For a better experience, Read this story in our App

TO ENJOY ADDITIONAL BENEFITS

Connect With Us

Get BusinessLine apps on

")

(PIC: Canva.com)

The looming threat of recession in the global markets and the possible impact on hiring could pose a challenge for Indian students who have been betting big on overseas education courses in the recent past.

While it is still too early to predict the exact impact, but industry experts feel that repayments could be affected leading to a spike in non-performing assets (NPAs) if the situation does not abate soon.

NBFCs and fintechs, which account for a major share of overseas education loans, might feel the brunt, particularly if they have not done the due diligence while underwriting the loans.

Shantanu Rooj, Founder & CEO of TeamLease Edtech told businessline, “The recessionary fears and the possibilities are real for the western markets. Student loans will be at risk if the recession actually hits the market. However, at this point in time, there are fair chances of the clouds of recession fading away post-first quarter of the coming financial year.”

Rooj added, “India is largely insulated from this at this point and the risks are quite low for student loans in India. However, students must keep adding evidence of additional skills that they pick up either through short-term supplementary courses, through industry internships, or through industry LinkedIn project work.”

While in the short-term, there might be a surge in NPAs and lead to loans being restricted, in the medium to long term, this is not likely to be a major risk for India, he added.

Financial institutions typically offer a six-month moratorium on such loans so students can bag a suitable job post-completion of course and settle down before starting their repayments.

However, for students graduating now, it might be a challenge as getting jobs, particularly in some of the markets could be comparatively difficult thereby affecting the repayments.

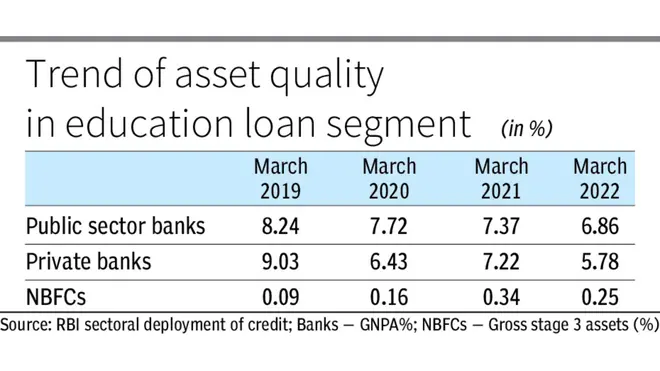

The NPAs from overseas education loans are typically very low, as compared to the domestic loans, industry insiders said.

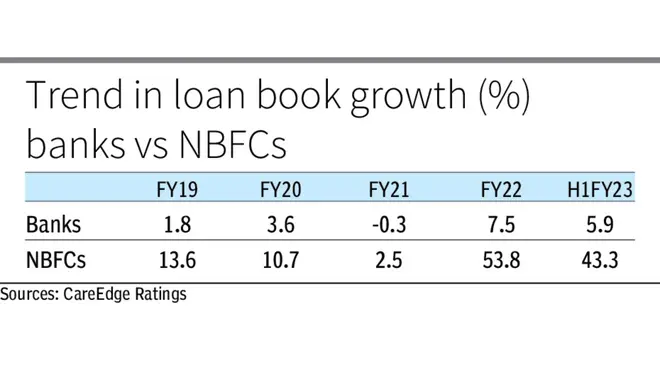

According to a recent report by CareEdge Ratings, NBFCs almost doubled their market share in retail education loans in the last two years from close to 10 per cent in September 2020 to nearly 19 per cent in September 2022. Market share gains of NBFCs came from establishing a strong foothold in overseas student education loans.

Though NBFCs follow specialised credit underwriting skills, have better asset quality parameters as compared to banks, and have been able to maintain the asset quality reasonably stable even during the Covid times.

However, a large proportion of outstanding loans has limited seasoning, global macroeconomic uncertainty and volatile job market conditions are major risks to asset quality in the near term on account of the recent large-scale layoff announced by a few MNCs, the report said.

The rise in overseas education demand is also aided by the increased availability of funding supported by specialised NBFCs adopting a student-led approach in risk underwriting enabling companies to estimate future employability and earnings potential, which includes an overall academic screening of students rather than traditional collateral-based lending adopted by banks thus leading to expansion in the pool of students eligible for funding.

While it has led to an expansion of the market, the flip side is any impact on future employability and earnings potential might hurt sentiments and affect repayments.

According to Ankur Dhawan, president, upGrad Abroad, if a candidate does not manage to bag a suitable opportunity, he might resort to taking up a lower quality job to be able to service the loans or it would be serviced by parents who are co-applicants.

Recession may in fact be a good time for students to go abroad as they will take atleast two years to complete the course by which time the markets are likely to start looking up, said Mayank Sharma, Country Head, Prodigy Finance.

“For students graduating now, it is tough with major layoffs happening. These loans typically have a moratorium of six months but if the stress continues for a longer period then we will have to see, it is a wait-and-watch situation right now,” he said.

According to Ankit Mehra, CEO and Co-founder, GyanDhan, the level of stress on asset quality would depend on the kind of underwriting practices followed by entities.

He pointed out, “There has been wage inflation in the high tech sector and that will essentially calm down but whether there will be mass employment issues that need to be seen. Some of the lenders might be forced to go slow on disbursements if risks in asset quality increase.”

Mehra added, “It is not likely to happen in the next one year as these loans have a moratorium, but if the situation turns into a crisis like we had seen in 2008 then it could have a severe impact.”

Published on March 22, 2023

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.