IW01_Stock_insight_Grasim_NET.jpg

The stock of Grasim Industries is down 22 per cent over the last one year and trades at nine times its trailing earnings (consolidated) of one year. With current valuation at the lower end of its PE band (9-11 times) in the last two years, it might be a good time to pick up the stock.

Ascribing a valuation of five times earnings to its standalone business — viscose staple fibre (VSF) and chemicals — and valuing its holdings in UltraTech Cement (subsidiary) and other group companies at 30 per cent discount to market price, the fair value per share of Grasim Industries comes to Rs 3,200.

The recovery in the US economy should help Grasim’s fibre and textiles business. The company’s VSF volumes are already rising. In the recent September quarter, at 93,025 tonnes, the sales volume was up 20 per cent sequentially and 9 per cent year-on-year. The company’s capacity expansion over the next year should help it capitalise on an improving market scenario.

Also, the cement business should see better times with the good monsoon expected to stoke rural demand in the coming months. Grasim holds 60 per cent stake in UltraTech Cement — an all-India cement player with capacity of 54 million tonnes per annum.

In the September quarter, Grasim’s consolidated revenues were up 5 per cent, Y-o-Y. But net profit was down 27 per cent due to steep earnings decline in the cement segment. Flat sales volumes, lower realisations and increase in cost of inputs proved a drag.

Cement prices may recover in the next six months with expected improvement in rural demand and with government initiatives to kick start infrastructure activities starting to pay off.

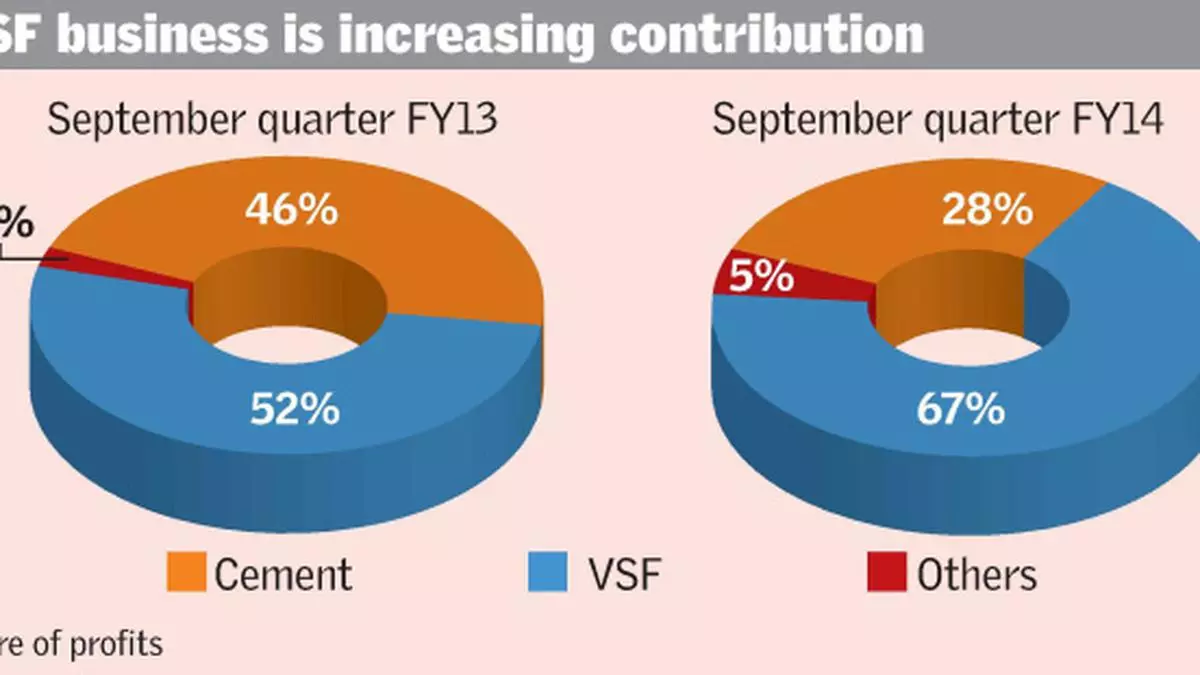

VSF exports growing

The VSF segment’s share in Grasim’s consolidated profits has gone up significantly in the last six months. This follows depressed business conditions in the cement arm and loss in a recently-acquired pulp mill in Canada. From 49 per cent in FY-13, the VSF segment’s share in the company’s profits has increased to 60 per cent in the first half of FY-14.

Grasim Industries has virtually a monopoly in the VSF market in India and is also a leading global player with 20 per cent share in the world market. VSF is used as a substitute for cotton, thanks to its superior properties in terms of moisture absorption, softness and comfort. The demand for this fibre globally has grown at an annual rate of 8 per cent over the last five years. Growth in the future will be driven by demand from the EU and the US — the world’s largest textile markets.

In this context, the better-than-expected economic growth in the US in the September quarter is a positive. Also, there have been reports of Indian textile exporters receiving enquiries from European buyers.

Grasim’s VSF production capacity stands at 3,77,775 tonnes, up 7 per cent over the last year following the expansion of its Harihar plant in Karnataka. The ongoing expansion at Vilayat, Gujarat (120,000 tonnes per annum), which is likely to be completed by FY15, will also benefit the company. In the September quarter, the VSF segment recorded 4 per cent growth in sales and operating margin was 19.6 per cent — the highest in the last four quarters, thanks to the weak rupee.

Over the next one year, sales growth for the company should be driven largely by volumes. Also, VSF prices may not correct significantly in the global market as prices are already at multi-year lows.

Rural push to cement

Grasim derives over 70 per cent of its consolidated revenues from its cement business through UltraTech Cement. In the first six months of 2013, even as the Holcim Group cement companies recorded drop in despatches, UltraTech held on to its volumes, thanks to its all-India presence.

Cement demand, though lacklustre now due to drop in overall economic activity in the country, should revive in the coming quarters.

The bountiful rain over the last few months is expected to increase disposable income in the hands of rural consumers and stoke housing demand. Housing makes up for two-thirds of cement demand in India and of this over 40 per cent is consumed in the rural markets. The trend of the rural population shifting to pucca homes should also aid cement demand growth in the long term. This will benefit pan-India players such as UltraTech.

In the September quarter, Grasim’s revenue from the cement business was down two per cent. At 9.88 million tonnes, volumes were up just 1 per cent over the last year. Also, the steep 7 per cent Y-o-Y decline in realisation hurt growth. Operating profit was down 31 per cent.

The savings in energy cost due to lower prices of pet coke and imported coal didn’t help much as cost of inputs such as flyash and limestone increased. Raw material cost as a percentage of sales was 16.8 per cent, up from 14 per cent in the same quarter last year.

Cement prices across India have increased 5-6 per cent in the last one month. The pent-up demand after the monsoon helped. If the price rise sustains, margins should improve for cement manufacturers, given that energy cost is on the wane.

Thermal coal prices in the international market are on a declining trend. There is excess supply in the market as Chinese demand has dropped. Prices are now $85/tonne, down from $93/tonne in January this year and $120/tonne in January 2012.

More Like This

Published on November 30, 2013

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.