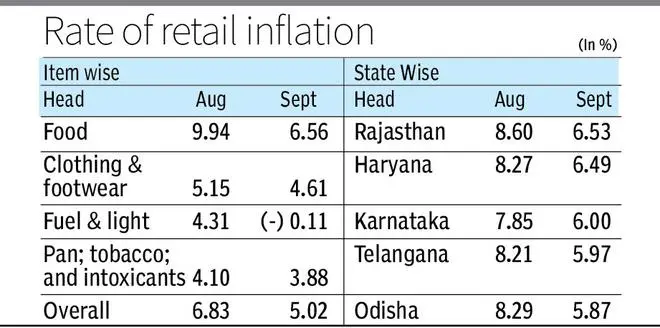

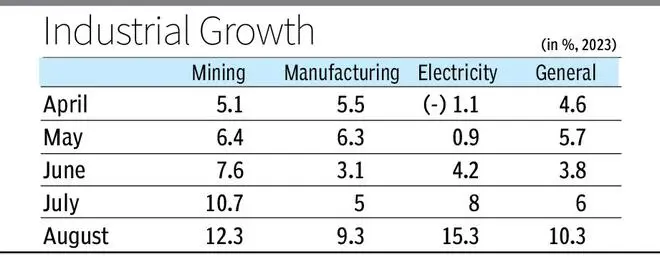

Two high frequency indicators reflected a sudden positive turn for the economy on Thursday. The consumer price index (CPI)-based inflation for September cooled down to 5.02 per cent as against 6.8 per cent in August, coming back to the Reserve Bank of India)‘s upper tolerance band of 2-6 per cent. Simultaneously, industrial growth based on Index of Industrial Production (IIP) surged to a 14-month high of 10.3 per cent in August.

The main reason for the drop from 6.8 per cent in August was a fall in vegetable and oil prices. Industrial growth surged on account of strong manufacturing activity. Experts feel that with these two indicators showing a positive turn, there is a possibility that the pause on policy repo rate (at which RBI lends money to commercial bank) will continue till August next fiscal.

In terms of State-wise inflation, two poll bound provinces – Rajasthan and Telangana – continue to have inflation rate higher than the national average. Other States where inflation continues to be high include Haryana, Karnataka and Odisha.

Swati Arora, Senior Economist with HDFC Bank, said moderation in CPI inflation was largely on account of correction in vegetable prices and edible oil prices. Vegetable prices are expected to ease further with the onset of winter. However, risks from higher pulses and cereals price remain within the food basket.

“We expect inflation to average around 5.6 per cent in Q3 FY24. For the full year, headline inflation is expected to average at 5.3 per cent while core is expected to average below 5 per cent,” she said. Echoing the sentiment, Aditi Nayar, Chief Economist with ICRA said headline CPI inflation will remain volatile in a wide range until June 2024, with the outlook for food inflation remaining murky and continuing volatility in crude oil prices.

Nevertheless, further monetary tightening is not warranted in the near term. “Given the MPC’s CPI inflation projections for Q1 FY2025 and the derived forward looking real policy rate, we maintain our expectations of an extended pause until the beginning of a shallow rate cut cycle of 50-75 bps in August 2024,” she said.

Experts also see the present trend of inflation as good for the debt market. Akhil Mittal Senior Fund Manager (Fixed Income) with Tata Asset Management said core inflation has come-off further at 4.5 per cent. This bodes well for future inflation expectations and also provides comfort to RBI regarding probability of meeting inflation trajectory. “I think this would be positive for markets and provide a breather to yields, which were headed higher since MPC review further fueled by geo-political developments. Overall positive for markets,” he said.

Industrial Growth

All-round growth in industrial sector pushed factory growth to 10.3 per cent in August as against 6 per cent in July. Manufacturing did better but two other sectors – Mining and Electricity – showed doubled digit growth. However, experts were not so optimistic about coming months.

Dipti Deshpande, Principal Economist with Crisil, felt industrial activity is expected to remain resilient but lose steam in the coming months. One indication for this was moderation in PMI for manufacturing to 57.5 in September from 58.6 previous month. In the coming months, the external environment will be a drag, as major western economies decelerate in the second half of 2023.

The impact of uneven monsoon on rural demand also remains to be seen. The transmission of rate hikes to lending rates could also temper domestic demand in the second half. “Overall, we expect GDP growth at 6 per cent for this fiscal compared with 7.2 per cent last year,” she said.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.