The sugar industry stands to gain from the upcoming Maharashtra elections and the BJP’s high stakes in Uttar Pradesh.

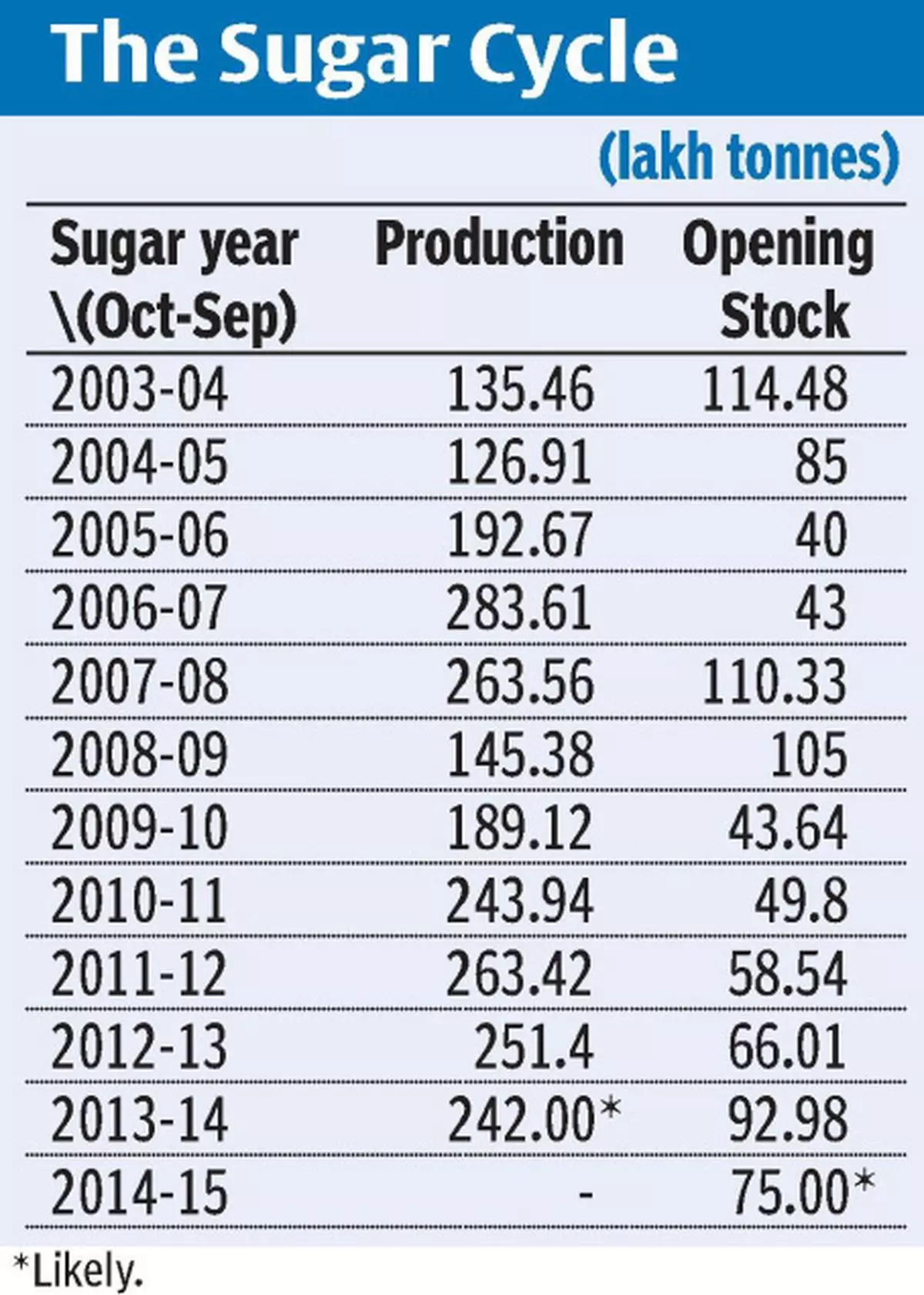

Sugar production is prone to cyclical oscillations. Typically, three years of high output is followed by two very bad production years.

Thus, 2003-04 and 2004-05 saw low production and then there was a rise for the next three years, before declining again in 2008-09 and 2009-10 (the sugar year runs from October to September).

The reason for such a pattern has largely to do with the dynamics of cane cultivation. The cane planted during March-May in UP is harvestable in about 11 months the following February-April. This plant-cane further yields a 9-10 month ‘ratoon’ crop automatically sprouting from its root stubbles, which mills can crush in November-February.

Thus, once a farmer plants cane, his land gets effectively locked for 20-21 months. It also means large arrears owed by mills prompting him not to plant this year. This could end up affecting production for the next two years. By then, soaring sugar realisations and the bidding up of cane prices by mills may induce farmers to plant again. They usually overplant, which is the prelude to the next crash.

Inevitable fallThe above ‘sugar cycle’ logic, and the fact that we have now had four consecutive high-production years, increases the likelihood of both output falling and prices firming up in the season beginning October 2014.

That is something the industry — battered by low sugar realisations and cane prices not amenable to downward adjustment because of political reasons — will not mind.

The impact of cane arrears leading to lower plantings may be especially pronounced in UP. Mills there currently owe farmers around ₹8,200 crore out of the ₹19,400 crore worth of cane procured at the official State-advised price of ₹280/quintal.

High cane dues are estimated to have reduced plantings in UP this time by 10-15 per cent, even as acreages in Maharashtra and Karnataka are said to be 10-15 per cent higher. But in the latter States, too, production in 2014-15 could be hit because of an additional factor: the prospects of a poor monsoon, courtesy El Nino.

Mildly bullishOverall, therefore, the outlook for Indian sugar is somewhat bullish — at least relative to the last three years or more. Yet, one may not see any significant improvement in price realisations only because the new sugar year would start off with stocks of roughly 75 lakh tonnes, equivalent to almost four months’ domestic consumption.

That also explains why the industry is keen on pushing exports.

Only recently, the incentive on raw sugar exports was restored to ₹3,300 a tonne after the previous Government had slashed it to ₹2,277 for shipments in April and May. The industry has also managed to convince the new Government to continue with the incentive until September 2015 and not stop it after the current sugar year ends.

The new Government may be more sympathetic to the industry keeping in view the upcoming Maharashtra Assembly elections and also the ruling BJP wanting to consolidate its position in UP after its remarkable showing in the recent Lok Sabha polls.

Given that cane growers constitute a significant vote-bank in both States, one wouldn’t rule out further ‘policy support’ for the industry in the coming days.

![]() Comments

Comments

companies that do not have access to pipeline networks, IGX added")

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.