For a better experience, Read this story in our App

TO ENJOY ADDITIONAL BENEFITS

Connect With Us

Get BusinessLine apps on

When faced with a choice between choosing a weapon-less Lord Krishna and the most powerful army (Dwaraka army) in the world, Arjuna chooses the former. Consequently, Duryodhana is thrilled by Arjuna’s choice, as this would mean that the most powerful army would be siding with the Kauravas. The current situation in the market isn’t dissimilar. Investors now have to choose between mid- and small-caps, which are perceived to be ‘weapon-less’ with no further scope of re-rating. The other choice being large-caps as represented by the Nifty 50, and characterised by some of the strongest companies in India armed with relative under-performance (thereby perceived to offer ‘protection’ and growth). The Kurukshetra war ended in 18 days with the defeat of the Kauravas led by Duryodhana despite possessing a stronger army. What seemed obvious to Duryodhana didn’t really work. Similarly, what is seemingly obvious to many investors is a shift towards the Nifty 50. Will it work?

This requires us to slice and dissect the constituents of Nifty. The Nifty 50 is an ageing index. The average age of the top 10 constituents of the Nifty 50 is 62 years old. Sixty per cent of the Nifty’s constituents have been stable and constant for more than a decade — quite surprising in this age of disruption.

At 33 per cent, the Nifty 50’s weight of financials is one of the highest in the world. No meaningful developed market index has such a high weight of financials. Progressively, we have seen weight of financials getting replaced by innovation-led technology or industrials in many countries. The average number of bank accounts per person in India has risen from 0.6 in FY10 to 1.8 in FY24, reflecting increased financial inclusion. However, with much of the population now banked, growth in this sector is beginning to plateau. This is further underscored by the challenges banks face in attracting deposits, as more funds flow into other financial vehicles like mutual funds. Moreover, investors were in a way forced to play non-lending themes via lending institutions like banks. With the listings of multiple wealth management companies, broking outfits, AMCs, insurance (life and non-life), depositories, registrar and exchanges, the ‘scarcity premium’ of lending financials is a thing of the past.

The rise of artificial intelligence (AI) and the rapid growth of Global Capability Centres (GCCs) in India present a growing challenge to the large IT players in the Nifty 50. India controls over 50 per cent of the global GCC market, with a market size of $46 billion and a workforce of more than 1.66 million as of FY23. By 2025, the country is expected to host 1,900 GCCs with a market size of $60 billion, projected to rise to $110 billion by 2030. This swift growth in GCCs could further dampen the prospects of the larger IT firms, whose growth has already been slowing.

While the whole premise of moving to large-caps is due to rich valuations in mid- and small-, the starting PE of the consumer pack in the Nifty 50 continues to be rich. The trailing PE of the consumer sector in the Nifty stands at 55x, while the Nifty’s own PE is 24x. A 2.3x premium! As we are all well aware, starting PE determines end returns.

Household ownership of motorcycles and scooters has surged from 19 per cent in 2006 to 54 per cent in 2021, while car ownership has climbed from 2.8 per cent to 8 per cent over the same period. Meanwhile, the percentage of households without any means of transport has dropped significantly from 35.6 per cent to 19.8 per cent. These figures indicate that most households now own a personal vehicle, while others rely on an ever-improving public transport system. Moreover, the auto incumbents present in the Nifty 50 are witnessing rapid fragmentation with newer players trying to nibble their market share.

The above four sectors alone constitute two-thirds of the weight of the Nifty 50. Therefore, the bulk of heavy lifting has to be done by the balance one-third comprising Oil&Gas, Metals, Cement, Healthcare etc. A tall ask!

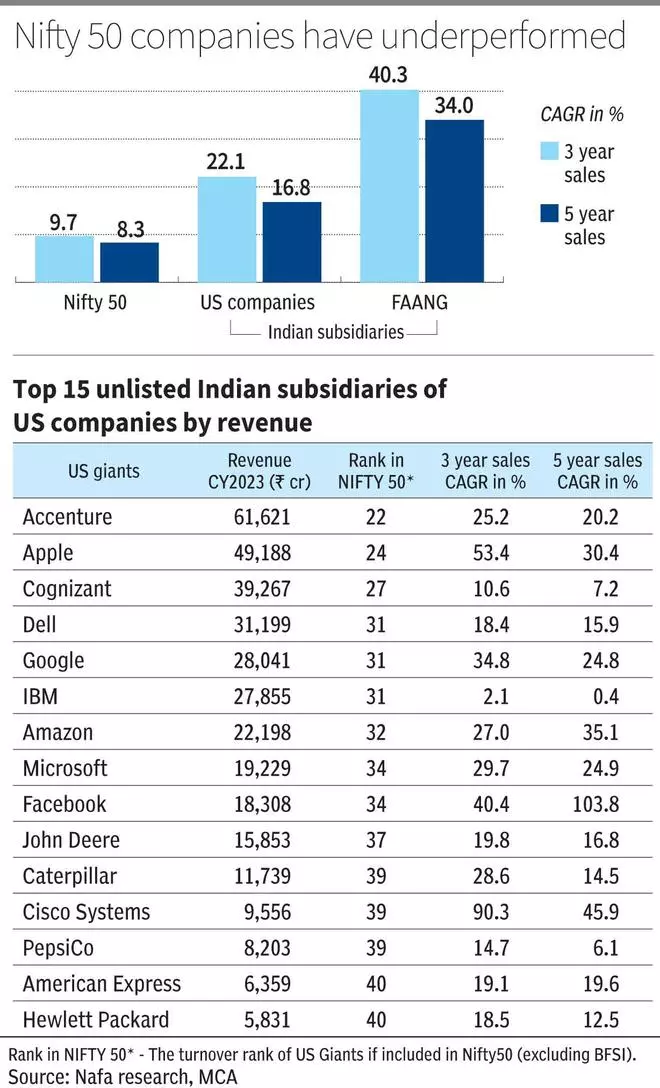

While large-cap companies in the Nifty 50 are experiencing slower growth, unlisted multinational players are expanding rapidly. US tech giants operating in India, such as the FAANG companies (Facebook [Meta], Amazon, Apple, Netflix and Google), are outpacing the Nifty 50 companies in terms of growth. These firms have posted three-year and five-year sales CAGRs of 40.3 per cent and 34 per cent, respectively, compared with the Nifty 50 (excluding BFSI) at 9.7 per cent and 8.3 per cent. This highlights the substantial growth of unlisted multinationals, while their listed large-cap counterparts stagnate. India’s FAANG has reached the scale and size of its legacy blue-chips within a short span of time.

Twenty years ago, it would’ve been possible to create wealth by being present in the top 30-40 companies in India, given the under penetration and relative lack of disruption. On the other hand, the mid- and small-cap segments were marred by lack of corporate governance, high share of unorganised segment etc. Today, the large-cap ROEs are attacked — their segments facing disruption and fragmentation. But the mid- and small-cap segments offer more investible opportunities notwithstanding many bubble pockets. In essence, large-cap growth in India is coming outside of the Nifty 50, while mid- and small-cap growth in India is available for investors amongst listed players.

Therefore, investors shouldn’t end up being like Duryodhana by choosing the seemingly obvious! Michael Batnick says, “The twelve most dangerous words in investing are: The four most dangerous words in investing are, it’s different this time.”

KR Senthilnathan has contributed to the article. The authors are part of the research team at NAFA Asset Managers

Published on October 5, 2024

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.