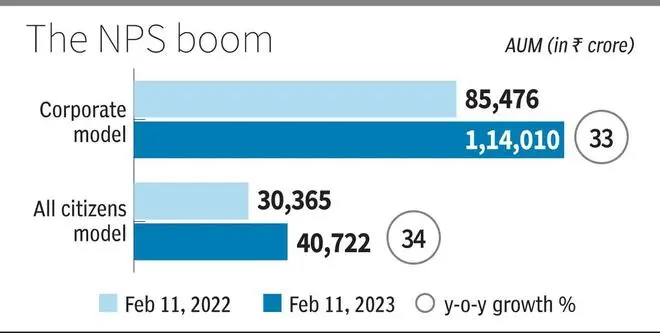

‘Corporate model’ under the National Pension System (NPS) has recorded a robust 33 per cent year-on-year growth in assets under management (AUM) as of February 11 at ₹1.14 lakh crore (₹85,475 crore).

The number of subscribers under the ‘Corporate model’ too saw a sizeable growth of 21 per cent at 16.50 lakh (13.60 lakh), official data with pension regulator PFRDA showed.

The “Corporate Model” is one of the two models under the National Pension System (NPS) in India. The other model is the “All Citizen Model”.

The ‘All Citizen model’ recorded 34 per cent year-on-year AUM growth as of February 11 at ₹40,722 crore (₹30,365 crore), PFRDA data showed. The number of subscribers in this model grew 34 per cent to 27.82 lakh (20.80 lakh).

This is a clear pointer that NPS is becoming an increasingly popular retirement savings option among individuals, and its continued growth is expected to play an important role in providing financial security to millions of Indians in their retirement years.

Under Corporate model, a retirement savings scheme of NPS regulated by the PFRDA, employers can enroll their employees in the NPS and make contributions to their retirement savings accounts.

The Corporate NPS scheme offers several benefits to employees, including portability, flexibility, and tax benefits. Employees can choose from a variety of investment options, including equity, corporate bonds, and government securities, and can also change their asset allocation based on their risk appetite and investment goals.

All Citizen Model

The All Citizen Model is designed for all citizens of India, including both employed and self-employed individuals. Under this model, any individual between the ages of 18 and 65 years can open a Tier-I pension account with a Pension Fund Regulatory and Development Authority (PFRDA) registered Point of Presence (PoP).

In the All Citizen Model, the individual has the flexibility to choose their pension fund manager, investment scheme, and asset allocation pattern.

The NPS is a defined contribution pension system, which means that the pension benefits are determined by the amount of contributions made by the individual and the performance of the investments made by the pension fund.

The All Citizen Model of NPS is regulated by the PFRDA, and the contributions made by the individual and their employer (if applicable) are invested in a mix of equity, debt, and government securities, depending on the individual’s choice of investment scheme.

Over the years, the NPS has gained popularity among individuals as a reliable and efficient tool for retirement planning. One of the key indicators of the growth of the NPS is its assets under management (AUM). The AUM of the NPS has been steadily increasing over the past few years, indicating that more and more individuals are choosing the NPS as their retirement savings option.

Overall pension assets

As of February 11 this year, the overall pension assets (NPS and Atal Pension Yojana - APY) AUM crossed ₹8.75 lakh crore, up 22 per cent over ₹7.15 lakh crore on the same day last year. While the Central government employees NPS value stood at ₹2.53 lakh crore, it was ₹4.37 lakh crore in the case of State Government employees accumulations.

The AUM has grown at a compounded annual growth rate (CAGR) of around 28% over the past five years.

The NPS has witnessed a significant increase in the number of subscribers in recent years. It stood at 6.18 crore subscribers as of February 11 this year from a level of 5 crore on the same day last year.

The increase in subscribers can be attributed to various measures taken by the government to promote the NPS, such as tax incentives, greater awareness, and the ease of registration and contribution.

The strong performance of the underlying asset classes has also contributed to the growth of the NPS AUM. The NPS offers a range of investment options, including equity, corporate bonds, government securities, and alternate investments. The equity component of the NPS has performed particularly well in recent years, as the Indian stock market has witnessed a strong bull run. The equity component of the NPS has generated an average annual return of around 16% over the past five years, which has attracted more individuals to invest in the NPS.

multiple factors at play

Supratim Bandyopadhyay, former PFRDA Chairman, said that the good response for both Corporate model and All citizens model is due to combination of factors. “One is increased awareness through PFRDA conducted awareness sessions and increased realisation among people that they have to do something about old age requirements. Secondly the tax benefit and lastly the kind of flexibility provided and returns generated by NPS so far over a period of time.”

Puneet Gupta, Partner, People Advisory Services, EY-India, said that tax reforms have been an important consideration for taxpayers in opting for the NPS.

At the contribution stage, a tax deduction is available for employer’s contributions to the extent of 10 per cent of basic salary (subject to a maximum of ₹750,000 for aggregate contributions towards NPS, Provident Fund and Superannuation fund in a financial year). Further, an additional deduction is available for employee’s contributions to the extent of ₹50,000 per annum. The deduction for employee’s contribution of ₹50,000 is in addition to the deduction of ₹ 150,000 available under Section 80-C for various contributions, investments and expenses. Even under the concessional tax regime, tax deduction is available for employer’s contributions to NPS (not available for employee’s contribution). At withdrawal stage, lump-sum withdrawal from NPS is fully non-taxable. This has made NPS more attractive from a tax perspective, Gupta said.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.