For a better experience, Read this story in our App

TO ENJOY ADDITIONAL BENEFITS

Connect With Us

Get BusinessLine apps on

requirements increasing by 55–60 bps")

Currently, the banking system capital is estimated to be ₹15.2-lakh crore, and the regulatory measures will lead to banks’ CRAR (capital adequacy ratio) requirements increasing by 55–60 bps | Photo Credit: EMMANUAL YOGINI

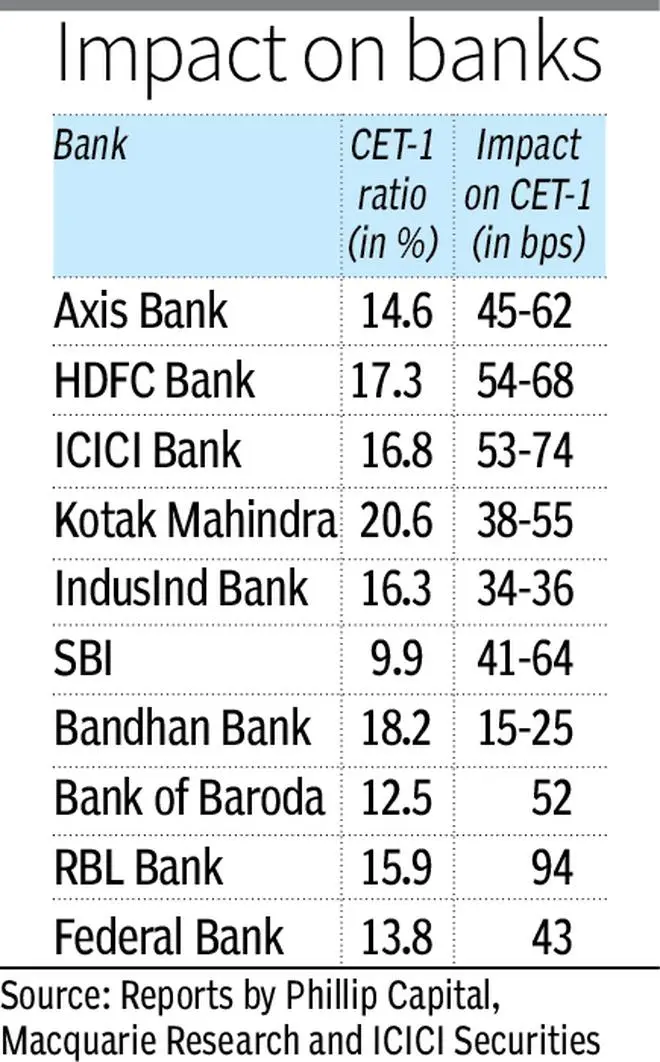

The capital requirement of banks is expected to increase by 5 per cent, or ₹84,000 crore of additional capital, due to the increase in risk weights for certain consumer loans by the RBI on Thursday. The common equity tier-I (CET-1) capital level is also expected to decline by 35–100 bps for various banks.

Currently, the banking system capital is estimated to be ₹15.2-lakh crore, and the regulatory measures will lead to banks’ CRAR (capital adequacy ratio) requirements increasing by 55–60 bps.

“Trends in consumer credit show it has been growing at 25 per cent plus since May 2022. The share of loans impacted (about ₹14.8-lakh crore) to total outstanding loans (₹1,51.5-lakh crore) is only around 9.8 per cent in September 2023,” SBI Research said, pegging the quantum of impacted personal loans at 31 per cent of the total portfolio of ₹48.3 lakh crore.

On Thursday, the RBI hiked the risk weights on unsecured consumer loans, including credit cards, by 25 percentage points for both banks and NBFCs to 125 per cent.

Risk-weighted assets for the top banks are expected to increase by 2-4 per cent based on loan mix, as a result of which brokerage firms expect common equity tier-I (CET-1) capital levels to decline by 35–100 bps. While this will lead to some moderation in credit growth to these segments, analysts don’t expect any significant slowdown as long as credit costs remain low and risk-adjusted returns remain healthy. Further, part of the impact is expected to be passed on by banks via higher lending rates to ensure return on capital is not adversely impacted.

The move will lead to prudent unsecured lending and may slow down the growth of unsecured lending over the next 3–6 months as lenders become more selective on unsecured credit, analysts said. They flagged a higher impact on ICICI Bank due to the higher share of loans of NBFCs, State Bank of India, and Axis Bank due to their relatively lower CET-1 capital levels, RBL Bank owing to the large share of credit cards, and IDFC First Bank for the high share of personal loans.

Among NBFCs, SBI Card and Bajaj Finance are seen as the most impacted, given their meaningful exposure to unsecured and personal credit. The CET-1 impact of risk weight is estimated to be around 416 bps for SBI Card and 240 bps for Bajaj Finance, whereas for other NBFCs it is seen at around 25–85 bps.

The cost of borrowing for NBFCs will also go up as banks look to increase lending rates, while a higher risk weight leads to higher capital consumption, analysts said, estimating an increase of 10–20 bps in the cost of funds. At present, bank borrowings form 32–65 per cent of the NBFC borrowing mix.

Banks, however, downplayed the impact. “Given our strong capital adequacy, either on an immediate basis or in the foreseeable future, we do not expect any impact of the increased risk weights on our growth trajectory and profitability,” said Poonawala Fincorp.

SBI Chairman Dinesh Khara told reuters that even after accounting for the increased capital requirement, the bank has enough buffers and does not see the need to accelerate fund raising.

But shares of most banks and financial companies declined on Friday, with the Bank Nifty Index ending down 1.3 per cent as all constituents barring AU Small Finance Bank ended 0.2–3.7 per cent lower.

Consumers are bracing for expensive loans as banks increase rates to compensate for the slower loan growth. “By raising the risk weightage for loans to NBFCs, the money supply will get throttled, and result in higher capital requirements for banks. For banks to maintain risk-adjusted returns, lending rates need to go up. At this stage, it is safe to assume that the lending rates can go up anywhere between 40 and 75 bps, but the actual scenario will be market-driven,” said Virat Diwanji, Group President and Head of Consumer Banking at Kotak Mahindra Bank, adding that it will definitely impact the ROE (return on equity) of lenders.

Published on November 17, 2023

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.