soar sensex.jpg

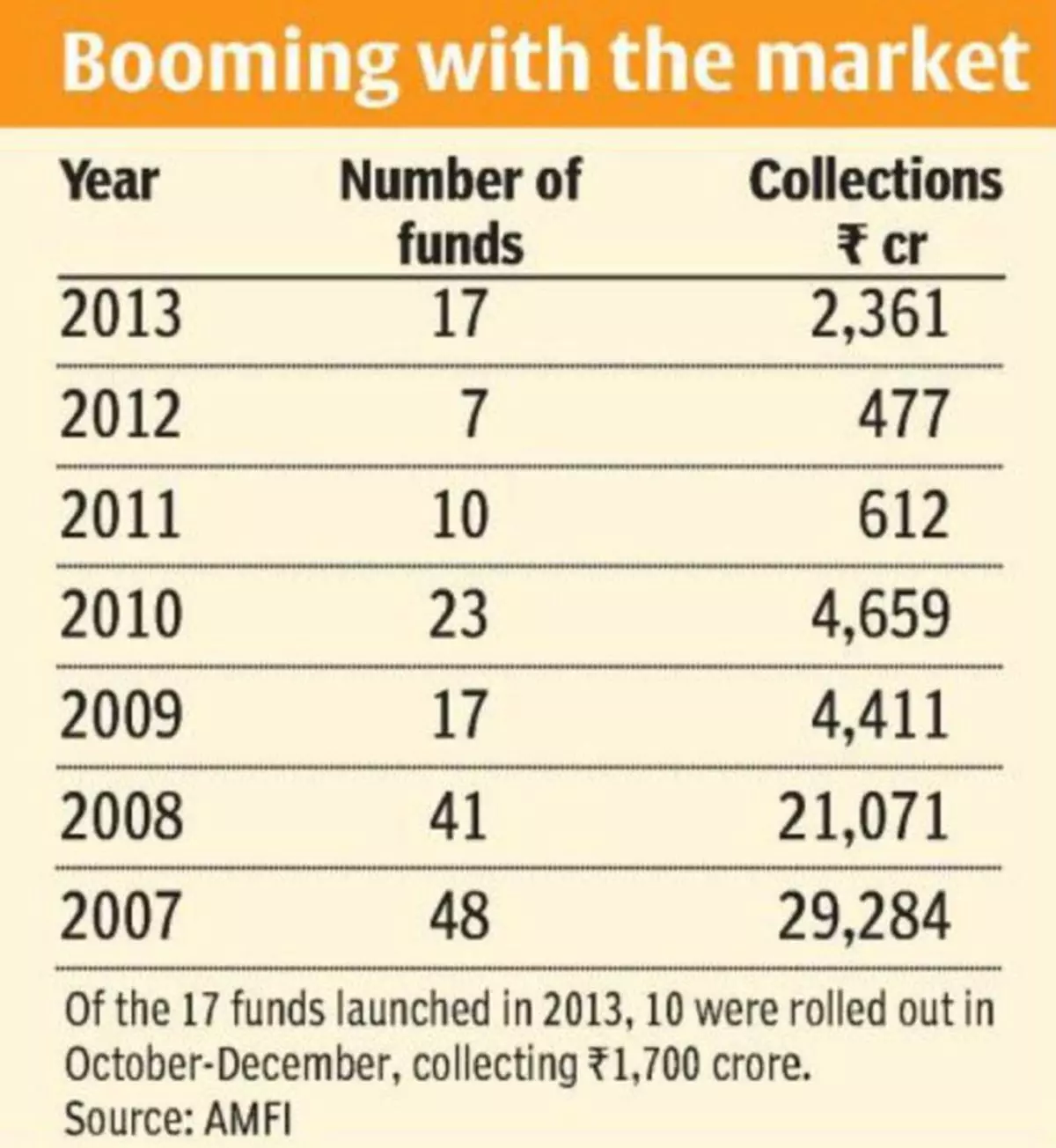

After a hiatus of four years, mutual fund houses are once again flooding the market with new fund offers (NFOs). A dozen new equity funds have been floated in the last three months, more than twice the number of funds launched over the whole of last year. Six more new funds will be peddling fancy themes, ranging from value investing to European stocks, over this week and the next.

Predictably, these offers are crowding in when the Sensex is perched close to its all-time high. The last time funds went on an NFO spree was in 2007-08, when scores of infrastructure-themed funds garnered money just before the markets crashed. A majority of them now languish below par.

Market peak?But fund managers vociferously deny that this NFO boom is anything like the earlier one. “At a Sensex level of 21,000 in 2007-08, the price-earnings multiple was in excess of 20 times. Today, the valuations are not as expensive. Besides, we were at the peak of an economic cycle then. Now we are trying to offer investment ideas that work at the bottom of an economic cycle. Our experience shows that products launched counter-cyclically tend to do much better,” says Kalpen Parekh, CEO, IDFC Mutual Fund.

Others explain that though the Sensex is at a new high, most stocks haven’t participated. Explains Manish Gunwani, Senior Fund Manager, ICICI Prudential Asset Management, “If we remove FMCG and large-cap IT stocks, the valuation of the market is really cheap. This is particularly true of mid- and small-cap stocks and cyclicals.”

The fund house rolled out ICICI Pru Value Series 1 just ahead of the rally in September. There are now many other schemes betting on a similar idea — Axis Small Cap, Pramerica Midcap Opportunities, Sundaram Select Micro-cap and the IDFC Equity Opportunity Series 1.

Keeping it closeInterestingly, many launches this time are of closed-end funds, where investors cannot pull out at will. Fund houses say that there is good reason for this. For instance, closed-end funds may be better able to own less liquid mid- and small-cap stocks. And with the economy likely to make only a slow recovery, closed-end funds allow time for the investments to play out.

But some industry players say that the preference for closed-end funds has more to do with distributor incentives.

Closed-end funds can incentivise distributors with hefty upfront commissions, unlike open-end funds which only pay an annual ‘trail’ fee for the period the investor stays with the fund.

As Parag Parikh, CEO and Director, Parag Parikh Financial Advisory Services, explains: “In many of these funds, fund houses are paying 3-5 per cent upfront commissions to their distributors, working in the fee for the entire three to five years.

These distributors are (hence) pushing the products because it is in their interest. The commissions are paid out of the Asset Management Company’s funds. So only the larger fund houses can afford this.”

He adds that closed-end funds may not be in the best interest of investors. “Closed-end funds (when listed in the market) usually quote at a 15-20 per cent discount to their Net Asset Value. Again, as the money cannot be taken out, there is a risk of such funds being stuck with under-performing stocks.”

But Parekh of IDFC MF counters this. “At IDFC MF, we have ensured that our total three-year incentive (for closed-end funds) is very similar to what we pay in our open-ended funds. Two, we have encouraged distributors to take trail incentives.

“So, we have given two price models. If they take a trail-fee model, we are happy to pay higher commissions vis-à-vis a pure upfront. This way, the interest of the Asset Management Company, the distributor and the investor are all aligned.”

More Like This

Published on January 26, 2014

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.