The Fourteenth Finance Commission, Chaired by Y. V. Reddy, has a galaxy of stalwarts as members – Sushma Nath, M. Govinda Rao, Abhijit Sen and Sudipto Mundle. Given the unquestioned quality of the team, there is great anticipation regarding the guidance the Commission would provide for India’s fiscal system for 2015-2020.

The main task of the Commission is to recommend how the Union Government should share taxes levied by it with the States and furthermore, the allocation among the States. One of the most salutary traditions is that the recommendations of the Finance Commission on the sharing of taxes is never challenged by either the Centre or the States.

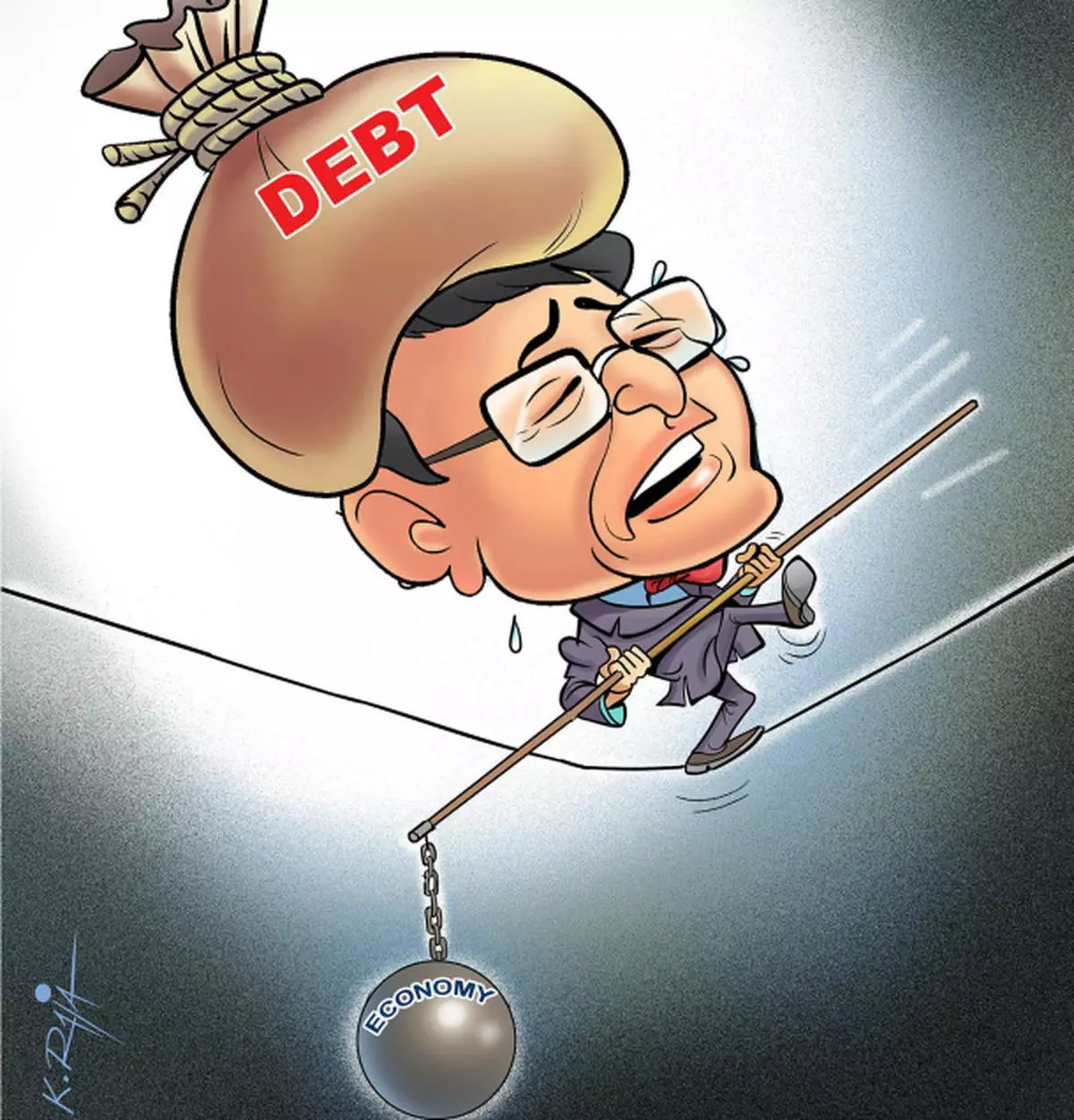

Emphasis on Debt Repayment

Earlier Finance Commissions (Eighth, Ninth and Tenth) and Comptroller and Auditor General Reports had laid emphasis on evolving a viable scheme for securing the repayment of the public debt.

While work in the Reserve Bank of India (RBI), in the latter part of the 1980s, by A. Seshan, C. Rangarajan and N. D. Jadhav highlighted the possibility of explosion of internal public debt, no specific scheme on debt repayment was worked out.

The RBI attempted some tentative work in the late 1980s to evolve a scheme for debt repayment, but it could not find a satisfactory resolution. Work in the RBI continued in the first half of the 1990s and in 1996 the RBI came up with a comprehensive scheme of a Consolidated Sinking Fund (CSF) which would, over time, become self-sustaining.

The Ministry of Finance shot down the scheme as it was felt that a CSF would be meaningless while there was a fiscal deficit. Furthermore, the then prevailing view in Government was that so long as the primary deficit was reduced there would be no problem of financing debt repayment. Over the years, a practice has evolved wherein the Government focuses its attention on its net borrowing. Once this is secured, it is for the debt manager to raise gross borrowing to meet the repayment. The system of repayment of public debt smacks of a Ponzi. Some years ago, the Government and the RBI used to highlight the Central Government’s gross borrowing, net borrowing, interest payments and the annual debt repayment profile.

Now, this information is lost in the mountain of statistical information. The RBI would do well to highlight, in its Annual Report for the year ending June 30, 2013, an annual data series from 1990-91 onwards, the Central government’s gross borrowing, net borrowing, interest payments and the profile of annual debt repayments. This information would bring out that the Central government’s public debt operations has elements of a Ponzi.

Had the RBI’s 1996 CSF scheme been implemented, by now the CSF would have been self-sustaining and there would not be recourse to borrowing to meet repayments. One hopes that the 14{+t}{+h} Finance Commission would incorporate, in its Report, an explicit examination of the debt repayment problem and suggest appropriate remedial measures.

At present, the government is seriously considering fundamental changes in the financial sector legislation. If public debt management is separated from the apron strings of monetary management and the government no longer has the crutch of the statutory liquidity ratio for banks and separate prescriptions for insurance, provident funds and pension funds, would the government be able to raise its market borrowing at low rates of interest?

In recent years there has been an elongation of the average maturity of government borrowing. At some future point of time, the average maturity could shorten. The present time is apposite for setting up a CSF.

Resources for CSF

A CSF cannot take up debt repayment immediately. It would need to develop a sufficient corpus which would then become self sustaining. The corpus of the CSF could be developed as follows:

(i) From each year’s gross borrowing, a small proportion, say 3 per cent could be earmarked for the CSF (precise figures will have to be actuarially worked out).

(ii) All proceeds from sales of public sector assets should be credited to the CSF. The sale of the family silver should be used only to reduce the government debt.

(iii) A part of the RBI profit transfer to the government should be earmarked for the CSF.

The snag is that with the creation of the CSF, the fiscal deficit would appear larger but fiscal transparency requires such hard decisions.

Finance Commission’s Role

It is sometimes argued by fiscal pundits that public debt does not create an inter-generational burden but it certainly does create an intra-generational burden. One fervently hopes that the 14th Finance Commission would undertake a study of the public debt repayment problem and come up with an enduring solution. Internal debt, unlike external debt, is a silent, sudden killer. The public debt Ponzi must be stopped before it disrupts government finances.

The author is an economist

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.