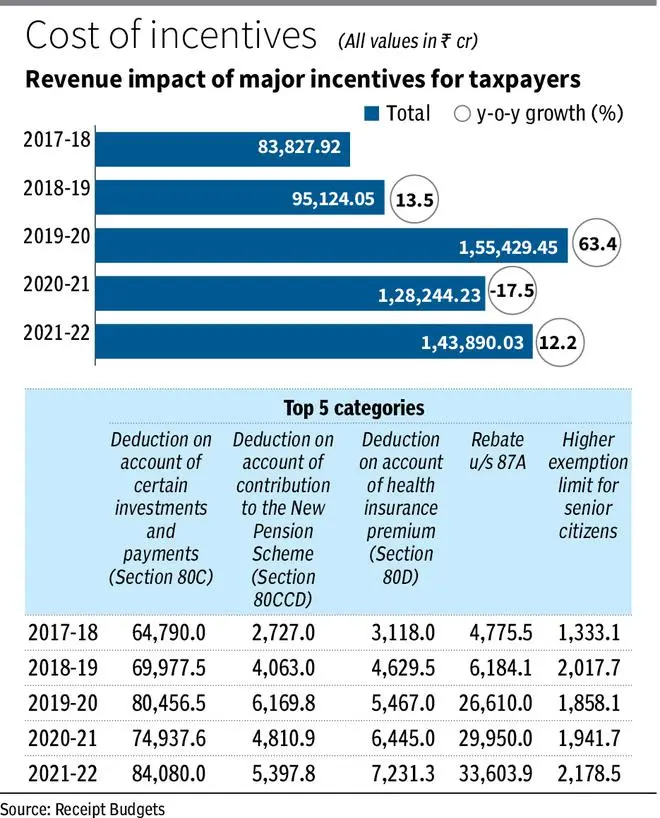

In FY22, India is projected to have foregone ₹1.43-lakh crore by allowing incentives to income taxpayers. This is a 12 per cent increase from the revenue Impact of major income tax Incentives for in FY21, which was ₹12.82-lakh crore. However, it is much lower than the pre-pandemic figures of ₹1.55-lakh crore.

A major chunk of this money, 58.4 per cent of it, comes from deductions claimed on account of investments and payments under Section 80C of the Income Tax Act. This Section allows individuals and Hindu Undivided Families a maximum deduction of ₹1.5 lakh every year from the total income.

This includes investments made under Public Provident Fund (PPF), Employees’ Provident Fund (EPF), LIC premia and equity. In FY22, the centre is projected to forego ₹84,080 crore, on account of this incentive. This is, however, not part of the new tax regime. This could also mean that in FY22, not many chose to move to the new income tax regime.

“The revenue impact for providing a tax incentive for investments in various saving instruments, repayment of housing loan and payment of tuition fees for children is the single largest tax expenditure in case of individual taxpayers followed by rebate on tax in case of resident individuals having income up to ₹5 lakh, deduction on account of health insurance premium and contribution to the new pension scheme,” reads the receipt budget for FY24.

The next biggest contributor is Section 80D, which is around ₹7,231 crore. Every individual or HUF can claim a deduction from their total income for medical insurance premiums paid up to ₹25,000 in any financial year. In the case of senior citizens, the deduction limit allowed is ₹50,000.

The amount under this Section has been rising every year and in FY22, it is projected to have jumped by 12 per cent, compared with FY21, indicating that more people are taking up health insurance.

As a rebate under Section 87A, the centre could have foregone around ₹33,603.9 crore. While these figures fell largely between FY19 and FY20, they started picking up since then. This Section applies to people whose income does not exceed ₹5 lakh per annum.

They are eligible to claim this rebate and not pay any tax. The other major contributors are Section 80CCD, which relates to the deductions under the National Pension Scheme (NPS) or the Atal Pension Yojana (APY) and the higher exemption limit for senior citizens.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.