With the latest dividend announcement, Hindustan Zinc will close FY23 with a dividend of ₹75.5 per share. Given the fact that the share is currently trading around ₹320, the dividends imply a staggering dividend yield of 23 per cent, more than adequately compensating for flattish share performance in FY23.

Though the shareholders of Hindustan Zinc—its promoter Vedanta (64.9 per cent stake), the Centre (29.5 per cent), LIC (2.7 per cent) and retail investors (1.4 per cent)—cannot complain, the latest surge in dividends raises questions on promoter’s motive.

Hindustan Zinc has been considered a dividend play with an average yield of 7.6 per cent in last five years. Though the company’s balance sheet remains healthy, depleting cash reserves, a threefold increase in dividend payouts, company’s financials and other factors indicate that it may not continue as a ‘high dividend’ play in the future.

Dividend bonanza

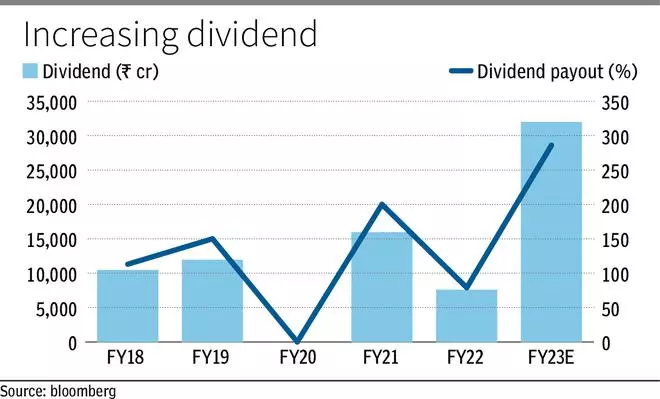

Hindustan Zinc’s recently announced dividend, which is the fourth in the current financial year, brings the company’s total dividends paid in FY23 to ₹32,000 crore, a staggering 250 per cent increase over the last five-year average dividend paid.

For context, the annualised revenues and PAT based on the financials for the first nine months of FY23 are at ₹34,100 crore and ₹10,570 crore, respectively. The payout ratio, which has averaged around 108 per cent in the last five years, may increase to nearly 300 per cent in FY23. Previously, FY21 proved to be a high dividend year, while there were no dividends in FY20.

Declining cash reserves

The company has been reinvesting funds back into the business at a healthy rate. The capex as a percentage of net profit has been at a healthy average of 37 per cent in the last five years. Revenue growth at 11 per cent CAGR in the last five years also supports this fact.

On the other hand, the company’s liquidity position has taken a hit. Despite good growth in revenue and profit, the cash position of the company has declined at 5 per cent CAGR in the last five years and its gross cash stood at ₹16,500 crore at the end of 9M FY23 (after taking into account the three interim dividends this financial year). Assuming fourth quarter operations finance half of the fourth interim dividend declared recently, Hindustan Zinc gross cash position may decline to a little above ₹10,000 crore by the start of FY24 compared to ₹35,000 at the end of FY16.

Hindustan Zinc will now pay 2 per cent of its consolidated revenue to parent Vedanta for the usage of brand and strategic management services of the parent, effective from October 2022. This will dent the cash flows to an extent. Also, prices of Zinc have declined more than 10 per cent in the year and are expected to remain weak owing to weak global commodity markets. The rupee depreciation that provided a strong support earlier may also turn into a headwind. Weak operating outlook and deflated gross cash position at Hindustan Zinc does not support a sustained high dividend outlook.

Promoter’s motive

Also, there are certain corporate overhangs which will have to be cleared as well. Recently, board of the Hindustan Zinc has declared its intent to purchase THL Zinc, a subsidiary of the parent Vedanta Group for close to ₹24,000 crore.

Being a related party transaction between two subsidiaries of a parent—Vedanta, the move also required a majority of minority shareholders to approve the deal. The Centre, which is a significant minority shareholder rejected the proposal last month and asked for a non-cash way of merging the sister entities. The Centre is also looking to offload stake in Hindustan Zinc to meet its divestment target, implying a higher supply of shares in the market in addition to weak outlook for dividends.

Vedanta has recouped close to ₹43,800 crore in the last five years from its subsidiary and can also expect 2 per cent on consolidated revenues going forward.

As the proposed stake sale in Hindustan Zinc is facing hurdles, the recent dividend announcement may be a way for Vedanta to access the cash lying at Hindustan Zinc to meet its debt obligations.

Although the parent’s debt metrics are currently healthy, they are experiencing a decline on a standalone basis.

The interest coverage ratio has declined from 8.7 times at the end of December 2021 to 5.5 times at the end of December 2022 due to slowdown in commodity prices.

With expectations of a further slowdown, debt metrics might raise slight concerns.

Vedanta Resources (the UK arm), which holds a controlling stake in Vedanta (the Indian listed arm), has debt maturities of $5.3 billion (₹43,560 crore) in the next two fiscals.

After the recent Adani saga, the listed bonds of Vedanta Resources also came under pressure. While the UK arm has reported an EBITDA of $2.5 billion in H1 FY23 (September 2022), volatile macro environment, rising interest rates and their impact on commodity markets are the major concerns for bond investors. Bonds maturing in January 2024 were trading at around 15 per cent discount to par value in the recent period. Vedanta, the Indian listed entity, announced that its board is considering a fifth interim dividend on March 28th, which may indicate the cash flow requirements of the entities.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.