For a better experience, Read this story in our App

TO ENJOY ADDITIONAL BENEFITS

Connect With Us

Get BusinessLine apps on

iStockphoto

I do not know how history will judge me, but let me say that I've spent a lot of time and energy trying to transform Tatas from a patriarchal concern to an institutional enterprise, said Ratan N Tata.

Business transformations have been par for the course in the last forty years. Ever since Industry 3.0 began, with the large-scale introduction of computers, automation and computer-controlled operations, many companies have found the need to transform their cultures, in view of the growing importance of the customer to the business.

Naturally, many ‘gurus’ appeared, with many theories on change management, business transformation and such.

One of the important movements to modernise businesses and help them to deal with the increasing complexity was ‘Business Excellence’ (BE). Originally the movement began in Canada, which the government decided to recognise and promote excellence in business, considering the increasingly competitive conditions emerging.

This was followed by the Malcolm Baldrige Model for Performance Excellence. This model was adopted in industry, first in the US, and then in all parts of the world through the development of regional and country-specific models.

The EFQM is another model. In India, we have the Rajiv Gandhi model, the Golden Peacock model, and the CII-EXIM model, which is the same as the EFQM. It is interesting to find that EXIM bank was the first bank to sponsor an award for Business Excellence.

Over the years, Business Excellence has grown manifold, with innovations like the Balanced Score Cards in 1991 (Kaplan and Norton), concept of core competencies by CK Prahalad, and, recently, by Dr Govindarajan with his ‘The Three Box Solution’. Another significant development was the work by John Kotter, with his eight-step method for managing change.

With all these and more, many Fortune 500 companies adopted these BE models and have reaped huge benefits.

What’s different with these models and what attracts companies to adopt them? And why should Indian banks be aware of and use these to ensure better returns for their lending?

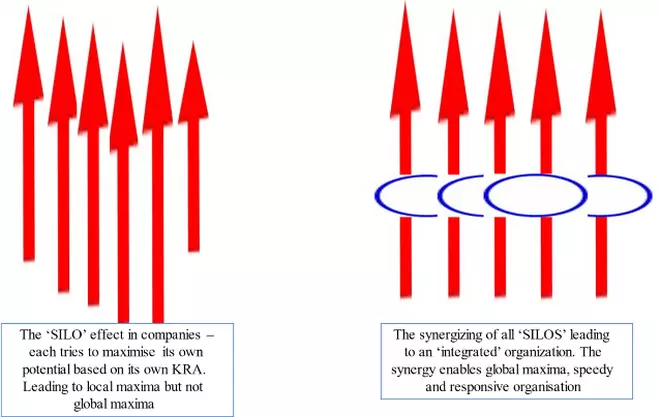

Modern companies use business processes in preference to silos management. Silos management existed when competition and customer friendliness were not essential for sustained profitability and growth. While individual departments worked to their potential, the overall company position was often compromised.

This is in line with the truism that ‘local maxima do not always lead to global maxima’. Quite the contrary, in many cases. To remedy this situation and make companies more agile and responsive to external stimuli, the BE models were invented.

Using these models, companies become more ‘integrated’, balancing the outputs from individual departments (or silos) in the companies, and gaining synergy. The synergy so gained led to the efficient overall growth of the organisation. Only such companies could prosper in competitive times.

So, where do Indian banks come into the picture?

Actually, they should have come in right at the beginning, when the BE movement started. For banks to get a better surety on the servicing of their long-term loans — both interest payments and repayment of the principal — they need an assurance from the companies to whom they lend that such ability will sustain.

Only on this basis can banks reduce risks, and avoid the accumulation of non-performing assets or NPAs. It is unfortunate that Indian banks did not take notice of the developments in industrial and business practices over the years.

It all began with Total Quality Management or TQM. This was followed by Business Excellence (or BE), which built upon the framework established by TQM, and linked the missing aspects, like leadership, strategy, stakeholders and sustainability.

The BE way of looking at any organisation is to provide guidance and facilitation to design and deploy ‘Best Practices’, systematic working, and integrated and synergised approach to organisational work which will increase efficiency and effectiveness.

Only one Indian bank — EXIM Bank — took notice and did something about it. EXIM bank joined hands with the Confederation of Indian Industry (or CII), to use the EFQM model to recognise ‘Best Companies’, through an awards system.

The CII-EXIM Bank awards became an important arbiter of excellence in organisations. Many companies joined the process and applied for the award. So far, there have been many companies who have won the award, and many are on the way.

Various studies have established that there is a correlation between the practice of BE and sustained business performance. BE models have enhanced the scope of business activities from direct profit earning to those that enable long-term sustainability of the industry as a whole, by using the Triple Bottom Line (TBL) principles, of late.

Regularly and periodically, BE models are updated to include the latest trends in corporate management — social, environmental, community, and stakeholders’ interests to be addressed.

If banks insist that companies who borrow money from them, should report on their performance using the BE model guidelines, it will ensure that the borrowers develop abilities to ‘excel’ in their performance in a systematic way. This will lead to better possibilities of sustained interest payments and principal returns. And this is exactly what banks want.

Such an approach has a double benefit. Companies improve their performance in multiple dimensions, and banks become drivers of the ‘friendly’ growth of the business. In view of the lower NPAs, they are able to reduce interest rates in the long run and improve their profit.

In a recently held ‘GBSN Seed Class for Sustainable Finance and ESG Investments’, (Global Business School Network) a conference of senior finance professionals gathered to discuss the ways in which Indian banks can help companies to address the increasing need for carbon neutrality, saving the environment, reducing environmental degradation, improving the sustainability of enterprises in the long run.

The group noted that ‘In Canada, banks take environmental protection into account when making lending decisions’.

An Internal Bhavans SPJIMR document said, “According to the Loan Market Association, Sustainability-linked issuance increased rapidly in the European leveraged loan market in the first half of 2021 and is now poised for growth among mid-cap companies, and small and medium-sized enterprises.”

It is recommended that banks also insist on borrowers, especially the larger corporates, to file an annual or bi-annual ‘performance excellence’ report, based on a chosen BE model, to reflect the continued commitment of organisations to prevent NPA and make consistent progress in establishing ‘excellent and sustainable businesses.

(R Jayaraman is Head of Capstone Projects at Bhavan’s SP Jain Institute of Management and Research)

Published on October 12, 2022

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.