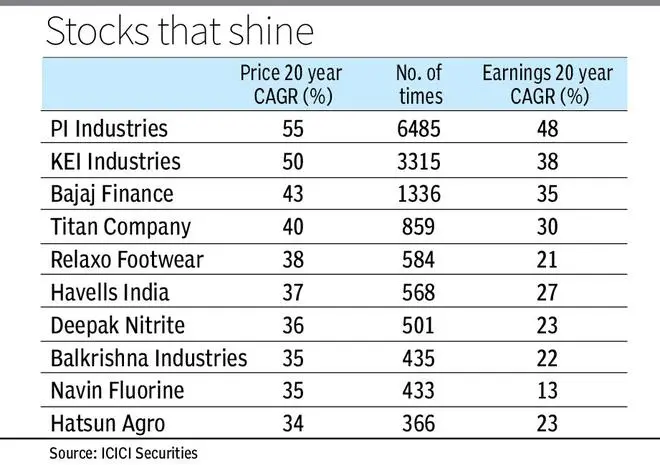

Shares of PI Industries have posted a whopping 55 per cent CAGR (compounded annual growth rate) return in the last 20 years, said a latest study by ICICI Securities.

The domestic brokerage, which came out with a study on stocks ‘through-the-cycle’ (TTC) compounders — business models that flourish during economic upcycles and preserve value during downturns — said the stock of PI Industries has risen 6,485 times.

The other top performers included KEI Industries, Bajaj Finance, Titan Company, Relaxo Footwears and Havells India.

According to the study, most of the stocks that constitute this list hail from traditional manufacturing — commodities (chemicals, cement, etc.), building materials, home appliances, capital goods, engineering, discretionary consumption, staples, pharma, etc.

A few TTC 100-baggers emanate from the services sector such as financials and ratings, it further said.

3 major cycles

Over the past 20 years, India’s ‘investment rate’, real estate and corporate profits have been through the niches and recesses of economic cycles – one full upcycle (2003–2010), followed by a full down cycle (2011–2020) and the emergence of the most recent upcycle post-FY21.

In this context, the journey through economic cycles throws up medium-term tailwinds/headwinds for stocks. Consequently, the longevity of a business model and the growth durability are put to test when a company weathers a full economic cycle.

Based on this criteria, it evaluated stocks that persevered and preserved value while battling economic downturns and reaping the full benefits of economic upcycles.

“We reckon traditional manufacturing and a few service companies form the bulk of the 100-baggers, sporting over 25 per cent CAGR stock price appreciation (ex-dividends) for the 20-year period,” said ICICI Securities.

Key learnings

Key learnings from the TTC compounders study are having a focussed business model (none of the stocks had a diversified business approach while there was a sharp focus on core business); focus on value creating growth (earnings growth and RoE greater than ‘cost of equity’); and business that earns more cash than it consumes (cumulative ‘operating cash flow’ exceeded cumulative capex over the past two decades).

Stocks of companies with high financial leverage and reduction in financial leverage over time and from regulated sectors are best avoided, it further said.

Other key findings are that competition is overstated — competition is a key risk while evaluating a company, but obsessing over it may not be beneficial for an investor; fancy growth stories such as the new age sectors during the ‘2000 dot-com bubble’ aligned under Telecom, Media and Technology (TMT) – comprising stocks with high growth expectations seldom materialise.

Cheap valuations, to start with, is an important criterion, ICICI Securities said.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.