For a better experience, Read this story in our App

TO ENJOY ADDITIONAL BENEFITS

Connect With Us

Get BusinessLine apps on

The realty sector has been on fire over the past year or so. After a decade of dull movements over 2010-20, the Covid era and beyond have seen people seek bigger and comfortable houses. And with work-from-home and hybrid cultures thriving, real estate has had a sustained upswing.

Among the mega cities that have led the revival in residential construction segment, Mumbai is a key area for several top and mid-sized builders.

In this regard, Suraj Estate Developers is coming out with an initial public offering of shares and is looking to raise ₹400 crore from the issue at a price band of ₹340-₹360.

The company is mostly into redevelopment projects in the value luxury and luxury categories of residential housing. It also builds commercial properties and boutique offices for corporates.

Suraj Estate Developers is focused exclusively on the south-central Mumbai market and has executed well over the past few decades.

At ₹360, the offer discounts its FY23 per share earnings by 35 times on the pre-offer equity base and nearly 50 times on a post-offer fully diluted equity base. However, though it may not be representational, if the June quarter per share earnings of FY24 are annualised, the Suraj Estate Developers offer would trade at a price-earnings multiple of 27 times on a fully diluted basis.

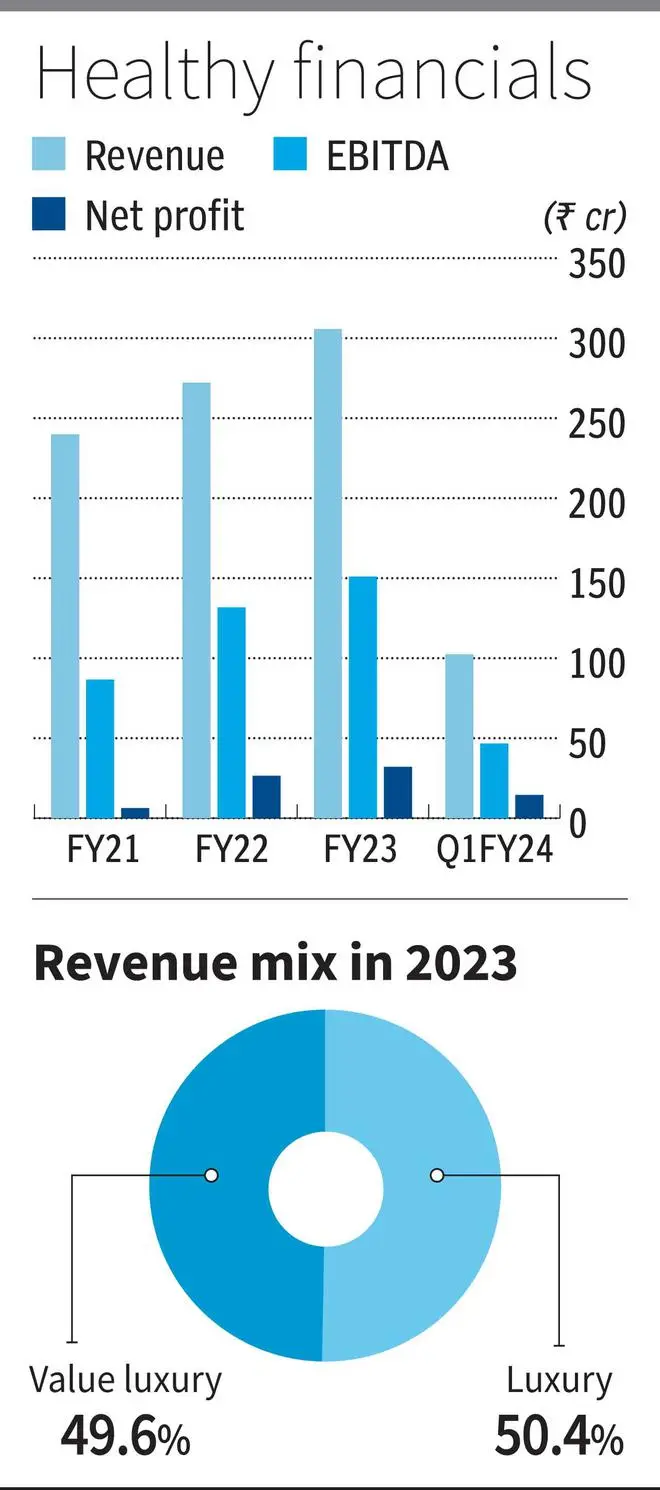

From FY21 to FY23, the company’s revenues grew at a CAGR of 12.9 per cent to ₹305.7 crore in FY23, while net profits rose more than five-fold to ₹32.1 crore from a low base in a relatively tough FY21, which was marked by lockdowns. The company enjoys an operating (EBITDA) margin of above 45 per cent consistently (49.4 per cent in FY23), which is among the best in the industry and among a select few to enjoy double-digit net margins. In 1QFY24, the company recorded ₹102.4 crore in revenue from operations and net profit of ₹14.5 crore, with an EBITDA margin of 45.6 per cent.

The return on capital employed in FY21 was a healthy 21.9 per cent and has been improving steadily.

Suraj Estate Developers’ valuations are certainly not cheap, but aren’t that expensive either.

Sharp focus on lucrative market segments, an asset-light model focused on redevelopment projects and a strong execution track record are positives for Suraj Estate Developers. Investors with a long-term perspective can consider subscribing to the issue, and not for listing pops, if any.

The peer set in real estate companies is quite difficult to pinpoint as some are multi-city focused and some have operations only in a single city. Also, the market segments of operation are different. The BSE Realty trades at a PE of over 84 times. And players of varying sizes and styles of operation trade from 28-80 times their FY23 earnings, with some outliers trading at three or even four-digit numbers, while others recorded losses.

Suraj Estate Developers is hyper focused in the sense that it operates in the sub-markets of South-Central Mumbai (SCM). Mahim, Matunga, Dadar, Prabhadevi and Parel are areas where it has executed projects. The company has been around for more than 36 years and has constructed more than 1 million square feet across 42 residential and commercial projects.

It has ongoing projects with about 6.1 lakh sq ft and upcoming projects of 7.44 lakh sq ft.

The company operates in three segments — value luxury, luxury and commercial. The value luxury residential segment is essentially those seeking 1 or 2 BHK apartments costing ₹1-3 crore. This segment accounts for over 54 per cent of the ongoing projects’ carpet area for sale.

Luxury segment is the part where buyers look for 3 BHK and 4 BHK apartments costing between ₹3 crore and ₹13 crore. This segment accounts for 39.4 per cent of the carpet area for sale.

Commercial buildings account for the remaining 6.3 per cent.

Suraj Estate Developers is predominantly focused on redevelopment projects in the residential segment. The builder focuses on the SCM area where there are apartments that are quite old (30 or more years) where residents find buildings too difficult to repair and maintain. The company gets involved in such projects, resettles tenants, develops a new property by demolishing the old one and gives residents new apartments with larger areas to live in. The extra apartments built due to higher FSI (floor space index) that is allowed in redeveloped buildings, would be sold to new buyers.

The company is fully dependent on external construction companies and architects for completing its projects.

The company is able to buy land parcels at cheaper rate and its focus is on redevelopment projects. Given that the SCM market in Mumbai has consistently had per sq ft rates north of ₹42,000, the margins have been extremely healthy for the company.

Suraj Estate Developers looks to use the issue proceeds to reduce debt substantially. Of the ₹400 crore to be raised from the issue, ₹285 crore would be used to repay its rather high net debt of ₹551 crore as of June 2023. Another ₹35 crore would be used to buy land parcels or land development rights.

Post the repayment of debt, on an enhanced equity base, the company would have a net debt to equity ratio of about 0.6, which is quite reasonable.

According to a recent ICICI Securities report, for a list of 10 listed players in the industry, the net-debt to equity ranges nil to as high as 2.5, with most in the 0.1-0.7 band in Q2FY24.

Published on December 16, 2023

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.