‘Inflation is just like alcoholism. When you start printing too much money, the good effects come first. The bad effects only come later.’ – Milton Friedman

If you thought the now popular ‘Buy Now Pay Later’, or BNPL, theme is a new concept, well you are wrong. Globally governments and central banks had taken to this financial engineering route long before the private sector caught on to this concept. This is back in the spotlight after the recent downgrade of US sovereign ratings by Fitch.

Printing money to fund government spending with hopes of paying it back later was the fulcrum of stimulative policies in the era since the global financial crisis. As the good effects of money printing started weighing in with no sign of bad effects for many years, governments only got emboldened and got more aggressive when Covid struck.

But the recent years’ binge seem to have been the proverbial last straw that broke the camel’s back.

Double whammy

Many of the developed market economies are now facing the double whammy of high government debt to GDP even as interest rates or yields on government debt are also at multi-decade highs.

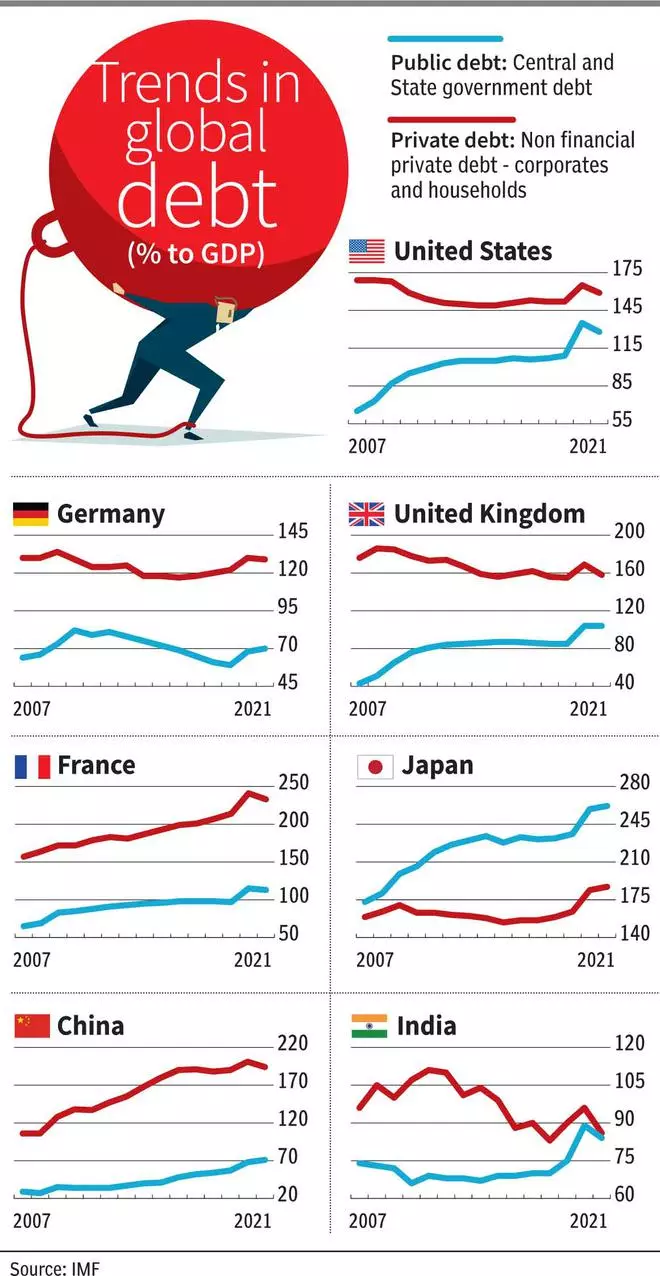

Analysis of data from the IMF on global debt that is available till 2021 indicates that large economies like US, UK, France, Japan and China have all seen a reckless increase in government debt (see chart) since 2007. Germany and India are the exceptions to this trend amongst large economies.

During the same time period, the private sector leverage, which was on binge pre-global financial crisis driven by a global housing boom and optimistic growth assumptions, has been on the mend at least in some of the countries. There are some exceptions though — China and France.

A common theme last year when economic growth concerns came to the fore was that private balance-sheets and consumer savings are strong including in the US. However, the irony is that government balance-sheets are weak now. The Covid era stimulus shifted the burden of debt in many countries from the private to the public sector.

So what?

Sure, the government can print money as much as it wants to repay debt. But here is the catch, as Milton Friedman warned, the bad effects of money printing come later. Bond vigilantes or the investors who protest against expansionary fiscal and monetary policy are back in play.

When Lizz Truss as British Prime Minister attempted an expansionary budget in a high inflation economy, bond investors showed their ire by dumping UK bonds.

This happened to such an extent that the Bank of England had to make a complete U-turn in a matter of weeks on its quantitative tightening policy (opposite of quantitative easing). The BOE thinking was that this was warranted to avert a major financial accident in the UK. Following the bond market disaster Liz Truss had to resign with the infamous record of shortest serving Prime Minister in UK history.

And, bond vigilantes are back in action not just in the UK but across the world too, with bond yields in the US and Europe at levels not seen in more than a decade. Higher yields will constrain government spending constricted by the interest burden.

For example, if the interest rate on government bonds across maturities increases by 2 per cent in the US, at current debt levels, it will increase its consolidated fiscal deficit-GDP ratio by a significant 2.5 per cent, assuming no cuts on current spending.

If the US government intends to maintain its current fiscal deficit, then it will have to reduce the spending elsewhere. Thus, across the developed world, governments have tough choices to make and these pose challenges to economic growth.

India effect

India’s public and private debt appear in good shape. But the risk we face is that of the spill-over effects as developed economies deal with their debt burden.

While we were indirect beneficiaries of their low interest regime and spending binge, we must be on the guard for collateral damage this time around.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.