Shares of Steel Authority of India Ltd (SAIL) have been moving in a narrow range this year and remain lacklustre with a flat return of 0.4 per cent year-to-date. On the other hand, Tata Steel and Jindal Steel & Power gave a return of 4.8 per cent and 8.84 per cent. However, on Friday, the stock closed 1.4 per cent higher at ₹89.27 even as analysts see only a little headroom for the stock due to cost pressure post its Q4 performance.

The PSU steel-maker reported a standalone profit of ₹1,241 crore for Q2-FY24, against a loss of ₹386 crore a year ago. The company reported ₹29,714 crore of revenue from operations, up 13 per cent year-on-year. Revenue in the year-ago period was ₹26,246 crore.

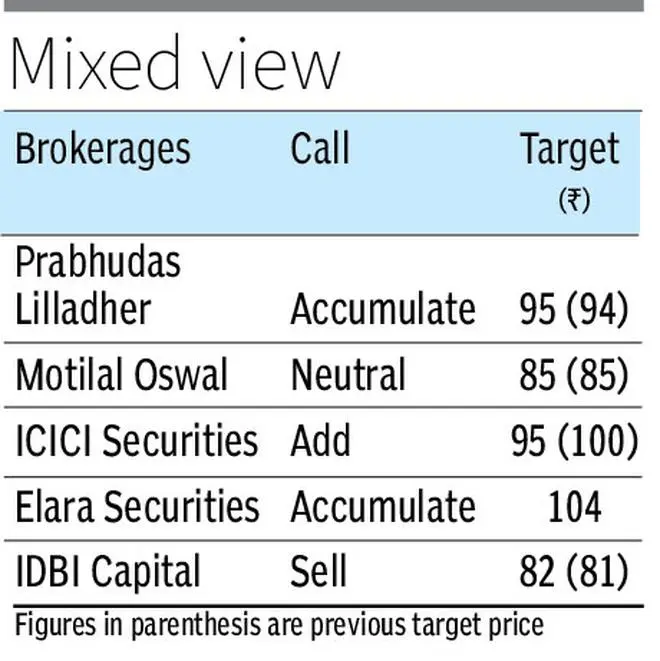

SAIL has delivered the highest volume growth among peers in Q2-FY24, said ICICI Securities. “We expect this to result in operating leverage benefits”. Besides, the coking coal procurement structure of the company is likely to ensure that it is better insulated from the adverse impact of higher international coking coal price in Q3-FY24. “Taking cognisance of Q2-FY24’s performance, we trim our FY24/FY25 EBITDA by 5 per cent each, resulting in a revised TP of ₹95 (earlier ₹100),” it added.

Motilal Oswal, retaining its Neutral stance with a target price of ₹85, said SAIL has earmarked ₹1-lakh crore for expansions across all its facilities over the next decade. “As the intensity of capex is expected to pick up post FY25, it would limit the deleveraging going ahead and thereby put pressure on the balance sheet and cash flow,” Motilal Oswal said, adding, “In line with the increase in coal cost and capex guidance, we have reduced our EBITDA estimates for FY24/FY25 by 10/1 per cent.

EBITDA concerns

IDBI Capital reiterated its Sell rating on SAIL with a target price of ₹83 (₹81 earlier), and expected its EBITDA growth to remain muted over FY24-25. “Further, SAIL has not lined up any major expansion plan in the coming two-three years. Hence, volume growth for SAIL is likely to be lower compared to its peers over the coming three-five years,” IDBI Capital said.

Elara Securities pointed out that as per SAIL management, the rise in coking coal prices will put pressure on operating cost; however, better steel prices in the past few weeks and benefits of selling at higher prices to railways will keep a check on margin. “SAIL is in the process of implementing several efficiency improvement measures and debottlenecking projects. We believe successful execution of these projects will be a key driver for future performance. While we largely retain our EBITDA estimates for FY26, we increase them about 7 per cent for FY24 and one per cent for FY25 to factor in better-than-expected performance in Q2-FY24. Further, we roll over to September 2025 from June with a TP of ₹104 based on 4.5x September 2025E EV/EBITDA,” Elara said.

Tushar Chaudhari, Analyst, Prabhudas Lilladher Pvt Ltd, said weak operating performance continues for SAIL. “We cut FY24/25 EBITDA estimates by 5/2 per cent on weaker H1 performance. We expect SAIL to remain a play on steel prices in medium term as its volume growth would depend upon successful execution of its planned capex in phases and significant capacity addition would only come post FY28; near-term volume growth would remain 8-10 per cent, but margins can get affected by higher coking coal costs. However, hardening iron ore prices will keep SAIL’s strategic advantage intact vis-a-vis peers,” he said.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.