For a better experience, Read this story in our App

TO ENJOY ADDITIONAL BENEFITS

Connect With Us

Get BusinessLine apps on

Most of the large PSU banks and some private sector banks have raised interests on their term deposits to support credit growth, which is traditionally accelerated in the last quarter of the financial year, and protect their margins.

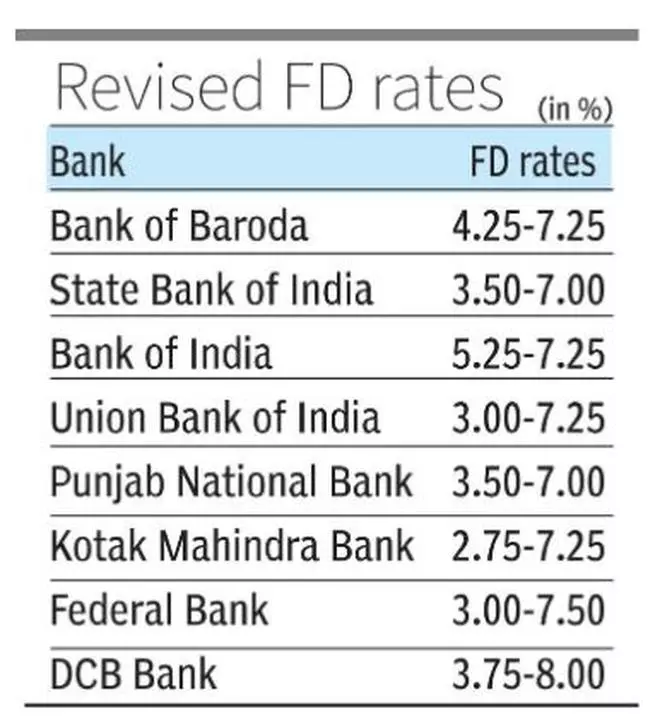

Over the last few weeks, lenders such as State Bank of India, Union Bank of India, Bank of India, Kotak Mahindra Bank and Punjab National Bank have hiked interest rates on domestic and/or NRI retail term deposits of less than ₹2 crore, by 10-75 bps, across various tenures.

Bank of Baroda was the outlier, raising rates by up to 125 bps. The PSU bank said that rate hikes are largely focused on shorter-term maturity buckets, especially those less than 1 year, to benefit shorter maturity depositors and help the bank manage its deposit portfolio.

“This step will not only attract more customers as they earn more on their savings but will also help the bank optimise its cost of deposits, thereby safeguarding our NIM,” said Ravindra Singh Negi, Chief General Manager - Retail Liabilities & NRI Business, Bank of Baroda.

Banks’ requirement for short-term funds has increased for asset-liability management, given the surge in disbursement of retail and personal loans, which tend be of up to 3 years. Smaller private sector banks and small finance banks had aggressively raised FD rates earlier in 2023 as deposit accretion became more competitive. However, larger PSU and private banks had so far largely been on the sidelines due to surplus liquidity and steady deposit growth.

Highest term deposit rates offered by most small finance banks are in the range of 7.60-9 per cent, for private banks are at 7-8 per cent, and for PSU banks are at 7-7.40 per cent.

Last week, SBI Chairman Dinesh Kumar Khara had said that hike in FD rates is because the bank believes in offering a “fair deal” to depositors. SBI offers interest of 3.50-7 per cent on its term deposits. The lender also has a special 400-day ‘Amrit Kalash’ FD Scheme where it is offering 7.10 per cent till March 2024.

“We have to take care of our depositors too. So that is the reason why we have done some calibration in terms of interest rates,” Khara had said, adding that the recalibration was also done because the lender had some “elbow room available”.

Bank of India too has introduced a ‘Super Special FD’ at 7.50 per cent for 175-day deposits of over ₹2 crore and less than ₹50 crore for HNIs and corporates, whereas Kotak Mahindra Bank increased rates on senior citizen FDs by up to 85 bps.

Analysts believe more banks could follow suit and FD rates could see some more increase before stabilising, especially given the hike in small savings rates for Q4 FY24.

Bank deposits rose 14.1 per cent yoy, touching a six-year high, in the fortnight ended December 15, 2023. However sequentially, deposit accretion was lower by 0.4 per cent. The credit-deposit (CD) ratio has remained below 80 per cent since September 2023, but improved 14 bps during the fortnight to a 3-year high of 79.9 per cent as of December 15. Excluding the HDFC merger, the CD ratio was 77.4 per cent compared with 75.8 per cent a year ago, according to CARE Ratings.

Published on January 2, 2024

introduces a lucrative 175-day fixed deposit offering 7.5% interest for deposits ranging from ₹2 crore to less than ₹50 crore. This move follows State Bank of India (SBI) and Bank of Baroda’s recent hikes in deposit rates.")

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.