FY22 and will be initiating its next phase shortly. Investors may wait and watch the development and need not subscribe to the issue now. The IPO will be open till November 11 and includes a fresh issue and OFS portion valued at ₹805 crore and ₹657 crore respectively at the higher price band.

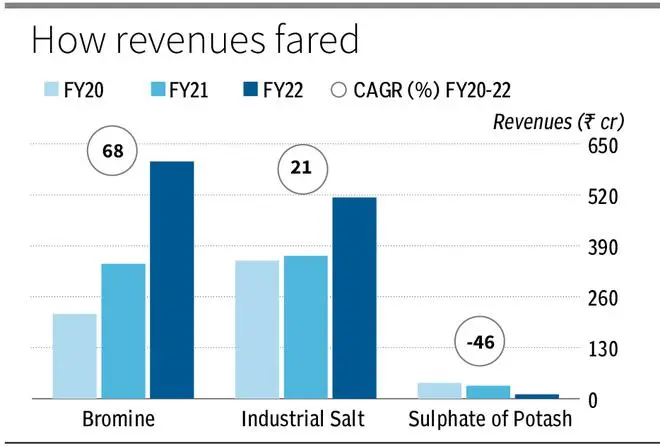

Archean operates from Rann of Kutch from where it sources brine reserves to manufacture bromine (54 per cent of FY22 revenues), industrial salt (45 per cent) and Sulphate of potash (1 per cent). Apart from Dead Sea in the Mediterranean, this brine rich reserves in Gujarat help Archean to be amongst lowest cost producers of bromine, globally. The regulatory hurdles (land lease and environmental, export and pollution controls) and the lead time involved in developing the fields, can act as an entry barrier for others. Archean has a 30-year lease renewed in 2017. Bromine is a used as a reactant and catalyst in chemical process and as a flame-retardant material. Similarly industrial salt is used in Chlor alkali (used for soda ash and bulk chemical manufacturing), oil wells and de-icing.

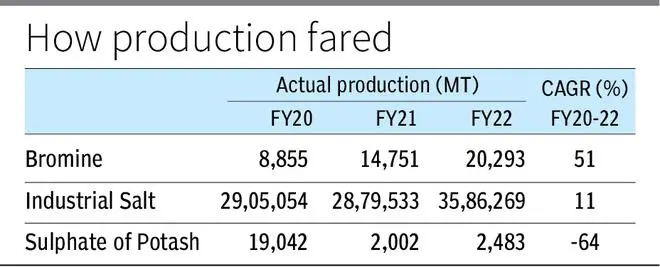

Archean achieved a significant improvement in bromine capacity, after financial and time delays in development (discussed below). Bromine, a value-added product compared to industrial salt, delivered a capacity growth from 10,500 MTPA in FY20 to 28,500 MTPA in FY22. Along with tripling capacity, average realization also showed a 11 per cent CAGR growth in Bromine in the period, driving 68 per cent CAGR revenue growth in two years. Industrial salts also had improved production for a 20 per cent CAGR revenue growth in FY20-22. Operating from brine reserves, Archean has negligible cost of raw materials (1 – 4 per cent of revenues) with packaging and freight costs being the biggest cost head. This improved from 42 per cent of revenues in FY20 to 32 per cent in FY22. With a higher contribution from bromine, Archean’s EBITDA margins improved from 24 per cent in FY20 to 41 per cent in FY22.

Archean’s further expansion plans are with established and new product range. The established product capacity is expected to increase by FY23 end. The cost is expected to be at a meagre ₹17 crore only. Bromine from current 28,500 MTPA to 42,000 MTPA, industrial salts from 3 million MTPA to 5 million MTPA. Sulphate of Potash, ran into site issues as raw material feed needed correction in FY22, which is expected to be scaled back again.

Archean also intends to develop bromine derivatives; High end Flame retardant - 10,000 MTPA, Clear Brine fluids – 13,000 MTPA and Pure terephthalic acid (PTA) – 5,000 MTPA all by 2HFY24. The project cost of ₹250 crore is expected to be financed by internal accruals. The development for flame retardant is backed by an agreement with Chinese technology provider to design, develop and operate the plant including a 90 per cent buyback clause. The plant located in GIDC Ankleshwar, Gujarat will start construction in December.

Archean commenced operations in 2013 and faced difficulties in developing capacities starting from 2017 to project completion in 2021. The company faced long delays in servicing debt related to the development. In 2017 Archean had to restructure the debt from six nationalized banks and find alternate capital to fund the project. The current selling shareholders, stepped in with debt in 2017. But IPO investors have to take note of history of capital funding proceeds sourced from banks, private debt, and equity shareholder in a span of eight years till it turned around.

The total cost of debt for Archean is at around 17 per cent after debenture issuance (convertible and non-convertible). Hence, interest cost which is the second biggest expense for Archean, can be cleared with the IPO as the company plans on becoming debt free using the fresh issue proceeds. The debt issuers (India Resurgence Fund and Piramal Natural resource Fund) with equity stake from converted debt will retain close to 60 per cent of pre issue shareholding after the OFS portion.

Archean is valued at 27 times FY22 earnings on a post-issue shareholding basis and will be lower adjusted for interest cost which will decline post IPO. Considering the large scope for capacity addition planned the valuation may seem justified. But considering the development history and upcoming portfolio of projects being undertaken we recommend long term investors may wait for development visibility before considering the stock.

Published on November 9, 2022

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.