bl13tara.jpg

“Insanity in individuals is something rare — but in groups, parties, nations and epochs, it is the rule”.

Friedrich Nietzsche

Ever since the global financial crisis of 2008, the mainstream economic thought has been that all that is needed is large doses of central bank monetary creation. After five years of monetary madness, the pundits are still looking for green shoots of recovery.

Paul Krugman and his sympathisers go on insisting that the money creation has been timid and that an acceleration of created money would resolve the problem. At the same time, there are shivers as to what would happen when the US Fed’s quantitative easing (QE) tapering takes place.

The immediate outlook for India is that we have to reconcile with a 5-5.5 per cent growth rate for the next two years. At the same time, India is afflicted by more than 10 per cent retail inflation. Strong anecdotal evidence points to the ‘true’ inflation rate to be significantly higher, which is reflected in the social unrest.

Inflation dilemma There have been episodes when political uncertainties have resulted in governance problems and monetary policy has borne the brunt of the adjustment — 1979-80, 1990-91, 1995-96 and 1997-98 — and on each occasion monetary policy has curbed inflation. This time around, the Reserve Bank of India (RBI) faces a major dilemma.

The Government is averse to any increase in borrowing cost. Again, industry appears to have a significant clout which is preventing strong monetary policy action. Moreover, swingeing monetary policy action has become unfashionable even though policy interest rates have become ridiculously low and, in fact, negative in real terms. As such, there is little support for higher interest rates.

Generalised inflation, as is the case in India, at the present time, warrants strong monetary policy action. Mainstream economists in India often talk about food inflation, fuel inflation, onion inflation and what have you, but are reluctant to consider this as generalised inflation, irrespective of the fact that inflation is hitting virtually all sectors.

Once it is accepted that inflation is generalised, the logical response is strong monetary policy action. Mainstream economists get hot under the collar when told that generalised inflation is a monetary phenomenon. In India, economists fail to distinguish between monetarism and strong monetary policy. Paul Volcker, the US Fed Chief who raised interest rates in 1979-80 to squeeze out inflation was horrified when, on a visit to India, he was identified as a monetarist for raising interest rates!

Window of opportunity With multiple windows for RBI accommodation, it must be emphasised while the industry’s perception is that policy interest rates have been raised since Rajan took charge, the weighted average cost of the RBI accommodation has come down. Moreover, there has not been any tightening of reserve requirements. It would appear that Rajan would not be inclined to actively use the instrument of reserve requirement. As such the only option is to decisively raise policy interest rates.

To the extent that the RBI prefers to use small incremental increases in policy interest rates, it would be necessary to use every window of opportunity to raise policy rates. This is imperative, as sooner or later the US Fed tapering will start.

Accordingly, on December 18, 2013, at the time of the Mid-Quarter Review of Monetary Policy, the RBI should raise the policy repo rate by at least 0.25 percentage point (a 0.50 percentage point increase would be a better option but if this is not possible, it would need to raise policy interest rates well before the full Quarter Review on January 28, 2014).

Too late for rate hikes? It is not often appreciated that the RBI has been absorbing large quantities of government securities through its Open Market Operations (OMO). This nullifies whatever monetary tightening is undertaken through raising policy interest rates. Moreover, this violates the spirit of the Fiscal Responsibility and Budget Management Act.

Official pronouncements are that the balance of payments current account deficit (CAD) in 2013-14 could be as low as 2.5-2.7 per cent of GDP. It is erroneously argued that a reduction in the CAD implies an increase in the savings rate. It is equally possible that investment rates have fallen. Given the inflation rate, the savings rate will go up only after a substantial increase in policy interest rates. The fear one has is have we left it too late to raise policy interest rates?

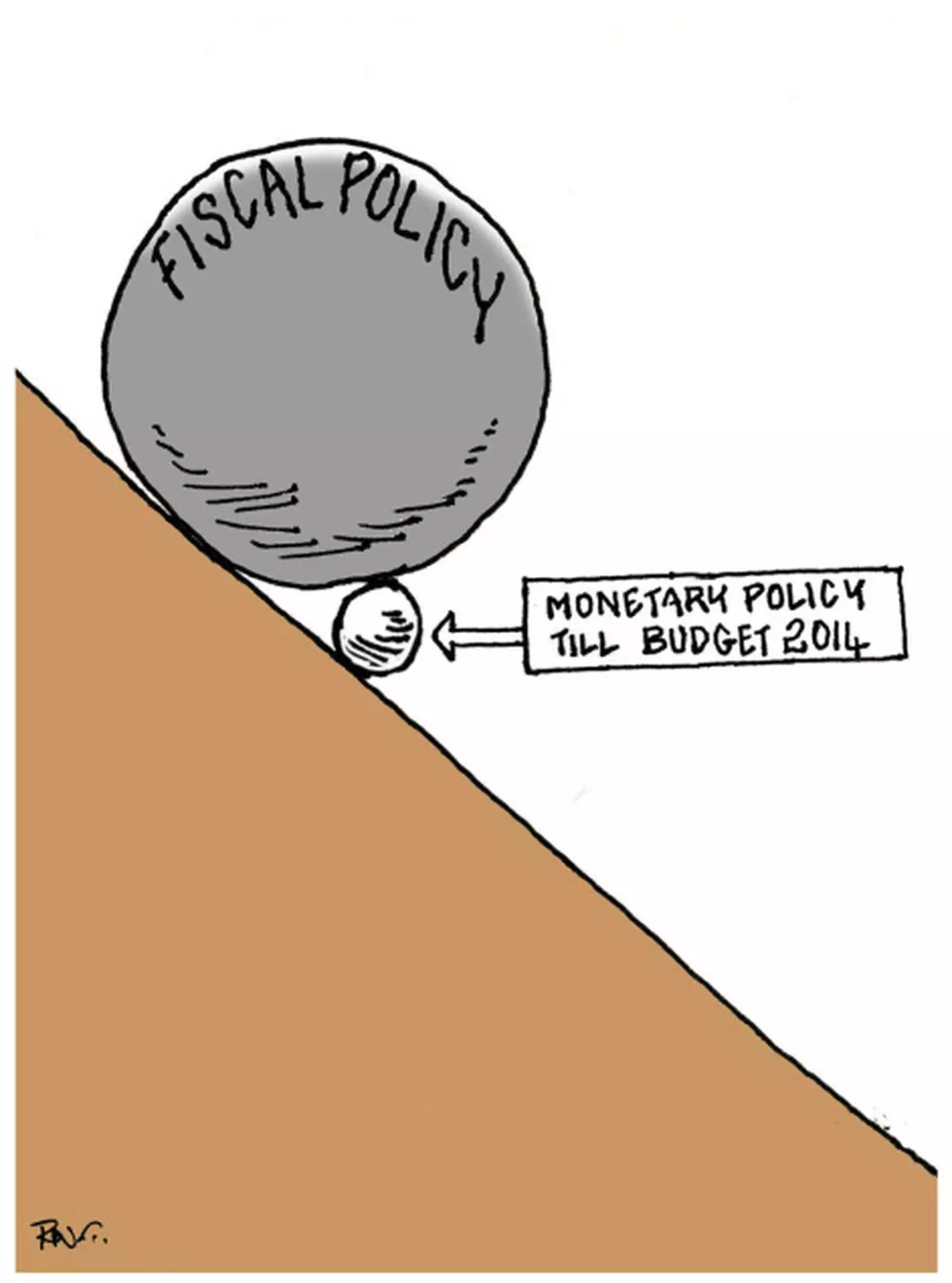

In the ensuing months, there would be severe constraints on the effective use of fiscal policy and this will put an increased burden on monetary policy. Those opposed to an active monetary policy would argue that a series of increases in policy rates did not curb inflation and, therefore, policy interest rates should not be raised.

We need to reflect on former RBI Governor Subbarao’s statement towards the end of his term that, perhaps, monetary policy was not tight enough. To keep the economy on an even keel, Governor Rajan should not hesitate to be like the little Dutch boy who put his thumb in the hole in the dyke till relief came. Rajan has to somehow hold the fort till the regular Budget is announced in May/June 2014.

(The author is an economist.)

More Like This

Published on December 12, 2013

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.